Alright, let’s grab a chai and talk business, specifically about something that keeps many small business owners up at night: business insurance costs. I mean, you’ve poured your heart, soul, and savings into building your venture. The last thing you want is an unexpected hiccup – a fire, a lawsuit, a sudden medical emergency for an employee – to derail everything. But then, there’s the nagging question: how much is this protection going to set me back? What’s the real deal with small business insurance cost?

Here’s the thing: insurance isn’t just another bill; it’s a strategic investment. Think of it as your business’s safety net, allowing you to innovate and grow without constant fear of unforeseen financial blows. It’s about securing peace of mind. And let me tell you, navigating the world of premiums, deductibles, and coverages can feel like trying to solve a Rubik’s cube blindfolded. But it doesn’t have to be. I’ve seen enough policies and spoken to enough entrepreneurs to know that with a little guidance, you can understand and manage your insurance costs effectively. We’re going to break it all down, step-by-step, to help you find that sweet spot between adequate protection and an affordable premium. This isn’t just about paying less; it’s about paying smart.

Why Even Bother? The Unseen Risks and the Real Value of Protection

Before we dive into the numbers, let’s address the elephant in the room: why do you even need business insurance? Many small businesses, especially startups, sometimes view insurance as an optional expense, a luxury even. That’s a common, yet potentially costly, misconception. The truth is, your business, no matter how small or niche, faces a myriad of risks daily. From a customer slipping on a wet floor in your boutique to a cyber-attack crippling your online operations, or even an essential piece of machinery breaking down, the potential for financial loss is immense. And let’s not forget the ever-present threat of lawsuits.

This is where different commercial insurance types come into play. You’ve got General Liability Insurance, which is like your basic shield against third-party claims for bodily injury or property damage. Then there’s Property Insurance, covering your physical assets – your office, equipment, inventory – from perils like fire, theft, or natural disasters. For those in service industries, like consultants or IT professionals, professional indemnity insurance price might be a key concern, as it protects against claims of negligence or errors in your professional services. The goal here isn’t to scare you, but to illustrate the wide net of protection that insurance casts, safeguarding your dream against a host of nightmares. Understanding these foundational needs is the first step in understanding and, ultimately, optimizing your small business insurance cost.

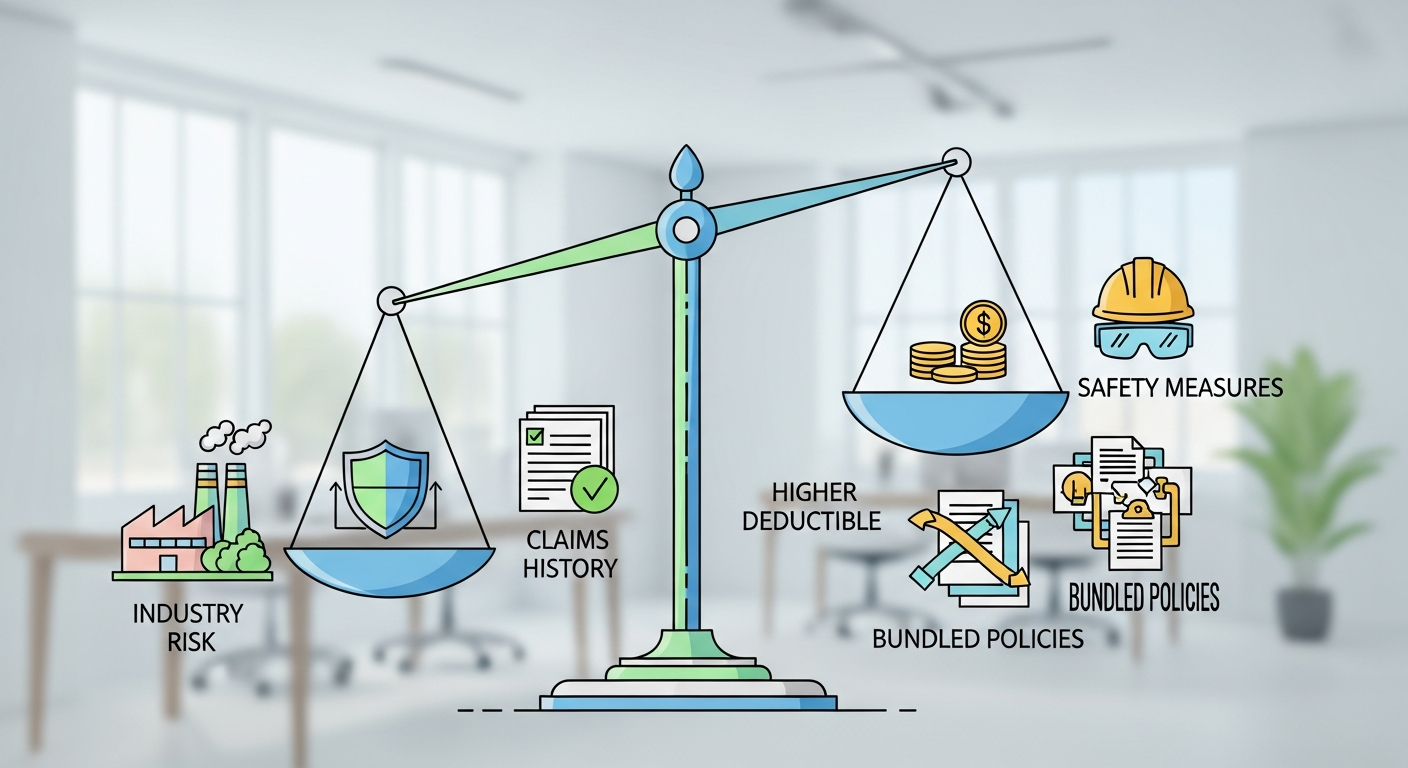

Cracking the Code: What Actually Drives Your Small Business Insurance Cost?

Alright, let’s get to the nitty-gritty. What makes one business pay X amount and another business pay Y? There’s no single magic number for small business insurance cost because, frankly, every business is unique. However, there are several universal factors affecting insurance premiums that underwriters consider. Think of it like a puzzle, where each piece influences the final picture.

- Industry and Business Type: A software development firm, for instance, typically faces different risks than a restaurant or a manufacturing unit. High-risk industries, by their very nature, will have higher premiums. A construction company will likely pay more for general liability insurance cost than a graphic design studio.

- Location, Location, Location: Operating in an area prone to natural disasters (floods, earthquakes) or with higher crime rates can push up your property insurance premiums.

- Business Size and Revenue: Generally, larger businesses with higher revenues, more employees, and extensive assets tend to have higher overall insurance costs because their potential for loss is greater.

- Number of Employees: More employees often means higher risk, especially when considering workers’ compensation or employee insurance for small business policies.

- Claims History: If your business has a history of frequent claims, insurers will see you as a higher risk, which will undoubtedly increase your premiums.

- Coverage Limits and Deductibles: This is a big one. Higher coverage limits (the maximum an insurer will pay) mean higher premiums. Conversely, choosing a higher deductible (the amount you pay out-of-pocket before insurance kicks in) can lower your premium, but you take on more initial risk.

- Risk Management Practices: Businesses that actively implement risk management for small businesses – like robust safety protocols, cybersecurity measures, or employee training – might qualify for lower premiums. Insurers reward proactive prevention!

Understanding these variables is crucial. It’s not just about getting a quote; it’s about understanding why that quote is what it is. For instance, if you’re concerned about your professional indemnity insurance price, consider if you can implement more stringent contract reviews or quality control processes to mitigate potential errors.

Smart Strategies for Affordable Protection: Navigating Your Options

Now that we know what drives the cost, how do we get that cost to work for us, not against us? The good news is, there are definitely ways to secure affordable business insurance without compromising on essential protection. It requires a bit of savvy, but it’s entirely doable.

- Shop Around and Compare: This might sound obvious, but it’s astonishing how many businesses just take the first quote they get. Always, always, always get multiple small business insurance quotes from different providers. Each insurer has its own underwriting criteria and risk appetite. What one considers high risk, another might view differently. Use online aggregators, work with independent brokers, and explore direct insurers.

- Bundle Your Policies: Many insurers offer discounts if you purchase multiple policies from them. This could mean combining your general liability, property, and professional indemnity into an comprehensive insurance solutions. This is often available as a Business Owner’s Policy (BOP) for eligible small to medium-sized enterprises (SMEs), and can significantly reduce your overall SME insurance plans expenditure.

- Increase Your Deductible: We touched on this earlier. If your business has a healthy cash reserve and you’re confident you can absorb a larger initial out-of-pocket expense in case of a claim, opting for a higher deductible can noticeably lower your monthly or annual premium. It’s a calculated risk, but often worth considering for affordable business insurance.

- Implement Robust Risk Management: This isn’t just about getting a discount; it’s about making your business safer. Install security systems, fire alarms, conduct regular safety training for employees, implement strong cybersecurity protocols, and maintain your equipment diligently. Document these efforts! Proactive measures reduce the likelihood of claims, which can lead to lower premiums over time. It shows insurers you’re a responsible operator.

- Review Your Coverage Annually: Your business isn’t static, so why should your insurance policy be? As your business grows, shrinks, or changes operations, your insurance needs will evolve. Annually review your policies with your insurer or broker. You might find you’re over-insured in some areas or under-insured in others. Perhaps you’ve outgrown your current business property insurance, or you now need new coverage for a service you’ve added.

- Seek Industry-Specific Policies: Sometimes, generic policies aren’t the most cost-effective or comprehensive. Many insurers offer specialized SME insurance plans tailored for specific industries (e.g., retail, IT, healthcare). These can often provide better coverage for common industry risks at a more competitive premium.

Beyond the Basics: Tailoring Coverage for Your Unique Venture

While the basics like general liability and property insurance are non-negotiable for most, the real finesse in managing your small business insurance cost comes from tailoring your coverage. Every business is a unique ecosystem, and your insurance should reflect that. For instance, if you operate a food delivery service, you’ll need specific commercial auto insurance. If you have valuable inventory, perhaps a robust business property insurance policy with additional endorsements for spoilage or transit is essential.

Consider the nuances. Do you have intellectual property that needs protection? Are you expanding into new markets with different legal landscapes? Do you rely heavily on specific employees whose unexpected absence could cripple operations, necessitating key person insurance? For small businesses rapidly growing, thinking about future exposures, not just current ones, is a mark of strong risk management. It’s about being proactive. Don’t just settle for standard; seek out what truly fits your unique needs. A great broker can be invaluable here, acting as your guide through the maze of options. For further reading on risk management strategies, check out resources like Investopedia’s guide to Risk Management.

Your Burning Questions, Answered

What’s the typical small business insurance cost in India?

Honestly, there’s no ‘typical’ cost. It varies wildly based on your industry, size, location, and the specific coverage you choose. A micro-enterprise might pay a few thousand rupees annually for basic liability, while a medium-sized manufacturing unit could pay lakhs for comprehensive commercial insurance covering property, liability, and employee benefits. The best way to find out is to get personalized insurance quotes.

Can I get insurance specific to my industry or niche?

Absolutely! Many insurers offer specialized SME insurance plans tailored for sectors like retail, healthcare, IT, education, and manufacturing. These often provide more relevant coverage for common risks within those industries and can sometimes be more cost-effective than generic policies.

Is business insurance mandatory for all small businesses in India?

While not all types of business insurance are mandatory for every small business, some are legally required depending on your operations. For example, Workers’ Compensation (or similar statutory employee liability) is often required if you have employees. Certain professionals might need professional indemnity insurance by their regulatory bodies. It’s crucial to check local and industry-specific regulations.

How often should I review my insurance policy?

Ideally, you should review your policy annually, or whenever there’s a significant change in your business operations. This includes expanding, reducing staff, moving locations, purchasing new assets, or changing your service offerings. Regular reviews ensure your coverage remains adequate and that you’re still getting the best value for your insurance premiums.

What happens if I under-insure my business?

Under-insuring means you haven’t bought enough coverage. If a major loss occurs, your policy might only cover a fraction of the actual damages, leaving you to bear the remaining financial burden. This can be catastrophic for a small business, potentially leading to closure. It’s a key reason why understanding your true risk exposure and adequately insuring is critical for long-term viability.

The Bottom Line: Protection, Not Just a Premium

Look, I get it. Every rupee counts when you’re running a small business. But thinking of your small business insurance cost purely as an expense is missing the bigger picture. It’s about resilience. It’s about safeguarding your assets, your employees, your reputation, and most importantly, your dream. By understanding the factors at play, actively seeking competitive quotes, and implementing smart risk management strategies, you can transform insurance from a bewildering burden into a powerful tool for growth and stability. Don’t wait for disaster to strike; be proactive, be smart, and secure your future today. Your peace of mind, and your business’s longevity, are worth every bit of that effort.