Alright, let’s talk about something incredibly important, yet often overlooked, especially here in India: your house insurance coverage . For many of us, our home isn’t just a structure of bricks and mortar; it’s a repository of dreams, memories, and a lifetime of hard work. It’s our sanctuary. Yet, when it comes to protecting this invaluable asset from the unforeseen, a surprising number of us either skimp, pick a policy without truly understanding it, or worse, avoid it altogether. And trust me, I’ve seen enough stories to know that’s a gamble you simply don’t want to take.

Here’s the thing: navigating the world ofhome insurancecan feel like deciphering an ancient scroll written in legal jargon. Policy documents can be dense, the options seem endless, and the fear of choosing wrong or paying too much is real. But what if I told you it doesn’t have to be that way? What if we could break it down, piece by piece, so you feel confident, empowered, and genuinely protected? That’s exactly what we’re going to do. Consider me your friendly guide, helping you cut through the confusion and truly understand the ‘how’ of safeguarding your home.

Why Your Home Needs More Than Just Walls | The “How” of True Protection

You’ve invested significantly in your home, right? From the foundation to the paint on the walls, every rupee signifies security and aspiration. But what about the external threats? Earthquakes, floods, cyclones – India, with its diverse geography, is no stranger to natural calamities. Beyond nature’s fury, there are man-made perils too: fires, burglaries, riots, even accidental damage. These aren’t just headlines; they’re very real risks that can turn your world upside down in an instant. This is precisely why understanding `house insurance coverage` isn’t a luxury; it’s a fundamental necessity for any homeowner.

I often hear people say, “It won’t happen to me.” Or, “My house is strong.” And while optimism is great, statistics and experience paint a different picture. The financial setback from rebuilding or replacing damaged property can be catastrophic. Think about it: an unfortunate fire or a severe flood could wipe out years of savings overnight. This is where comprehensive `home insurance plans India` step in, acting as your crucial financial safety net. They don’t prevent the event, sure, but they definitely cushion the fall, allowing you to rebuild without being financially crippled.

Decoding the Jargon | Understanding Different Types of House Insurance Policies

So, you’ve decided to look into house insurance coverage . Excellent! But then you’re hit with terms like ‘structure cover,’ ‘contents cover,’ ‘all-risk,’ ‘named perils.’ What does it all mean for you, the homeowner in India? Let’s untangle this.

Broadly, mostIndian home insurance policiesfall into categories that protect either the structure of your home, its contents, or both. Understanding these `types of home insurance policy` is your first step to informed decision-making:

- Structure Cover (Building Only): This policy protects the physical framework of your home – the walls, roof, foundations, permanent fixtures like fitted wardrobes, kitchen units, and even attached garages. If a cyclone rips off your roof or an earthquake cracks your walls, this is the cover that kicks in.

- Contents Cover: This is for everything inside your home that you’d take with you if you moved. We’re talking furniture, electronics, appliances, jewellery, clothes, and other personal belongings. Imagine a burglary – this cover would help you replace your stolen valuables.

- All-Risk Policy (Comprehensive): This is often the preferred choice as it typically covers both the structure and contents against a wide range of perils, unless specifically excluded. It offers peace of mind by wrapping everything into one neat package.

- Named Perils Policy: As the name suggests, this policy only covers damage caused by perils specifically named in the policy document. If a peril isn’t listed, it isn’t covered. This type requires careful reading of the fine print.

When you’re sifting through policies, a crucial question arises: `what does home insurance cover and not cover`? Generally, policies cover fire, lightning, explosion, aircraft damage, riots, strikes, malicious damage, terrorism, natural disasters (like floods, storms, cyclones, earthquakes – often bundled as `natural disaster coverage India`), pipe bursts, and impact damage. However, common exclusions include wear and tear, intentional damage, damage due to war or nuclear perils, and often, certain types of gradual damage like mould or pest infestations unless it’s a direct result of a covered event.

One distinction that often confuses people is `renters insurance vs homeowners insurance`. If you own your home, you’re looking for homeowners insurance. If you’re renting, you generally only need contents insurance (sometimes called renters insurance), as the landlord is responsible for the building’s structure. Simple, right?

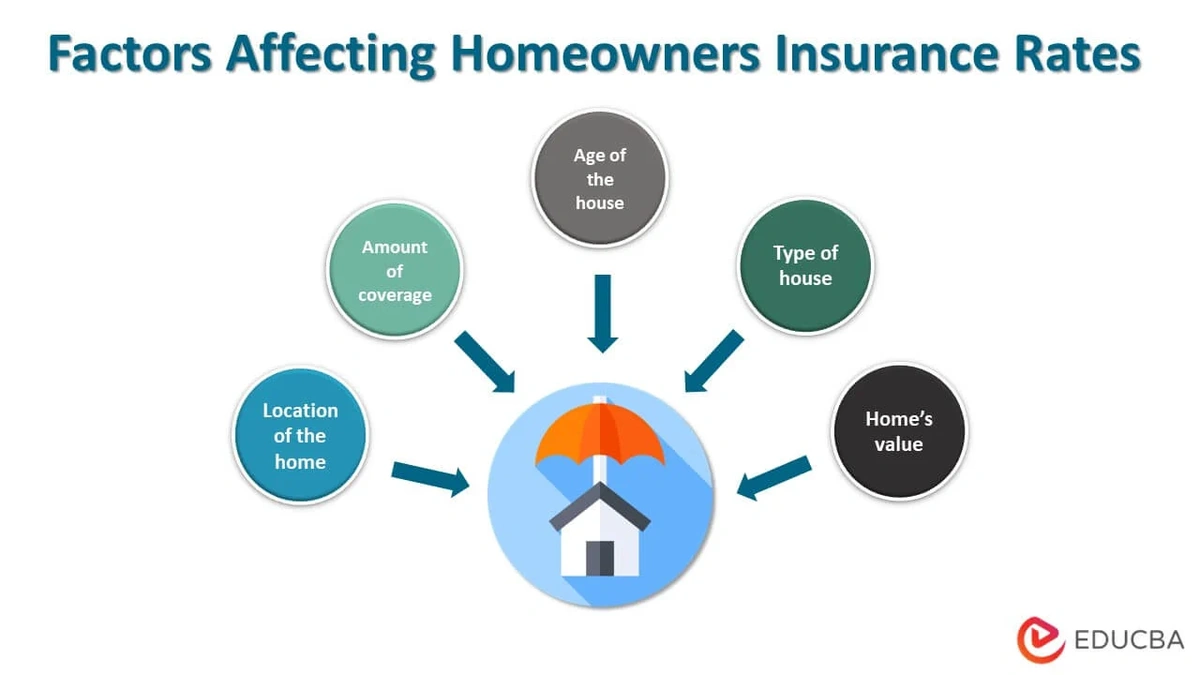

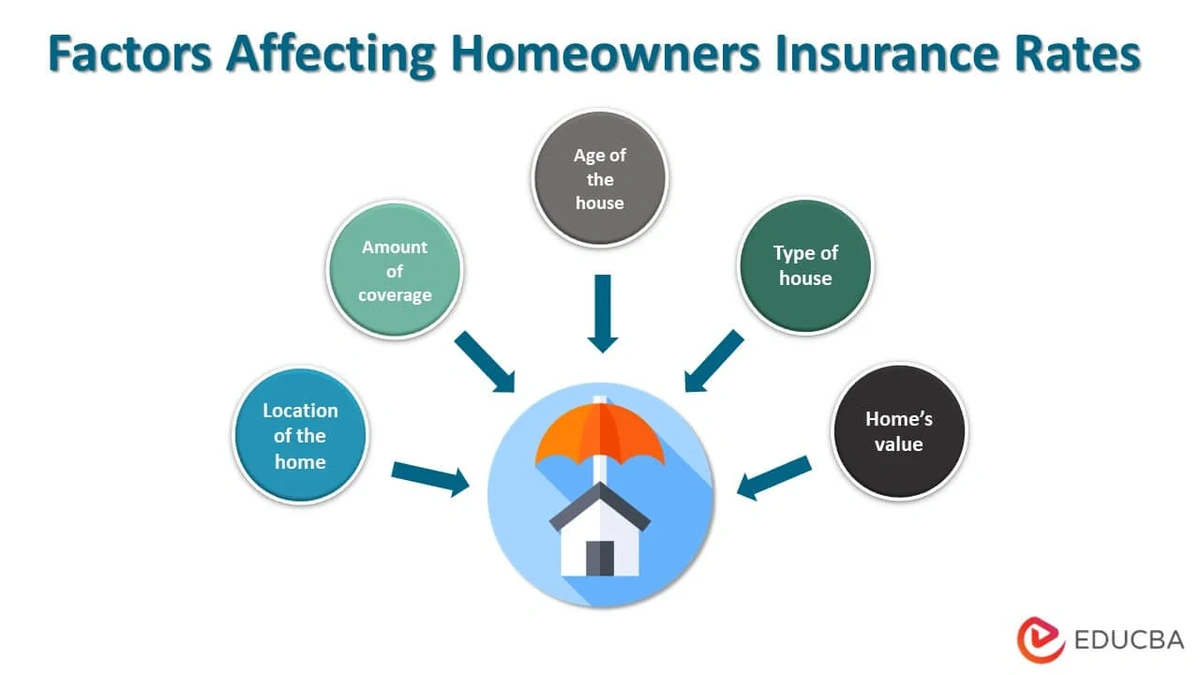

The Money Talk | What Influences the Cost of House Insurance Premium?

Okay, let’s be honest. One of the first questions on everyone’s mind is, “How much will this cost me?” The `cost of house insurance premium` isn’t a one-size-fits-all figure. It’s calculated based on several factors, and understanding them can help you optimize your spending without compromising on essential house insurance coverage .

Here are the key determinants:

- Property Value & Location: A higher reconstruction cost for your home means a higher premium. Similarly, homes in high-risk zones (e.g., flood-prone areas, seismic zones) will naturally have higher premiums due to the increased likelihood of claims.

- Type of Construction: A robust, well-maintained concrete structure will typically command a lower premium than, say, a semi-permanent house, simply because it’s more resistant to damage.

- Coverage Amount & Type: The more extensive your `types of home insurance policy` (e.g., opting for an ‘all-risk’ policy with high sum insured for contents), the higher the premium.

- Security Features: Homes equipped with advanced security systems (alarms, CCTV, strong locks) often qualify for discounts, as these features reduce the risk of burglary.

- Age of the Property: Older homes might require higher premiums if not well-maintained, as they could be more susceptible to issues like wiring faults or plumbing problems.

- Deductible: This is the amount you agree to pay out of your pocket before your insurance company steps in. A higher deductible usually means a lower premium, but remember, you’ll bear a larger initial cost during a claim.

My advice? Don’t just look at the premium alone. A cheaper policy might be cheaper because it offers inadequate `what does home insurance cover and not cover`. Focus on value – comprehensive protection that genuinely safeguards your asset – and then look for ways to reduce the `cost of house insurance premium` through smart choices like enhancing security or opting for a slightly higher deductible if you have emergency savings.

Choosing Your Shield | A Step-by-Step Guide to Selecting the Right Coverage

Now that you’re well-versed in the ‘what’ and ‘why,’ let’s get to the ‘how’ of actually choosing the best house insurance coverage for your unique situation. This isn’t just about clicking ‘buy now’; it’s about tailoring protection that truly fits.

- Assess Your Needs Thoroughly: Before even looking at policies, make a detailed inventory of your home. What’s the rebuild cost of your structure (not its market value)? What’s the approximate value of your contents? Don’t forget high-value items like electronics, jewellery, and art. Think about potential risks specific to your location. Is your area prone to floods? Earthquakes?

- Compare, Compare, Compare: Never settle for the first quote. Reach out to multiple insurance providers. Online aggregators can be a good starting point, but always verify details directly with the insurers. Look beyond just the premium. Compare the extent of `types of home insurance policy` offered, the sum insured, the deductibles, and crucially, the exclusions.

- Understand the Reinstatement Value vs. Market Value: This is a critical point. Most policies offer coverage on a ‘reinstatement value’ basis, meaning they’ll pay the cost of rebuilding your home or replacing items with new ones, without deducting depreciation. ‘Market value’ policies, on the other hand, factor in depreciation. Always aim for reinstatement value for structural coverage, as market value won’t be enough to rebuild.

- Read the Fine Print (Seriously!): I can’t stress this enough. Every policy document has terms and conditions, inclusions, and exclusions. Pay close attention to `what does home insurance cover and not cover`. Are there specific clauses for `natural disaster coverage India`? Is terrorism covered? What about alternate accommodation if your home becomes uninhabitable? A few hours spent reading now can save you immense heartache later.

- Don’t Be Afraid to Ask Questions: If anything is unclear, call the insurer or consult an independent insurance advisor. There are no silly questions when it comes to protecting your most valuable asset. Ensure you understand the `house insurance coverage` completely before signing on the dotted line.

When Disaster Strikes | Navigating the House Insurance Claim Process

This is the moment no one wants, but it’s precisely why you bought house insurance coverage in the first place. A smooth `house insurance claim process` can make a world of difference during a stressful time. Being prepared and knowing the steps can genuinely alleviate pressure.

- Immediate Action (Safety First!): Your first priority is the safety of yourself and your family. Once safe, take necessary steps to prevent further damage (e.g., turning off electricity, covering a broken window). But do NOT discard damaged property or undertake major repairs until the insurer has had a chance to inspect.

- Notify Your Insurer Promptly: Contact your insurance company as soon as possible after the incident. Most policies have a specific timeframe within which you must report a claim. Provide them with all the initial details – date, time, nature of loss, and estimated damage. Keep a record of your communication. For general insurance needs, you can always check out etmhtml5game.com/ for resources.

- Document Everything: This is absolutely crucial. Take clear photographs and videos of the damage before anything is moved or cleaned up. Keep receipts for damaged items, property documents, previous valuations, and police reports (if applicable, like in case of burglary). The more evidence you have, the smoother your `house insurance claim process` will be.

- Cooperate with the Surveyor/Assessor: The insurer will appoint a surveyor to assess the damage. Be transparent and cooperative. Provide all requested documents and answer their questions truthfully. This expert will determine the extent of loss and recommend the appropriate compensation.

- Review the Settlement: Once the assessment is complete, the insurer will offer a settlement. Review it carefully. If you believe it’s inadequate or doesn’t reflect the true extent of your loss, discuss it with the insurer. Don’t hesitate to seek clarification or even a re-evaluation if you have strong grounds.

Remember, the goal of your house insurance coverage is to restore you to your pre-loss financial position. By following these steps diligently, you can ensure you get the full benefit of your policy when you need it most.

So, there you have it. Far from being a dry, confusing topic, house insurance coverage is a dynamic shield, an investment in your peace of mind and the longevity of your most cherished asset. It’s not just about protecting four walls and a roof; it’s about safeguarding your future, your stability, and the countless memories yet to be made under that roof. Go forth, Indian homeowner, and insure wisely!

Frequently Asked Questions About House Insurance Coverage

Is house insurance mandatory in India?

Generally, house insurance for private residences is not mandatory by law in India. However, if you have taken a home loan, your lender will almost certainly require you to purchase building insurance to protect their financial interest in the property. Even without a loan, it’s highly recommended for financial security.

Can I get coverage for my valuables inside the house?

Yes, absolutely. Most comprehensive home insurance policies offer ‘contents coverage’ which specifically protects personal belongings like electronics, furniture, jewellery, and other valuables against perils like fire, theft, and natural disasters. You might need to declare high-value items separately.

How often should I review my home insurance policy?

It’s a good practice to review your policy annually, or at least every 2-3 years. This ensures that your coverage amount keeps pace with inflation, any renovations, or new high-value purchases. Your needs can change, and your policy should evolve with them to provide adequate house insurance coverage .

What is not typically covered by house insurance?

Common exclusions include damage due to wear and tear, pre-existing damage, intentional damage, damage from war or nuclear perils, and often, damage from gradual issues like mould, mildew, or pest infestations that aren’t a direct result of a covered event.

What’s the difference between market value and reinstatement value?

Market value is the cost of your property or item, factoring in depreciation (its age and wear). Reinstatement value is the cost of rebuilding or replacing your property/item with a new one of similar kind and quality, without any deduction for depreciation. For sufficient house insurance coverage , always aim for reinstatement value for your building.

What documents do I need for a claim?

For a smooth `house insurance claim process`, typically you’ll need the policy document, claim form, photographs/videos of the damage, repair estimates, invoices for damaged items, a police report (for theft/burglary), and sometimes, a fire brigade report or society letter for common damages.