Alright, let’s talk shop. If you’re a contractor in the UK, whether you’re a seasoned pro or just starting out, there’s one thing that often gets pushed to the back burner amidst project deadlines and client demands: insurance. Specifically, your contractor insurance UK liability cover. And let me tell you, it’s not just another box to tick. It’s the very bedrock of your professional peace of mind, the safety net that catches you when the unexpected, and often expensive, happens.

I’ve seen it time and again – contractors, brilliant at their craft, but a little… let’s say, ‘optimistic’ about potential risks. They think, “It won’t happen to me.” But here’s the thing: in the world of contracting, where you’re often working on client premises, providing expert advice, or even just using your tools, ‘it’ absolutely can happen. And when it does, the financial fallout can be devastating, threatening not just a project, but your entire livelihood. So, how do you navigate this often-confusing landscape? How do you ensure your business insurance for contractors truly protects you? Let’s break it down, step-by-step, so you can build your business on solid ground.

Why “Just Any” Cover Won’t Cut It | Understanding Your Core Risks as a UK Contractor

You’re not an employee; you’re an independent professional. This distinction, while offering immense freedom, also shifts the burden of risk squarely onto your shoulders. When you’re working for a client, you’re responsible for your actions, your advice, and often, the actions of anyone working under you. This is where the specific nuances of contractor insurance UK liability cover become critically important. It’s not just about having some insurance; it’s about having the right insurance that addresses the unique vulnerabilities of your contracting work.

Think about it: are you visiting client offices? Handling sensitive data? Providing crucial consulting advice? Using specialised equipment? Each of these scenarios carries its own set of potential pitfalls. A slip on a client’s wet floor, a piece of advice that leads to a financial loss for your client, or even an injury to a temporary assistant – these aren’t just theoretical possibilities. They’re real-world risks that demand robust protection. This isn’t just about legal compliance; it’s about safeguarding your reputation and your financial future.

The Three Pillars of Protection | Deciphering Key Liability Covers

When we talk about contractor insurance UK liability cover, we’re typically looking at three main types. Each serves a distinct purpose, and depending on your specific work, you’ll likely need a combination of them. Let’s demystify each one.

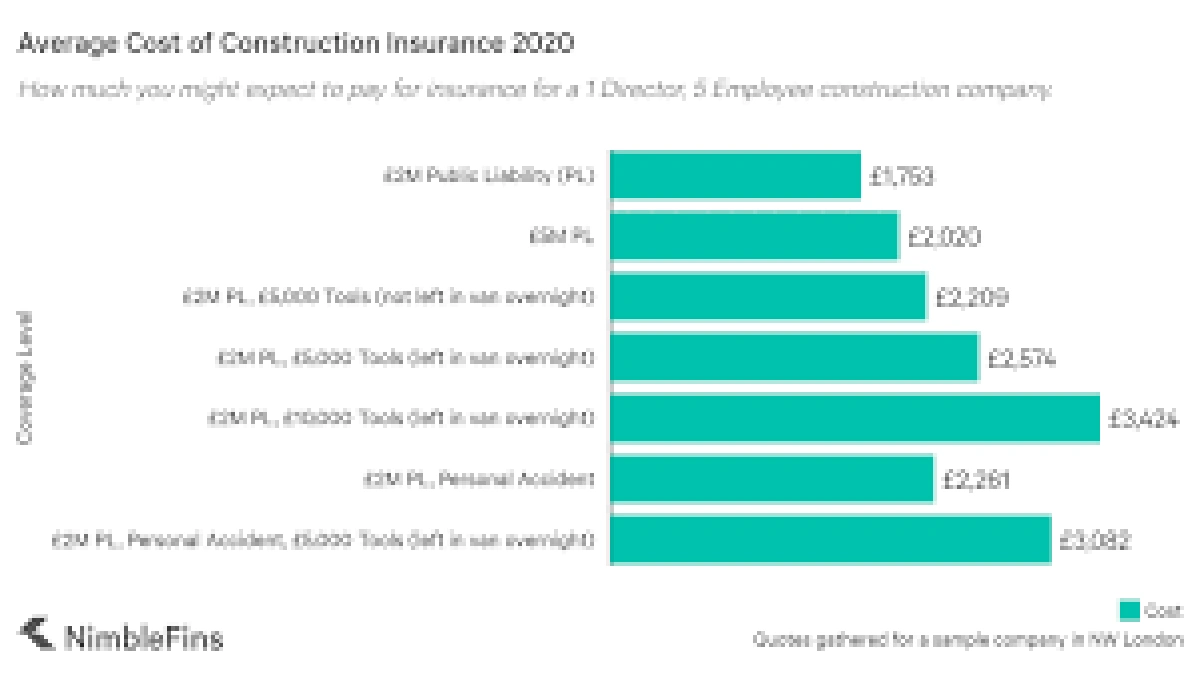

Public Liability Insurance | Your Shield Against Everyday Mishaps

This is probably the most commonly understood and often required form of public liability insurance for contractors. In essence, it protects you against claims from third parties (people who aren’t your employees) for injury or damage to their property, caused by your business activities. Imagine you’re an IT consultant, and you accidentally spill coffee on a client’s server, causing significant damage. Or perhaps you’re a self-employed plumber, and a pipe bursts during your work, flooding a customer’s kitchen. Public liability insurance steps in to cover the costs of compensation, legal fees, and expenses. It’s truly non-negotiable if you interact with the public or work on client sites. Most clients, especially larger ones, will insist on seeing proof of adequate public liability insurance before you even set foot on their premises.

Professional Indemnity Insurance | Protecting Your Expertise (and Your Wallet)

Now, this one is crucial for anyone offering advice, design, or services based on their professional expertise. If you’re a consultant, a web developer, an architect, an accountant, or any professional whose work involves intellectual input, then professional indemnity insurance is your best friend. It covers you against claims of negligence, errors, omissions, or misrepresentation in the professional services you provide. Let’s say you provide financial advice that, due to an oversight, leads to a client’s financial loss. Or a software bug you developed causes operational issues for your client. This is where `professional indemnity for freelancers` becomes invaluable. Without it, a claim could mean hefty legal defence costs and potentially massive compensation payouts, which could easily sink your business. For many UK contractors, especially those in the professional services sector, this is as vital as the air they breathe. It protects your reputation and your livelihood from the unique risks associated with intellectual work, making `indemnity insurance UK` a critical consideration.

Employers’ Liability Insurance | A Legal Must-Have (Even for Small Teams)

This is a big one, because in the UK, if you employ anyone – even just one person, even on a temporary basis – you are legally required to have employers’ liability insurance. Yes, even if it’s just a part-time assistant, a fellow freelancer you’ve subcontracted, or someone helping you out for a few days. This insurance covers the cost of compensating employees who are injured or become ill as a result of the work they do for you. The penalties for not having `employers liability cover` when you should can be severe, running into thousands of pounds. It’s a non-negotiable legal requirement under the Employers’ Liability (Compulsory Insurance) Act 1969. For more detailed guidance, you can check the official HSE guidance . So, if you’re thinking of expanding your team, even slightly, make sure this is sorted first.

Choosing Your Armour | Practical Steps to Getting the Right Contractor Insurance

So, you understand the types of cover. Great! But how do you actually go about getting the right contractor insurance UK liability cover? It’s not about picking the cheapest option; it’s about smart protection. Here’s my advice:

- Assess Your Specific Risks: Sit down and honestly evaluate what you do. What are the potential hazards? Do you work with dangerous equipment? Handle sensitive client data? Provide high-stakes advice? Your industry, the size of your projects, and your client base all influence your `business insurance requirements UK`.

- Understand Client Requirements: Many contracts will stipulate minimum levels of UK contractor insurance requirements for public liability and professional indemnity. Always read your contracts carefully and ensure your cover meets or exceeds these.

- Consider Cover Limits: This is crucial. A policy with a £1 million public liability limit might sound like a lot, but if you’re working on a multi-million-pound project, it might not be enough. Think about the maximum potential damage or loss your work could cause.

- Compare Quotes, But Not Just on Price: Yes, `contractor insurance cost` is a factor, but don’t let it be the only factor. Look at what each policy actually covers, its exclusions, and the insurer’s reputation. A slightly more expensive policy with better coverage and a reliable claims process is almost always a smarter investment. Websites like Simply Business’s guide to contractor insurance can offer a starting point for comparing options.

- Seek Expert Advice: If you’re unsure, speak to an insurance broker who specialises in contractor or `freelancer insurance UK`. They can help you tailor a policy that fits your unique needs and budget, ensuring you get the most appropriate types of contractor liability insurance.

Remember, the goal isn’t just to buy a policy; it’s to buy peace of mind. It’s about having the confidence that if something goes wrong, you’re financially protected and can continue focusing on what you do best.

Beyond the Basics | Other Important Considerations for UK Contractors

While liability cover is paramount, it’s worth briefly touching on a couple of other insurance types that often complement your core contractor insurance UK liability cover:

- Tools & Equipment Insurance: If your livelihood depends on your tools, consider covering them against theft, loss, or damage.

- Legal Expenses Insurance: This can cover legal costs for things like contract disputes, property disputes, or tax investigations, which can be a real headache for self-employed individuals.

- Personal Accident & Sickness Insurance: As a contractor, if you can’t work, you don’t get paid. This type of insurance provides an income if you’re unable to work due to injury or illness.

When you’re looking at `how to choose contractor insurance`, remember to review your policy regularly, especially as your business grows or changes. New clients, new types of projects, or even hiring your first assistant can all trigger a need to update your cover. Don’t let your insurance become an afterthought; make it an integral part of your business strategy. It’s not just an expense; it’s an investment in your future. Consider what `self-employed liability insurance` truly means for your specific trade.

And speaking of investments, it’s always good to consider your broader financial planning. For instance, understanding the nuances of a joint life insurance policy UK comparison might seem unrelated, but it’s all part of securing your future and that of your loved ones, much like your business insurance protects your professional life. Similarly, exploring a family floater insurance premium calculator can give you insights into protecting your family’s health, ensuring holistic security.

Frequently Asked Questions About Contractor Liability Cover

What is the minimum public liability insurance for contractors?

There’s no universal legal minimum for public liability insurance in the UK, but most clients will require at least £1 million, with many asking for £2 million or even £5 million, depending on the project’s size and risk profile. Always check your contract’s specific requirements.

Do I need professional indemnity insurance if I’m a sole trader?

Absolutely. Your legal structure (sole trader, limited company, etc.) doesn’t change your liability for professional negligence. If you provide professional advice or services, professional indemnity insurance is highly recommended, regardless of whether you’re a sole trader or a larger entity.

Is employers’ liability insurance always mandatory?

Yes, if you employ anyone in the UK, even casually or on a temporary basis, you are legally required to have employers’ liability insurance. There are very few exemptions, mainly for family businesses where all employees are close family members.

How much does contractor insurance cost in the UK?

The `contractor insurance cost` varies significantly based on your profession, the level of cover you need, your claims history, and your turnover. A simple public liability policy for a low-risk trade might start from £60-£100 per year, while comprehensive packages for high-risk professions can be hundreds or even thousands of pounds. It’s essential to get tailored quotes.

Can I get contractor insurance UK liability cover quickly online?

Yes, many reputable online brokers offer instant quotes and immediate cover for various contractor insurance UK liability cover needs. However, for more complex or specialised requirements, speaking to a broker directly is often advisable to ensure you have the most appropriate and comprehensive protection.

So, there you have it. Don’t let the jargon intimidate you. Understanding your contractor insurance UK liability cover is one of the smartest moves you can make for your business. It’s not just about compliance; it’s about building resilience, protecting your hard-earned reputation, and ensuring that you can continue to do the great work you do, come what may. Get it right, and you’re not just buying a policy; you’re investing in your future. Stay covered, stay confident!