Alright, let’s talk about something that probably isn’t high on your list of exciting college experiences: car insurance. I get it. Between classes, exams, social life, and maybe a part-time job, the last thing you want to do is wade through insurance jargon. But here’s the thing: if you’re a college student in the USA with a car, or planning to get one, navigating the world of auto insurance can feel like trying to solve a Rubik’s Cube blindfolded. It’s often expensive, confusing, and frankly, a bit daunting.

That’s where I come in. Think of me as your seasoned guide, someone who’s seen the ins and outs of this particular maze. My goal isn’t just to tell you what to do, but to show you how to do it, making sure you don’t just find any policy, but the best car insurance for college students USA has to offer – one that fits your budget and lifestyle. We’re going to break down the strategies, the hacks, and the crucial questions you need to ask to secure reliable coverage without sacrificing your ramen budget. Let’s get started, shall we?

Decoding the College Student Insurance Conundrum

Why is car insurance such a headache for college students? Well, insurers look at risk, and unfortunately, young drivers (especially those under 25) are statistically considered higher risk. Less experience behind the wheel, combined with a higher likelihood of distractions (hey, we’ve all been there!), often translates to higher premiums. It’s not personal; it’s just how the actuarial tables churn. This can make finding cheap car insurance for college students feel like an uphill battle.

But don’t despair! The myth that affordable insurance is impossible for students is just that – a myth. What fascinates me is how many students simply accept the first quote they get, not realizing there are numerous levers they can pull to significantly reduce costs. Understanding these factors is your first step to empowerment. We’re not just looking for coverage; we’re looking for smart coverage.

Smart Strategies for Scoring Student Car Insurance Discounts

This is where the real savings begin. Insurance companies actually want to reward responsible behavior, and many have specific programs tailored for students. You just need to know where to look and what to ask for.

The All-Important Good Student Discount

This is probably the most well-known and impactful discount for college students. If you maintain a certain GPA (usually a B average or 3.0), many insurers will offer a significant discount. Why? Because academic discipline often correlates with responsible driving habits. Always, always, always ask about the good student discount . You’ll typically need to provide transcripts to prove eligibility, but it’s well worth the minor hassle.

Driver’s Education & Defensive Driving Courses

If you’ve completed an approved driver’s education course, or if your state offers defensive driving courses, these can lead to discounts. Not only do they make you a safer driver (which is invaluable, truly), but they also signal to your insurer that you’re committed to minimizing risk. It’s a win-win.

Telematics and Usage-Based Insurance (UBI)

This is a game-changer for many young drivers. Companies like State Farm (Drive Safe & Save), Progressive (Snapshot), and Geico (DriveEasy) offer programs where they monitor your driving habits (speed, braking, mileage) via an app or a device plugged into your car. If you’re a safe driver, you can earn substantial discounts. This is particularly beneficial for students who don’t drive frequently or have excellent driving habits. Embracing telematics insurance can really pay off.

Other Potential Student Car Insurance Discounts

- Student Away at School Discount: If you attend college more than 100 miles from home and don’t take your car with you, you might qualify for this. It acknowledges that your risk of driving is significantly reduced. This is key for those looking for car insurance for students living away from home.

- Multi-Car/Multi-Policy Discount: If you’re on your parents’ policy (more on that in a moment), combining policies can often lead to savings for the whole family.

- Vehicle Safety Features: Anti-lock brakes, airbags, anti-theft devices – these aren’t just for your safety; they can lower your premium too.

Parent’s Policy vs. Your Own | What’s the Smart Play?

This is a common dilemma, and honestly, there’s no single right answer for every student. It largely depends on your specific situation.

Staying on Your Parent’s Policy

For most students, especially those living at home or attending college nearby, remaining on your parent’s policy is often the most cost-effective option. Why? Because you benefit from their established driving record, higher credit score (if applicable), and potentially multi-car or multi-policy discounts. It streamlines things, and insurers often prefer to keep families together on one policy.

However, if you’re attending college far from home and taking your car with you, or if your parents’ insurer has very high rates for young drivers, it might be worth exploring alternatives. Also, be aware that any accidents or tickets you incur will affect your parents’ rates, which could be a point of contention. It’s a conversation to have, for sure.

Getting Your Own Policy

When does it make sense to venture out on your own? If you’re financially independent, have your own credit history, or if your parents’ rates are simply too high for you to remain on their policy, then exploring individual options is a must. This is also often the case if you’re living in a different state for college, as insurance regulations and rates vary widely by location. You’ll want to specifically search for car insurance for young drivers in your college town or state.

The key here is to run the numbers for both scenarios. Don’t assume one is better without getting actual quotes. Sometimes, the difference can be surprisingly small, or surprisingly large!

Navigating the Quote Maze | Tips for Young Drivers

Once you know whether you’re looking for an individual policy or adding yourself to a family one, the next step is to compare car insurance quotes . This isn’t just a suggestion; it’s absolutely crucial. Rates can vary by hundreds, even thousands, of dollars between different providers for the exact same coverage.

Start by gathering all necessary information: your driver’s license number, vehicle identification number (VIN), academic transcripts (for that good student discount!), and any driving course certificates. Then, get at least three to five quotes from different insurers. Don’t be afraid to use online comparison tools, but also consider calling a local independent agent who can shop multiple carriers for you. They often have insights into local discounts or specific insurers that cater well to students.

Understanding what you’re actually paying for is also vital. Don’t just look at the bottom line. Here’s a quick rundown of essential coverage types:

- Liability Coverage: This is legally required in almost every state. It covers damages (bodily injury and property damage) you cause to others in an at-fault accident. I can’t stress this enough: skimping here is a huge risk. Aim for higher limits than the state minimums if you can afford it. Think about how unexpected expenses like medical bills could impact your financial health. Understanding different types of insurance, even beyond car insurance, can help you manage overall risks. For example, knowing about family health insurance or rental property insurance can broaden your financial literacy.

- Collision Coverage: This pays for damage to your own vehicle if you hit another car or object, regardless of fault.

- Comprehensive Coverage: This covers non-collision damage to your car, such as theft, vandalism, fire, or damage from natural disasters.

- Uninsured/Underinsured Motorist (UM/UIM): Protects you if you’re hit by a driver who doesn’t have enough (or any) insurance. Given the number of uninsured drivers out there, this is a smart addition.

When choosing your deductible (the amount you pay out-of-pocket before insurance kicks in), consider your emergency fund. A higher deductible means lower monthly premiums, but you’ll pay more upfront if you have an accident. Balance your ability to pay with your desire to lower car insurance premiums .

Beyond the Policy | Keeping Costs Low Year-Round

Your insurance journey doesn’t end once you sign the dotted line. There are ongoing habits and decisions that can continue to save you money.

Maintain a Stellar Driving Record

This sounds obvious, but it’s the single most important factor over the long term. Avoid tickets, avoid accidents. A clean driving record is gold. Insurers will look back several years, so every safe mile you drive builds a positive history that translates to lower rates.

Choose Your Vehicle Wisely

If you’re in the market for a car, remember that the type of vehicle you drive significantly impacts your insurance costs. Sports cars, luxury vehicles, and cars with high theft rates are almost always more expensive to insure. Opt for a reliable, safe, and less flashy model, and you’ll likely see lower premiums. You can often check vehicle safety ratings and crash test results from organizations like theInsurance Institute for Highway Safety (IIHS)before you buy.

Review Your Policy Annually

Life changes, and so do insurance rates. Don’t just set it and forget it. Every year, especially around renewal time, take 15-20 minutes to review your policy. Have you moved? Changed schools? Gotten better grades? Paid off your car? All these factors could impact your rates. It’s also a good time to re-shop for quotes and see if another insurer can offer you a better deal. Loyalty is great, but sometimes a new provider offers more competitive pricing.

FAQs | Your Burning Questions Answered

Can I stay on my parents’ policy if I’m away at college?

Often, yes! Many insurers allow students who attend college away from home to remain on their parents’ policy, especially if they still consider the parents’ address their primary residence and don’t have their own car registered solely in their name. Make sure your parents inform their insurer about your student status and address, as some companies offer a ‘student away at school’ discount.

What’s the difference between comprehensive and collision coverage?

Collision coverage pays for damage to your car resulting from a collision with another vehicle or object. Comprehensive coverage , on the other hand, covers damage to your car from non-collision events like theft, vandalism, fire, natural disasters, or hitting an animal. Both are typically optional unless your car is financed or leased.

How much does car insurance usually cost for a college student?

This is the million-dollar question, and unfortunately, there’s no single answer. The average cost of car insurance for college students varies wildly based on age, gender, location, vehicle type, driving record, coverage limits, and available discounts. It can range from under $100 per month to several hundred. The best way to know is to get personalized quotes.

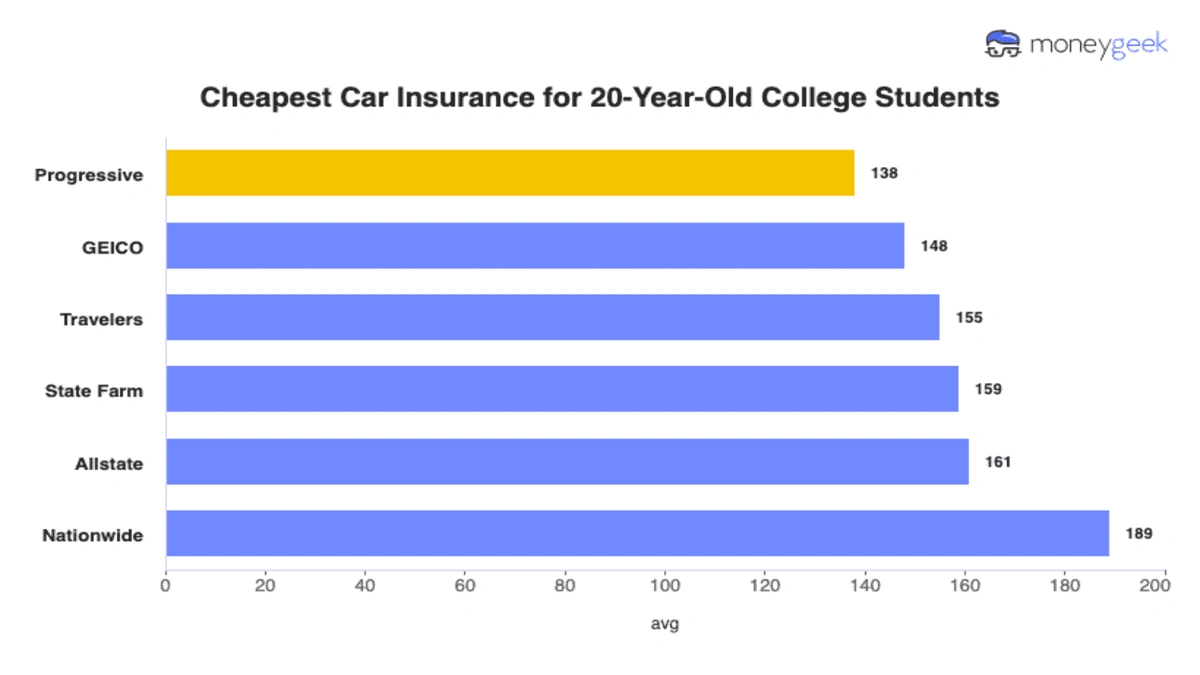

Are there specific companies better for students?

While many major insurers (Geico, State Farm, Progressive, Allstate, Farmers, USAA for military families) offer student-friendly discounts and programs, there isn’t one universal ‘best’ company. Your individual profile will dictate which insurer offers you the most competitive rates. It’s always about comparing personalized quotes.

What if I only drive occasionally?

If you’re a student who drives infrequently, consider telematics or usage-based insurance programs (like those mentioned earlier). Some companies also offer pay-per-mile insurance. These options can be significantly cheaper than traditional policies, as they directly tie your premium to your actual driving habits and mileage.

What documents do I need to get car insurance?

You’ll typically need your driver’s license, vehicle registration, vehicle identification number (VIN), and proof of your academic standing (transcripts for a good student discount). If you’re on a parent’s policy, they’ll need similar information for their existing policy.

So, there you have it. Finding the best car insurance for college students USA isn’t about magical secrets; it’s about being informed, proactive, and a little bit savvy. By understanding your options, leveraging discounts, and making smart choices, you can protect yourself and your finances without feeling like you’re paying a tuition fee for your car. Drive safe, study hard, and enjoy the ride!