Alright, let’s be honest. The world of insurance can feel like a maze, full of jargon and numbers that make your head spin. And when it comes to something as crucial aslife insurance, the stakes feel even higher. You know you need it; you want to protect your loved ones. But then comes the big question: how much will it cost? This is where the life insurance premium calculator online steps in, and trust me, it’s not just a fancy tool – it’s your personal financial guide.

I’ve seen countless folks (and perhaps you’re one of them) get intimidated by the idea of figuring out their life insurance. They either put it off, or worse, they settle for a generic plan without truly understanding its implications. Here’s the thing: understanding your potential premium isn’t just about getting a number; it’s about gaining clarity, peace of mind, and ultimately, making an informed decision that secures your family’s future. It’s a vital part of proactive financial planning tools , especially in a dynamic economy like India’s.

This isn’t about pushing you into a sale. My goal today is to demystify the process, show you why this calculator is your best friend, and how to use it effectively to avoid paying too much or, equally critically, too little. Because getting the right life cover amount is paramount, isn’t it? Let’s dive in.

Why You Can’t Afford to Skip This Step | Beyond Just a Number

Many assume an online premium calculator is just a quick way to get a quote. And yes, it does that. But that’s like saying a car only gets you from point A to point B – it misses the entire experience! What fascinates me about the life insurance premium calculator online is its power to educate and empower you. Think of it as a simulation of your financial future.

Firstly, it brings transparency. In an age where information is king, relying on vague estimates or waiting for an agent to give you a quote can feel archaic. With a few clicks, you get a real-time estimate, allowing you to compare and contrast without any pressure. This instant feedback loop helps you grasp the correlation between different factors and the ultimate insurance policy cost . You start to see how certain choices – like policy term or sum assured – directly impact your monthly outgo.

Secondly, it helps you visualize. When you input your age, health status, and desired coverage, the calculator doesn’t just spit out a figure; it paints a picture of affordability. Perhaps you thought a certain life cover amount was out of reach, but after using the calculator, you discover a robust plan is surprisingly within budget. Or maybe you realize your initial expectation for coverage was too low, and you need to adjust upwards to truly secure your family. This process is crucial for effective insurance planning .

And let’s be frank, for many of us, the idea of discussing our mortality and financial responsibilities can be uncomfortable. The calculator offers a private, no-pressure environment to explore options at your own pace. It transforms a potentially daunting conversation into an accessible, informative exercise. This is especially true for those exploring a term insurance premium calculator , which often provides straightforward, budget-friendly options for substantial coverage.

The Magic Behind the Machine: How the Life Insurance Premium Calculator Works

So, you’re ready to dive in. You’ve found a good life insurance premium calculator online on a reputable insurer’s website (or even a reliable aggregator likeEtmhtml5game Insurance). But what exactly is happening behind that sleek interface? It’s not magic, it’s mathematics and actuarial science at play!

At its core, the calculator takes the information you provide and runs it through complex algorithms. These algorithms are built upon vast datasets of mortality rates, investment returns, and administrative costs. Essentially, the insurer is trying to predict how likely they are to pay out a claim on your policy and how much they need to charge you to cover that risk and still make a profit. It’s a careful balance of risk assessment and financial projection.

When you input your age, gender, lifestyle habits, and health information, the calculator assesses your individual risk profile. Younger, healthier individuals typically pose less risk, leading to lower premiums. Conversely, someone older or with pre-existing conditions will generally face higher premiums. This personalized assessment is what makes these calculators so valuable – they move beyond generic pricing to give you an estimate tailored to you.

It’s important to understand that while these calculators provide accurate estimates, they are not always final quotes. The final premium might vary slightly after a thorough underwriting process, which could involve medical tests or detailed health declarations. However, the calculator gets you remarkably close, often within a few percentage points of the final figure, making it an excellent starting point for your online insurance comparison .

Unpacking the Variables: Factors Affecting Premium (and How to Influence Them)

Alright, this is where the plot thickens. Knowing what factors influence your premium gives you a strategic edge. It’s not just about passively accepting the numbers; it’s about understanding how you can potentially optimize your insurance policy cost . Here are the key players:

- Age: This is arguably the biggest factor. The younger you are when you buy a policy, the lower your premium. Why? Because you’re statistically less likely to make a claim in the immediate future. Pro tip: Don’t delay! Getting life insurance in your 20s or early 30s can lock in significantly lower rates for the long term.

- Gender: In India, women generally have a longer life expectancy than men, which often translates to slightly lower life insurance premiums for them.

- Health Status: Your current health and medical history play a huge role. Conditions like diabetes, heart disease, or even being overweight can increase your premium. Be honest about your health when using the calculator, as misrepresentation can lead to claim rejection later.

- Lifestyle: Smoking and alcohol consumption are red flags for insurers. Smokers, for instance, typically pay substantially higher premiums due to increased health risks. Certain dangerous occupations or hobbies might also impact your rates.

- Sum Assured (Life Cover Amount): This is the payout your nominees receive. Naturally, a higher death benefit calculation (a larger sum assured) means a higher premium. You need to balance your family’s financial needs with your affordability.

- Policy Term: How long do you want the coverage to last? A longer policy term generally means higher overall premiums, as the insurer is covering you for a greater duration.

- Type of Policy: A pure protection plan like a term insurance policy will have significantly lower premiums for the same sum assured compared to an endowment or ULIP plan that combines insurance with savings or investment components. A term insurance premium calculator will often show you just how affordable pure protection can be.

- Premium Payment Frequency: While not a huge difference, paying annually can sometimes be slightly cheaper than paying monthly or quarterly due to administrative costs.

By understanding these factors affecting premium , you can make more informed choices, perhaps by focusing on improving your health, quitting smoking, or simply buying earlier in life to secure a more affordable life cover .

Your Step-by-Step Guide to Getting Accurate Online Premium Quotes

Ready to get a precise estimate? Here’s how you typically use a life insurance premium calculator online effectively, ensuring you get meaningful online premium quotes :

- Choose a Reliable Platform: Stick to official insurer websites or well-known, reputable insurance aggregators. This ensures the data and algorithms are accurate and up-to-date with current IRDAI regulations. For instance, the IRDAI website itself provides information on regulations, which helps understand the context.

- Input Basic Personal Details: You’ll start with your age (or date of birth), gender, and sometimes your marital status. Accuracy here is key, as these are fundamental in risk assessment.

- Provide Health & Lifestyle Info: Be honest about whether you smoke or consume alcohol. Declare any existing medical conditions truthfully. This is crucial for accurate quotes and to avoid complications during claims.

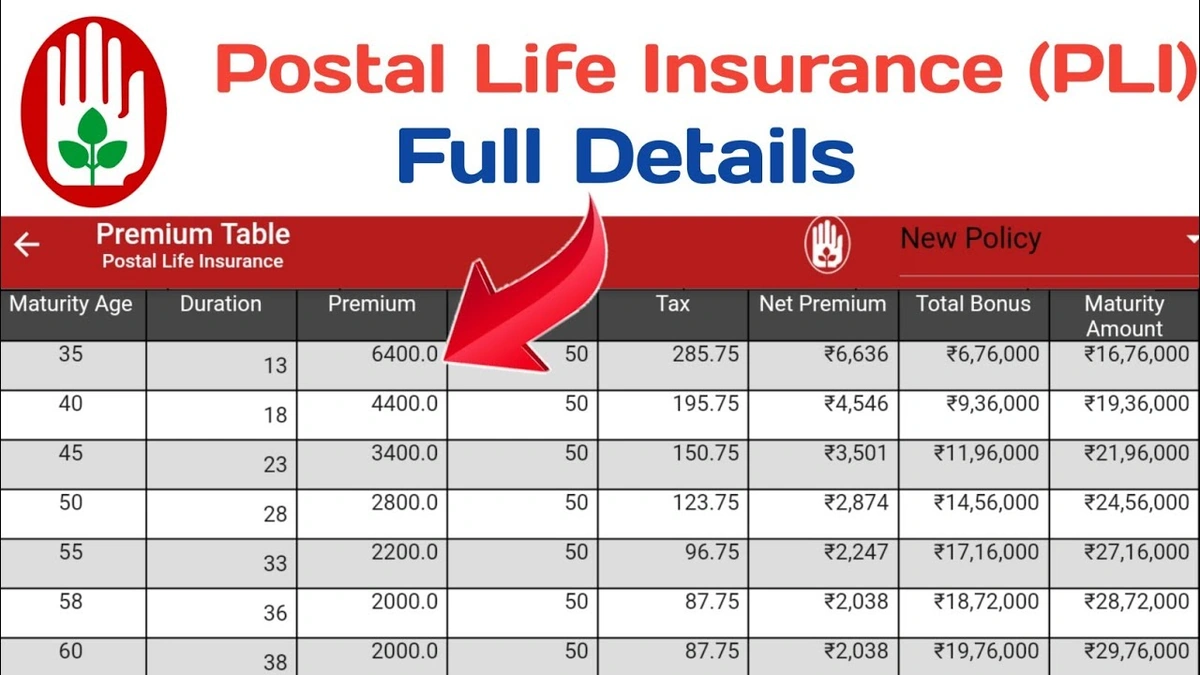

- Select Desired Coverage (Sum Assured): This is the big one. How much do you want your family to receive if something happens to you? Think about your outstanding loans, your family’s living expenses, future goals (child’s education, marriage), and inflation. This directly impacts your death benefit calculation.

- Choose Policy Term & Type: How long do you need coverage? And are you looking for a pure protection plan (like term insurance) or something with savings benefits? Most calculators allow you to toggle these options.

- Explore Riders (Optional): Many policies offer ‘riders’ – add-on benefits like critical illness cover, accidental death benefit, or waiver of premium. While these increase the premium, they can significantly enhance your policy’s protective scope. Experiment with them to see the cost impact.

- Review and Compare: The calculator will generate an estimated premium. Don’t stop at just one! Use it on multiple platforms or adjust variables to compare different scenarios. This is where online insurance comparison becomes truly powerful for finding the best life insurance India offers.

Remember, this is about personalized planning for your secure family future . Take your time, understand each input, and don’t hesitate to experiment with different combinations.

Common Mistakes to Avoid (and How to Ensure Your Life Cover Amount is Right)

Even with such a user-friendly tool, people often make a few missteps. Knowing these can help you get the most out of your life insurance premium calculator online :

- Underestimating Coverage Needs: This is perhaps the most critical error. Many people opt for a low life cover amount just to keep premiums down. But think about your family’s needs for at least 10-15 years, accounting for inflation, loans, and major life events. A good rule of thumb often suggested by financial advisors in India is 10-15 times your annual income.

- Being Dishonest About Health/Lifestyle: It might seem tempting to omit that smoking habit or a minor health issue to get a lower premium. Don’t do it! Insurers conduct background checks, and if discrepancies are found during underwriting or, worse, at the time of a claim, your policy could be invalidated. Honesty is always the best policy here.

- Not Comparing Enough: Different insurers have different risk appetites and pricing models. A premium that seems high from one insurer might be significantly lower from another for similar coverage. Always use 2-3 calculators from different providers or a reliable aggregator for comprehensive online premium quotes.

- Ignoring Riders: While they add to the premium, critical illness or accidental death riders can offer crucial protection for specific scenarios that a basic policy might not cover. Don’t dismiss them outright; consider your personal risks.

- Delaying Purchase: As we discussed, age is a primary factor. Waiting even a few years can noticeably increase your premiums. The best time to buy life insurance was yesterday; the next best time is today.

The life insurance premium calculator online is a powerful ally in your quest for financial security. Use it wisely, understand its nuances, and you’ll be well on your way to securing an affordable life cover with optimal insurance policy benefits for your future financial security .

Frequently Asked Questions About Life Insurance Premiums

What factors affect my life insurance premium?

Your life insurance premium is primarily influenced by your age, gender, health status (including lifestyle choices like smoking), the sum assured (coverage amount), and the policy term. The type of policy you choose (e.g., term, endowment) also plays a significant role in the overall insurance policy cost .

Can I get a final premium quote using an online calculator?

An online premium calculator provides a highly accurate estimate, often very close to the final premium. However, the final quote might be confirmed after a complete underwriting process by the insurer, which could include medical examinations or detailed health declarations. It’s a fantastic starting point for budgeting and comparison.

Why are premiums lower for term insurance compared to other policies?

Term insurance is a pure protection plan, meaning it only provides a death benefit if the policyholder passes away during the policy term. It does not have a savings or investment component. This focus on pure risk cover makes its premiums, as seen through a term insurance premium calculator , significantly lower for a given life cover amount compared to plans that also build cash value or offer investment returns.

Is it better to pay my premium monthly or annually?

While monthly payments offer greater flexibility, paying your premium annually can sometimes result in a slightly lower overall cost due to reduced administrative overhead for the insurer. Always check the annual payment option when using a life insurance premium calculator online to see if there’s a saving.

How much life cover should I opt for?

The ideal life cover amount depends on your individual circumstances, including your annual income, outstanding debts, dependents’ future needs (education, marriage), and inflation. Financial experts often suggest a cover of 10-15 times your annual income. Using the life insurance premium calculator online can help you simulate different coverage amounts against their respective premiums to find what’s right for your secure family future .

So, there you have it. The life insurance premium calculator online isn’t just a tool; it’s a gateway to understanding, planning, and truly securing your legacy. Don’t let uncertainty hold you back from making one of the most important financial decisions of your life. Go ahead, give it a try – you might be surprised at how clear your path to a protected future can become.