Alright, let’s be honest. The world of insurance can feel like a dense jungle, especially when it comes to securing your family’s future with a partner. You’ve probably typed ” joint life insurance policy UK comparison ” into Google, only to be met with a sea of jargon and conflicting advice. It’s enough to make you want to throw your hands up and just pick the first thing you see, isn’t it? But here’s the thing: this isn’t just about ticking a box. This is about peace of mind, about protecting your loved ones, and about making sure that if the unthinkable happens, they’re financially secure. And that, my friend, is why a careful, informedcomparisonisn’t just a chore; it’s an act of love. I’m here to cut through the noise, walk you through the complexities, and help you understand exactly how to navigate the UK joint life insurance landscape like a pro.

My goal isn’t to sell you anything, but to empower you. To show you that understanding your options for life insurance for couples UK isn’t rocket science, but it does require knowing what questions to ask and what pitfalls to avoid. So, grab a cuppa, get comfortable, and let’s demystify this together, step by logical step.

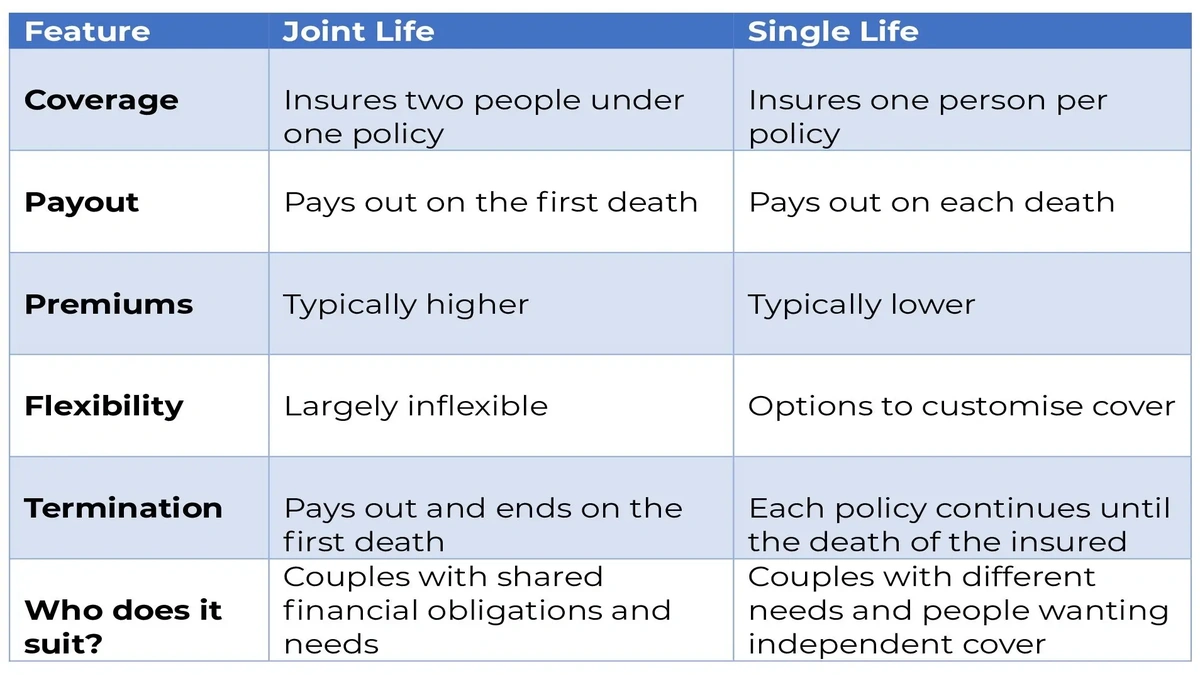

Joint vs. Single | Unpacking the Big Decision

This is often the first fork in the road, and it’s a crucial one. Should you go for a joint life insurance policy or two separate single life policy plans? On the surface, a joint policy can look like the more straightforward and, often, cheaper option. It’s one policy, one monthly payment, and it covers both of you. Simple, right? Well, yes and no. The main thing to wrap your head around is how the payout works.

A typical joint life insurance policy UK comparison will highlight that most joint policies are ‘first event’ policies. This means they pay out once – on the first death of either policyholder – and then the policy ends. Great for ensuring the surviving partner has immediate financial support, perhaps to clear a mortgage or cover living expenses. But what if the surviving partner then passes away? There’s no further payout from that specific policy. This is where the `joint vs single life insurance UK` debate really heats up. If you each have a single policy, then both policies would pay out independently, offering two separate sums to your beneficiaries.

So, when is a single life policy actually better? If you want two separate payouts, regardless of when each partner passes, or if you have significantly different health conditions that might make a joint policy more expensive, then separate policies could be the way to go. It’s also often preferred if you have very different financial obligations or different beneficiaries in mind. However, for many `life insurance for couples UK` scenarios, especially those focused on covering a shared financial burden like a mortgage, a joint policy often makes sense – but you need to understand its limitations. A common mistake I see people make is assuming a joint policy means two payouts, which, for most standard policies, simply isn’t the case.

First Event vs. Second Event | Understanding the Payout Triggers

This is where the nuances of joint life insurance really come into play. As I mentioned, most policies are designed to be `first event vs second event life insurance` policies, paying out on the ‘first event’ – meaning the first person to pass away. This is the most common type and what you’ll typically find when you start to `compare joint life insurance quotes`.

Let’s break down the implications of `first death joint life insurance`. Imagine you and your partner take out a policy. If one of you dies, the policy pays out, and the surviving partner receives the lump sum. This money can be absolutely vital for covering immediate costs, replacing lost income, or paying off a shared debt. The policy then ceases to exist. This can be perfect for couples who want to ensure that their partner is financially secure should they pass away prematurely, especially if they have children or a mortgage. The surviving partner can then decide if they need to take out a new single policy for themselves.

Now, `second death joint life insurance` is a different beast entirely, and it’s far less common for general family protection. These policies are designed to pay out only after both policyholders have passed away. Who needs this? Typically, it’s used for inheritance tax planning. For instance, if you want to ensure that your beneficiaries receive a lump sum to cover a potential inheritance tax bill when the second partner dies, this type of policy can be incredibly useful. It’s a niche product, often associated with `whole of life joint policy` structures, and definitely something to discuss with a financial advisor if it aligns with your estate planning goals. For the average couple looking for protection, you’ll almost certainly be looking at a first event policy.

Types of Joint Life Cover | Beyond the Basics

Okay, so you’ve decided on joint, and you understand the first event payout. Now, what kind of cover do you actually need? Just like single policies, joint life insurance comes in a few flavours, each designed for a specific purpose.

First up, we have `decreasing term joint life insurance`. This is the go-to option for covering a repayment mortgage. Why? Because the amount of cover decreases over time, broadly in line with your outstanding mortgage balance. The idea is that as you pay off your mortgage, you need less insurance cover. It’s usually the most affordable option for this reason, and a very popular choice for couples. It makes perfect sense to align your insurance with a debt that’s shrinking, doesn’t it?

Then there’s `level term joint life insurance`. With this, the payout amount remains the same throughout the policy term. If you take out £200,000 of cover, your beneficiaries will get £200,000 whether you pass away in year one or year twenty-nine of a thirty-year policy. This is ideal if you want to leave a fixed sum, perhaps to cover family living costs, children’s education, or to ensure a certain lifestyle is maintained, regardless of when the claim is made. It offers a consistent level of protection, which can be incredibly reassuring.

And finally, the `whole of life joint policy`. Unlike term policies that run for a set period, a whole of life insurance policy is designed to pay out whenever you die, as long as premiums are maintained. It’s essentially guaranteed to pay out eventually, making it a powerful tool for inheritance planning or ensuring a legacy. It’s typically more expensive than term insurance because the payout is a certainty, not just a possibility within a timeframe. When looking at a `joint life insurance policy UK comparison`, you’ll notice significant cost differences between these types.

Don’t forget about adding critical illness cover . Many providers allow you to add `critical illness cover joint policy` to your life insurance. This means if one of you is diagnosed with a specified critical illness (like a heart attack, stroke, or certain cancers) during the policy term, you’d receive a lump sum. This can be invaluable for covering medical costs, adapting your home, or simply replacing income if one partner can no longer work. It’s a powerful layer of protection that often gets overlooked, but it’s worth exploring theMoneyHelperfor impartial advice on this.

Navigating the Comparison | How to Find the Best Joint Life Insurance Deals

So, you’ve got a clearer picture of the different types. Now comes the practical part: how do you actually `compare joint life insurance quotes` and find the `best joint life insurance deals` without getting overwhelmed? It’s not just about the cheapest premium; it’s about value, reliability, and the right fit for your unique circumstances.

First, let’s talk about the `cost of joint life insurance UK`. Several factors play a huge role here: your age, health (medical history, current conditions), lifestyle (smoking, drinking habits, dangerous hobbies), and the amount and term of cover you choose. The longer the term and the higher the sum assured, generally, the higher the premium. Don’t be tempted to skimp on honesty here; inaccurate information could invalidate your policy later. Providers also look at your occupation – some jobs are deemed riskier than others. It’s all about assessing risk, after all.

When you `compare joint life insurance`, here are some key questions to ask:

- What exactly does the policy cover? (e.g., just death, or also critical illness?)

- What are the exclusions? (e.g., pre-existing conditions, certain activities)

- How easy is it to make a claim? (Check reviews, provider reputation)

- Can the policy be adjusted later? (e.g., increasing cover if you have more children)

- What happens if we separate? (Some policies allow you to split them into two single life policy plans, others don’t). This is particularly important for `joint life insurance for unmarried couples` who might not have the same legal protections as married couples.

To find the `best joint life insurance providers UK`, I always recommend using a reputable comparison website as a starting point, but don’t stop there. Get direct quotes from a few providers, and consider speaking to an independent financial advisor. They can offer tailored advice and access to policies not always available on comparison sites. Remember, the cheapest isn’t always the best if it doesn’t meet your needs. It’s like buying a house – you wouldn’t just pick the cheapest, would you? You’d consider its suitability, its structure, its future potential. The same meticulous approach applies here. You might also want to check out this article onhomeowners insurancefor another perspective on comprehensive protection.

FAQs | Your Burning Questions Answered

Is joint life insurance cheaper than two single policies?

Generally, yes, a joint life insurance policy designed to pay out on the first death is typically cheaper than taking out two separate single life policy plans for the same amount of cover. This is because it only pays out once. If you want two separate payouts, two single policies are usually necessary, and will cost more overall.

What happens to a joint life policy if we separate or divorce?

This depends on the specific policy and provider. Some policies allow you to split them into two individual single life policy plans, each with its own terms and premiums. Other policies may simply continue, but the remaining partner might choose to cancel it or update beneficiaries. It’s crucial to check your policy terms or speak to your provider immediately if your relationship status changes, especially for `joint life insurance for unmarried couples`.

Can we add critical illness cover to a joint policy?

Yes, many providers offer the option to add `critical illness cover joint policy` to your joint life insurance . This would mean a payout if either policyholder is diagnosed with a specified critical illness during the policy term, in addition to the life cover.

What factors affect the premium for joint life insurance?

The premium for a joint life insurance policy UK comparison is influenced by several factors, including the age and health of both applicants, their lifestyle (e.g., smoking status, dangerous hobbies), the amount of cover, the policy term, and the type of policy (e.g., `decreasing term joint life insurance`, `level term joint life insurance`, `whole of life joint policy`).

Are there any tax implications for joint life insurance payouts?

Life insurance payouts are generally paid free of income tax and capital gains tax in the UK. However, they can form part of your estate for inheritance tax purposes. To avoid this, many people place their joint life insurance policy in a trust, which ensures the payout goes directly to the beneficiaries and isn’t considered part of the estate. It’s always wise to seek professional financial advice regarding trusts and inheritance tax planning.

So, there you have it. The world of joint life insurance policy UK comparison doesn’t have to be a bewildering place. By understanding the core distinctions – joint vs. single, first event vs. second event, and the different types of cover – you’re already miles ahead. The key is to approach this with clarity, ask the right questions, and remember that this isn’t just a financial product; it’s a foundation for your family’s future. Take the time, do your research, and choose wisely. Your peace of mind, and your loved ones’ security, depend on it.