Alright, let’s talk about something incredibly important, yet often surprisingly confusing: life insurance payout options explained USA . You’ve done the responsible thing, bought a policy, and perhaps even paid premiums for years. But when the time comes when a loved one passes away understanding how that money actually reaches the beneficiaries can feel like navigating a maze. And let’s be honest, at that difficult moment, the last thing anyone needs is more confusion. So, let’s cut through the jargon and get down to brass tacks. I’m here to walk you through the common wayslife insurance beneficiariesreceive funds in the U.S., helping you make informed decisions now, or understand what to expect later.

Here’s the thing: most people assume a life insurance payout is a simple lump sum. And often, it is! But what if I told you there are other ways that money can be distributed, each with its own quirks and benefits? Understanding these settlement options life insurance offers isn’t just for the policyholder; it’s crucial for beneficiaries too. It can impact everything from tax implications to long-term financial stability. So, buckle up, because we’re going to demystify this together, step-by-step.

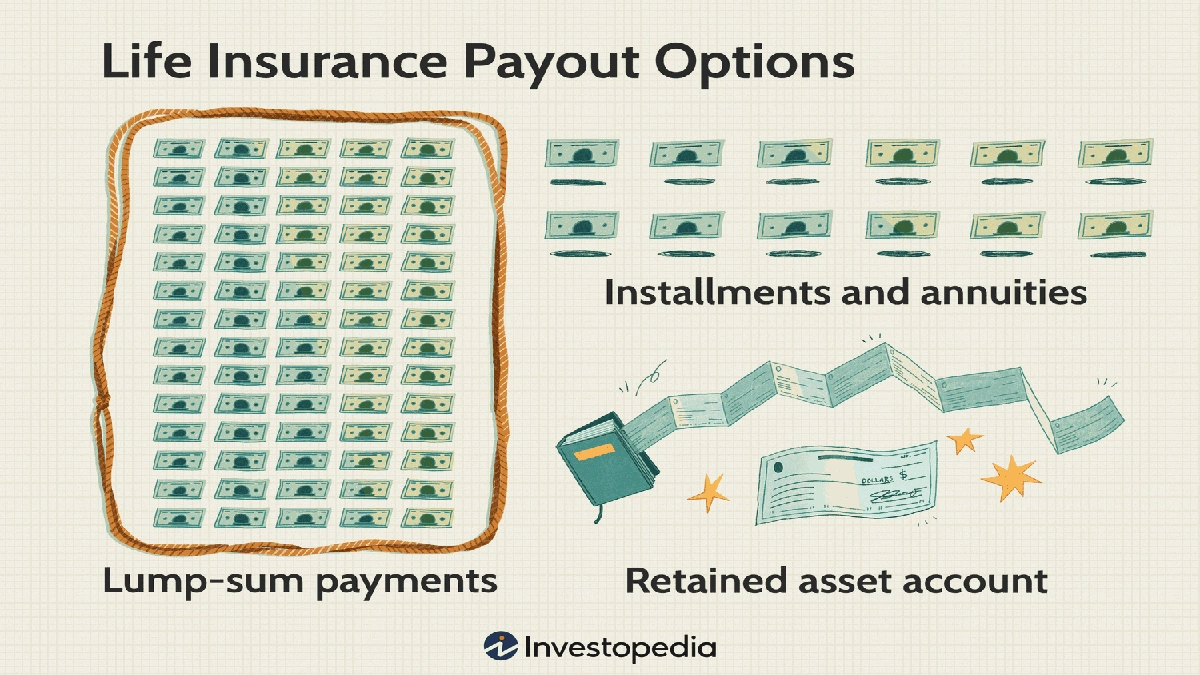

The Grand Entrance | The Lump Sum Payout

When you picture a life insurance payout, this is probably what comes to mind: a single, substantial payment made directly to the beneficiary. It’s the most straightforward and, frankly, the most common option. The insurance company verifies the claim, processes the paperwork, and then cuts a check (or initiates a direct deposit) for the full death benefit amount. Simple, right?

Why it matters: The biggest advantage of a lump sum is immediate access to all the funds. This can be incredibly helpful for covering immediate expenses like funeral costs, medical bills, or outstanding debts. It also gives the beneficiary complete control over the money. They can invest it, pay off a mortgage, or use it for whatever financial needs arise. This direct control is why many people, especially those with financial savvy or immediate cash needs, prefer it. However, with great control comes great responsibility. Managing a large sum of money suddenly can be overwhelming, and without proper planning or guidance, it could be mismanaged.

From my experience, a common mistake I see people make is not considering the beneficiary’s financial literacy. If you’re designating someone who isn’t comfortable managing large sums, a lump sum might not be the most beneficial option for them, even if it seems simplest on paper. It’s worth a conversation, perhaps with a financial advisor, to truly understand the implications of this primary death benefit distribution method.

Beyond the Big Check | Installment Payouts

Now, let’s explore alternatives to the lump sum. Insurance companies often provide several installment options, designed to offer a more structured approach to receiving the death benefit. These can be particularly appealing if the goal is to provide a steady income stream rather than a one-time windfall.

1. Fixed-Period Installments

With this option, the death benefit, along with any accrued interest, is paid out in equal installments over a specified period. Think of it like a personal annuity. For example, a $500,000 policy might be paid out over 10 years, meaning the beneficiary receives a set amount each month or year for that decade. The longer the period, the smaller the individual payments will be, but the total amount received will be higher due to interest.

The Gist: This is excellent for beneficiaries who need predictable income for a defined period, perhaps to replace lost earnings or support dependents through college. It removes the immediate pressure of investing a large sum and can prevent impulsive spending. However, the downside is that the beneficiary doesn’t have access to the full principal immediately. If an unexpected large expense arises, they might not be able to tap into the remaining funds.

2. Fixed-Amount Installments

Here, the beneficiary decides how much they want to receive in each installment, and the payments continue until the entire death benefit (plus interest) is exhausted. So, instead of choosing a period, you choose a payment amount. This offers a bit more flexibility, as the beneficiary can adjust the payment amount if their needs change, though typically within certain limits set by the insurer.

The Lowdown: This option offers more control over the payment size, which can be great for budgeting. It’s a good choice if you know you need a certain amount each month to cover living expenses but aren’t sure how long those needs will last. The risk, of course, is that if the chosen amount is too high, the funds could run out sooner than anticipated. It requires a bit of foresight andcareful financial planning.

3. Life Income Option (Annuity)

This is where things get really interesting, especially if you’re thinking long-term. Under a life income option, the death benefit is converted into an annuity, providing the beneficiary with regular payments for the rest of their life. The payment amount is determined by factors like the beneficiary’s age, gender, and the current interest rates at the time of the payout.

My Take: This is a powerful choice for beneficiaries who need guaranteed income and are concerned about outliving their funds. It offers unparalleled peace of mind. However, there’s a trade-off: if the beneficiary dies soon after payments begin, the remaining principal (if any was guaranteed) might revert to the insurer or be paid to a secondary beneficiary, depending on the specific annuity terms. It’s a classic lump sum vs annuity life insurance debate, and the right answer depends entirely on individual circumstances and risk tolerance. It’s often compared to a pension, providing a reliable stream of income no matter how long the beneficiary lives. This makes it a strong contender for those looking for secure, lifelong financial support, rather than a large sum they need to manage themselves.

Navigating the Payout Process | Understanding Your Rights

Regardless of the chosen payout method, the life insurance claim process generally follows a similar path. First, the insurer needs to be notified of the policyholder’s death. This usually involves submitting a claim form and a certified copy of the death certificate. The company will then review the claim, verify the beneficiary, and ensure all policy conditions were met. This typically takes a few weeks, but can sometimes extend to months if there are complexities or missing documentation.

What often goes unsaid, but is incredibly important, is that beneficiaries usually have a choice in how they receive the payout, even if the policyholder initially selected a default. While some policies might specify a particular payout option, many insurance companies allow the beneficiary to elect a different method after the death of the insured. It’s always worth asking the insurer about all available understanding life insurance payouts settlement options when filing a claim.

Trustworthiness comes into play here: while the insurance company wants to fulfill its obligation, they also have their processes. Don’t be afraid to ask questions, seek clarification, and even consult with a financial advisor or an attorney specializing in insurance claims if you feel overwhelmed. This is your right, and it’s about ensuring your financial well-being during a challenging time. It’s also crucial to be aware of the typical timeframes for processing claims. While state laws vary, most insurers are required to pay out within a certain period (e.g., 30 days) once all necessary documentation is received and approved. Delays might incur interest, so knowing your rights is key.

The Fine Print | Tax Implications and Other Considerations

Now, let’s talk about something nobody loves but everyone needs to understand: taxes. Generally speaking, the death benefit proceeds from a life insurance policy are income tax-free for the beneficiary in the U.S. This is a huge advantage and a key reason why life insurance is such a valuable financial planning tool. However, there are nuances:

- Interest Income: If the death benefit is paid out in installments, any interest earned on the unpaid balance is taxable. So, while the principal is tax-free, the growth on that principal is not.

- Estate Taxes: While usually not an issue for beneficiaries directly, if the policyholder owned the policy at the time of their death and the estate is large enough, the death benefit could be subject to federal or state estate taxes. This is where complex planning tools like irrevocable life insurance trusts (ILITs) come into play, but that’s a topic for another day (and perhaps a chat with an estate attorney!).

- Accelerated Death Benefits: If the policyholder accessed a portion of their death benefit while alive (e.g., for terminal illness), that portion might have different tax implications.

Another consideration is the role of a contingent beneficiary. This is the person or entity designated to receive the death benefit if the primary beneficiary is no longer living at the time of the insured’s death. Always make sure both primary and contingent beneficiaries are up-to-date on your policy. I’ve heard too many stories where outdated beneficiaries led to lengthy legal battles and heartache. It’s a simple update that can save immense trouble.

Finally, considerhow different insurance products, like whole life or universal life, might have cash value components that affect the overall financial picture, though the death benefit payout options typically remain similar across policy types.

FAQ | Your Burning Questions About Life Insurance Payouts

Common Questions About Life Insurance Payouts

What is the fastest way to receive a life insurance payout?

Generally, a lump sum payment via direct deposit is the fastest way. However, the speed of the entire life insurance claim process largely depends on how quickly the beneficiary submits all required documents (death certificate, claim form) and how efficiently the insurance company processes them. Most claims are processed within a few weeks once all documentation is in order.

Can I change the payout option after the policyholder dies?

In many cases, yes! While the policyholder might have designated a default option, most insurance companies allow the beneficiary to choose a different settlement option when they file the claim. It’s crucial to discuss all available options with the insurer’s claims department before making a final decision. This flexibility is key to understanding life insurance payouts .

Are life insurance payouts taxable in the USA?

Generally, the death benefit proceeds from a life insurance policy are income tax-free for beneficiaries in the U.S. However, any interest earned on installment payouts is taxable. In rare cases, for very large estates, the death benefit might be subject to federal or state estate taxes, but this typically impacts the estate, not the beneficiary directly.

What happens if the beneficiary is a minor?

If a minor is named as a beneficiary, the insurance company cannot directly pay them. The funds are typically held in trust, or a guardian is appointed by a court to manage the money until the minor reaches the age of majority (usually 18 or 21, depending on the state). This highlights the importance of setting up a trust or naming a guardian in your will if you have minor beneficiaries, to ensure smooth death benefit distribution .

What are structured settlements life insurance?

A structured settlement, in the context of life insurance, refers to an arrangement where the death benefit is paid out in a series of periodic payments rather than a lump sum. This is essentially what we discussed with fixed-period or fixed-amount installments, designed to provide a steady income stream over time, often for long-term financial support.

The Final Word | Making Informed Choices

So, there you have it. Understanding life insurance payout options explained USA isn’t just about knowing the different names; it’s about appreciating the flexibility and strategic potential each option holds. Whether it’s the immediate power of a lump sum, the steady rhythm of fixed installments, or the lifelong security of an annuity, each choice has profound implications for the beneficiary’s financial future. My advice? Don’t leave it to chance. If you’re a policyholder, discuss these options with your beneficiaries and a trusted financial advisor. If you’re a beneficiary, don’t hesitate to ask your insurance company for a full breakdown of all available settlement options. This isn’t just about money; it’s about providing stability and peace of mind when it’s needed most. Make choices that truly serve the long-term well-being of those you care about.