Alright, let’s be honest. Few things induce quite the same level of existential dread as opening that monthly statement and seeing the line item for family health insurance monthly cost USA . It’s not just a number, is it? It’s a significant chunk of your hard-earned money, a perpetual question mark hanging over your budget. And if you’re trying to figure out what you should be paying, or why your neighbor’s family of four pays less than your family of three, well, you’re not alone. The American healthcare system, especially when it comes to insurance, can feel like a labyrinth designed by a particularly mischievous minotaur.

Here’s the thing: pinning down an exact, universal figure for family health insurance monthly cost USA is like trying to catch smoke. It’s wildly variable, influenced by a complex interplay of factors that go way beyond just ‘family’ and ‘USA.’ As someone who’s spent a fair bit of time digging into these numbers, what fascinates me is not just what people pay, but why those numbers fluctuate so dramatically. Let’s pull back the curtain, shall we? We’re going to dissect the ‘why’ behind those daunting figures, offering you a clearer picture of what you’re actually paying for and how to navigate this often-confusing landscape for more affordable family health coverage .

The Shifting Sands of Premiums | Why Costs Aren’t Static

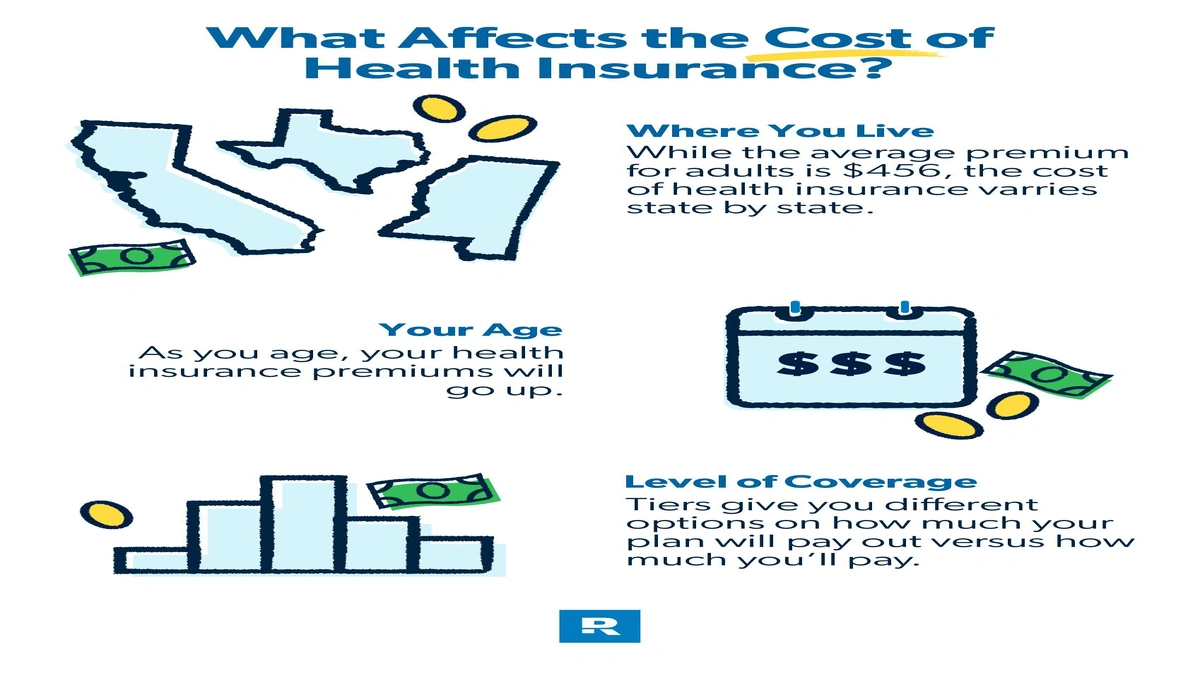

So, why isn’t there a simple price tag for health insurance plans USA ? It boils down to a few key variables, and understanding them is your first step toward financial clarity. First off, age. It’s not fair, but it’s true: generally, the older you get, the higher your premiums. Insurers see older individuals as having a higher likelihood of needing medical care, and that risk is priced in. Then there’s location. A family living in, say, New York City will almost certainly face higher premiums than one in a rural part of Nebraska. This isn’t just about the cost of living; it’s about the concentration of healthcare providers, local medical costs, and even state-specific regulations. It’s a localized market, not a national one.

Another massive factor is tobacco use. If anyone in your family (who is applying for coverage) uses tobacco, expect a surcharge. It’s a direct reflection of increased health risks. And, crucially, the number of people on your plan matters, but not always linearly. Adding a second child often doesn’t double the cost of the first, but it certainly adds to it. What’s often overlooked is the type of plan you choose. A high-deductible plan (which we’ll get to) will have a lower monthly premium than a comprehensive PPO with a low deductible. It’s a trade-off, and understanding that balance is key to managing your overall healthcare costs .

Deciphering the Jargon | Deductibles, Copays, and Out-of-Pocket Maximums

The monthly premium is just one piece of the puzzle, a down payment, if you will. The real story, the one that can truly impact your family healthcare budget , lies in the less glamorous terms: deductibles, copays, coinsurance, and out-of-pocket maximums. Many people get fixated on the premium, but as I often tell friends, a low premium with a sky-high deductible can leave you in a world of hurt if someone actually gets sick. This is where understanding deductibles really comes into play.

A deductible is the amount you have to pay out of your own pocket for covered medical services before your insurance company starts to pay. Think of it as your initial contribution. For a family plan, this can range from a few thousand dollars to well over $15,000. Only after you hit that number does your insurance kick in for most services (preventive care is usually covered before the deductible). Then you have copays (a fixed amount you pay for a doctor’s visit or prescription) and coinsurance (a percentage of the cost of a service you pay after your deductible is met). And finally, the out-of-pocket maximum – this is your safety net. It’s the absolute most you’ll have to pay for covered services in a plan year. Once you hit this, your insurance pays 100% of covered costs. Knowing this number is critical for peace of mind, especially for families with potential high medical needs. It’s a big part of the true story of US health insurance system expenses.

The Marketplace Maze | Navigating ACA and Subsidies

For many families, especially those not covered by employer-sponsored plans, the Affordable Care Act (ACA) marketplace, often found atHealthcare.gov, is the go-to. And let me tell you, it’s not always as straightforward as it seems, but it’s crucial to understand why it exists and how it can genuinely help. The ACA was designed to make health coverage plans more accessible and, yes, more affordable, particularly for those who earn too much for Medicaid but not enough to comfortably afford private insurance.

A huge component here is premium subsidies , officially known as Premium Tax Credits. These aren’t just for low-income families; many middle-income families qualify, especially after recent enhancements. These subsidies directly reduce your monthly premium, making ACA plans cost significantly less. The amount you get depends on your household income relative to the federal poverty level. It’s a sliding scale, meaning the less you earn, the more help you get. This is why two families with similar incomes might pay vastly different amounts if one qualifies for significant subsidies and the other doesn’t. It’s a game-changer for many, turning what seems like an impossible monthly bill into something manageable. Don’t assume you don’t qualify – it’s always worth checking your eligibility for these subsidies for health insurance .

Beyond the Marketplace | Employer-Sponsored vs. Private Plans

Of course, not everyone is shopping on the individual marketplace. A vast number of Americans get their health insurance USA through their employer. This is often the golden ticket, and here’s why: employers typically foot a significant portion of the premium bill, making group health insurance considerably cheaper for the employee than if they were to buy the exact same plan on their own. The employer’s contribution can vary wildly, from 50% to 90% or even more, which is why your take-home pay might feel a lot better than if you were covering the full premium yourself. This is also a good place to consider something likesmall business liability insurance USA cost, as many small businesses grapple with these same financial considerations for their employees.

However, employer plans aren’t always perfect. You might have limited choices, and if your employer’s plan isn’t great, you might find yourself weighing whether to stick with it or explore healthcare marketplace options . This is a common dilemma, and one I’ve seen many families grapple with. For example, a family of four might find that while their employer covers a good chunk of their individual premium, adding dependents makes the totalhealth insurance family 4 costthrough work prohibitively expensive. In such cases, it might actually be more cost-effective for the dependents to get coverage through the marketplace, especially if they qualify for subsidies. It’s about doing the math, comparing apples to oranges, and seeing which basket offers the best value for your unique family situation.

Strategic Savings | How to Reduce Your Family’s Healthcare Burden

So, after all this talk about why costs are what they are, what can you actually do? The good news is, you’re not entirely powerless. First, always, always compare plans. Don’t just auto-renew. Every year, during open enrollment, revisit your options. Look at the balance between premiums and those crucial out-of-pocket costs like deductibles and copays . Sometimes, a slightly higher premium can save you thousands if it comes with a much lower deductible, especially if you anticipate needing medical care.

Consider Health Savings Accounts (HSAs) if you opt for a high-deductible health plan (HDHP). These are fantastic tools for saving and paying for medical expenses with pre-tax dollars, and the money rolls over year after year. It’s like a personal rainy-day fund for your health. Also, don’t underestimate the power of preventive care. Staying healthy through regular check-ups, vaccinations, and a healthy lifestyle can prevent more serious (and expensive) issues down the line. Finally, if you’re eligible, maximize those subsidies. They exist to help, and leaving them on the table is leaving money in Uncle Sam’s pocket that could be in yours.

Frequently Asked Questions About Family Health Insurance Costs

What is the average family health insurance monthly cost in the USA?

While an average can be misleading due to huge variations, for a family of four, unsubsidized premiums on the ACA marketplace can range from $1,000 to $2,500+ per month, depending on location, age, and plan type. However, many families qualify for significant subsidies, drastically reducing their actual payment.

Can I get affordable health insurance if I’m self-employed or don’t have employer coverage?

Absolutely! The ACA marketplace (Healthcare.gov) is specifically designed for individuals and families who don’t have employer-sponsored plans. You may be eligible for premium tax credits that make coverage much more affordable.

What’s the difference between a PPO and an HMO plan?

PPOs (Preferred Provider Organizations) generally offer more flexibility, allowing you to see out-of-network doctors without a referral, but often come with higher premiums. HMOs (Health Maintenance Organizations) usually require you to choose a primary care physician (PCP) and get referrals for specialists, but often have lower monthly costs and out-of-pocket expenses.

How can I lower my family’s health insurance premium?

Consider a higher deductible plan, check your eligibility for ACA subsidies, explore different metal tiers (Bronze, Silver, Gold, Platinum – Bronze has the lowest premiums but highest out-of-pocket costs), and utilize an HSA if available. Also, ensure you’re not paying for coverage you don’t need.

What is an out-of-pocket maximum and why is it important?

The out-of-pocket maximum is the most you’ll have to pay for covered healthcare services in a year. Once you hit this limit, your insurance pays 100% of covered costs. It’s crucial because it caps your financial risk for medical expenses, providing a financial safety net against catastrophic health events.

Does my location really affect my health insurance costs that much?

Yes, significantly. Health insurance markets are largely state-specific, and even county-specific. Factors like the number of insurers in an area, local healthcare costs, and state regulations on insurance can lead to vast differences in premiums for similar plans across different regions of the USA.

The Bottom Line | Your Health, Your Wallet, Your Strategy

Navigating the family health insurance monthly cost USA isn’t just about finding the cheapest option; it’s about finding the right option for your family’s unique needs, health profile, and financial situation. It requires a bit of detective work, a willingness to compare, and an understanding of the underlying forces at play. Don’t be intimidated by the complexity. Instead, empower yourself with knowledge. Ask questions, compare plans diligently, and leverage every subsidy or savings mechanism available to you. Your peace of mind, and your bank account, will thank you for it. After all, isn’t that what genuine peace of mind is truly worth?