So, you’ve built an amazing online store. Products are flying off the virtual shelves, customer reviews are glowing, and you’re living the dream of digital entrepreneurship. It’s exhilarating, right? But here’s the thing: while you’re busy chasing that next sale, are you truly protected from the unexpected? I’ve seen countless brilliant e-commerce ventures hit a snag, not because their product wasn’t great, but because they overlooked a critical safety net: a robust ecommerce business insurance USA policy . Let’s be honest, insurance isn’t the most glamorous topic, but ignoring it is like building a skyscraper without a foundation. It’s not a matter of if something goes wrong, but when , and the implications for your growing online empire can be devastating.

What fascinates me about the e-commerce landscape is its unique blend of opportunity and vulnerability. Unlike a brick-and-mortar store, your risks aren’t just physical; they’re digital, logistical, and often, quite subtle. Today, we’re not just going to talk about what insurance policies exist; we’re diving deep into why they matter, what hidden contexts you need to be aware of, and exactly how to secure the right coverage to safeguard your hard work. Consider me your knowledgeable friend, guiding you through the often-confusing world of online business protection.

The “Why” | Beyond the Sale – Understanding Your Digital Business Risk

Running an online store feels different, doesn’t it? You might think, “I don’t have a physical storefront, so what could go wrong?” Ah, but that’s where the illusion lies. Your digital business risk is arguably more complex than that of a traditional business. Think about it: you’re dealing with customer data, shipping logistics across states (or even internationally), product sourcing, and an ever-present threat of cyberattacks. Each of these touchpoints represents a potential liability that could cost you a fortune.

For instance, imagine a data breach where customer credit card information is compromised. Or a customer sues you because a product you sold caused an injury. What about a shipment that gets lost or damaged, leading to angry customers and costly replacements? These aren’t hypothetical nightmares; they’re real-world scenarios that can cripple even the most successful online ventures. Effective online store protection isn’t just about preventing these incidents; it’s about having a plan when they inevitably occur. This is why a comprehensive ecommerce business insurance USA policy isn’t a luxury; it’s an absolute necessity for survival and sustained growth.

Decoding the Must-Haves | Key Ecommerce Insurance Policies You Need

Alright, so we’ve established the ‘why.’ Now, let’s get into the ‘what’ and ‘how.’ Navigating the various insurance options can feel like deciphering ancient scrolls, but I promise, it’s manageable once you understand the core components. Here are the essential policies that should be on every e-commerce entrepreneur’s radar:

Commercial General Liability (CGL)

This is often the bedrock of any small business insurance USA policy. CGL protects your business from claims of bodily injury or property damage that occur as a result of your business operations. While you might not have customers tripping over rugs in your virtual store, CGL can cover things like advertising injury (e.g., libel or slander in your marketing) or damage caused by your product once it’s in the customer’s hands (though product liability often takes over here). It’s broad coverage that catches many of the general unforeseen incidents.

Product Liability Insurance

If you sell physical goods, this is non-negotiable. Product liability insurance protects you if a product you sell causes injury, illness, or property damage to a customer. Even if you’re just a reseller or a dropshipper, you can still be held liable. Think of it: a faulty electronic device, a contaminated food product, or even a toy with a hidden hazard. Claims can range from medical expenses to legal fees, and they can be incredibly expensive. Understanding your exposure toproduct liability insuranceis crucial for any e-commerce business.

Cyber Insurance (or Cyber Liability Insurance)

In our digital age, this is rapidly becoming as important as CGL. Cyber insurance for online businesses is designed to protect your company from the financial fallout of data breaches, cyberattacks, and other technology-related risks. This includes costs associated with notifying affected customers, credit monitoring, legal fees, forensic investigations, and even regulatory fines. Given that most e-commerce businesses handle sensitive customer data, the risk of a breach is significant, and the consequences can be catastrophic without this coverage.

Business Interruption Insurance

What happens if your website goes down for an extended period? Or your fulfillment center experiences a fire? Business interruption insurance for e-commerce can replace lost income and cover ongoing expenses (like payroll) during a period when your business operations are disrupted by a covered peril. It’s your financial lifeline when unforeseen events temporarily shut down your ability to generate revenue.

Shipping Insurance for E-commerce

Every online store relies on shipping. And let’s face it, things go wrong in transit. Packages get lost, damaged, or stolen. While your shipping carrier might offer basic coverage, it’s often insufficient. Shipping insurance for e-commerce provides additional protection for your goods while they are in transit to your customers. This reduces your financial exposure to loss and helps maintain customer satisfaction by allowing you to quickly replace or refund damaged orders.

Navigating the “How” | Choosing the Right Ecommerce Business Insurance USA Policy

Now that you know what’s out there, how do you pick the right ecommerce business insurance USA policy for your specific needs? It’s not a one-size-fits-all situation, and honestly, that’s where many entrepreneurs get stuck. Here’s my advice:

First, thoroughly assess your specific risks. What do you sell? Where do you store inventory? Do you collect sensitive data? Do you have employees? The answers to these questions will dictate your coverage needs. For instance, a dropshipper might have less physical inventory risk but higher product liability exposure. A seller of digital goods might prioritize cyber insurance above all else.

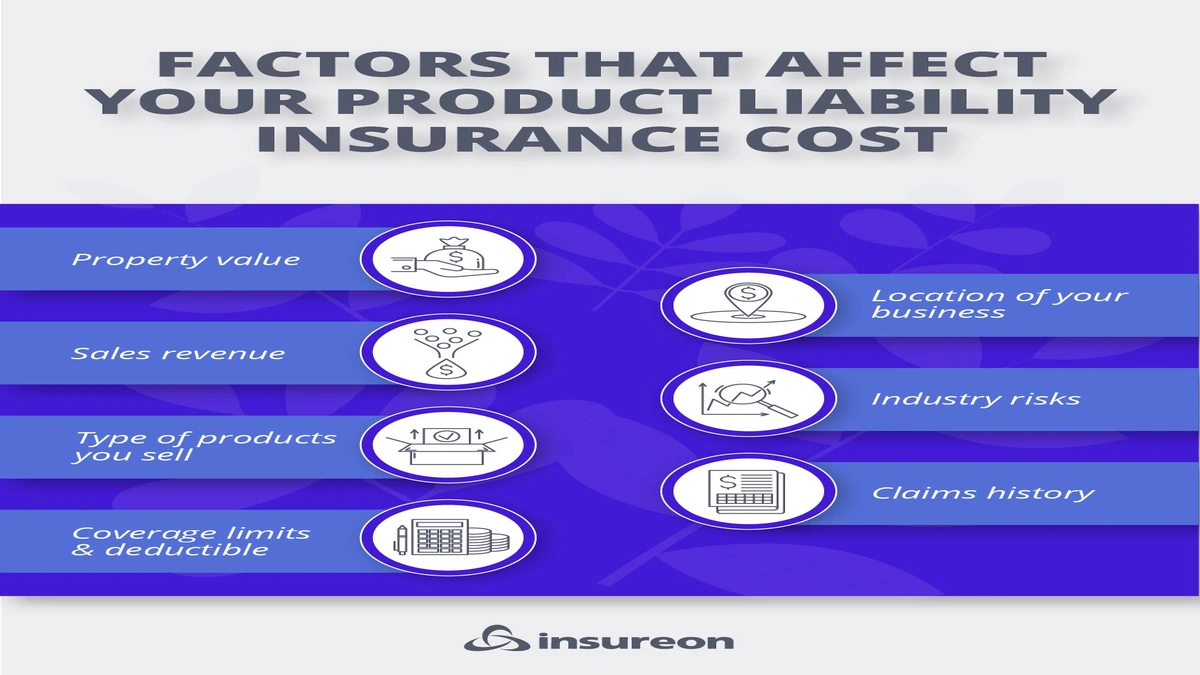

Next, consider the factors influencing your online business insurance cost . These typically include your sales volume, the type of products you sell (high-risk vs. low-risk), your claims history, and even your business location. Don’t just go for the cheapest option; focus on adequate coverage. A common mistake I see people make is underinsuring, only to find out later that their policy doesn’t cover the extent of their loss.

When it comes to finding the best ecommerce insurance providers , I recommend starting with independent insurance brokers who specialize in small businesses or e-commerce. They can shop around with multiple carriers to find policies tailored to your unique situation. Online platforms are also an option, but ensure you understand exactly what you’re buying. Remember, a good policy is an investment in your business’s longevity. This is as crucial as understanding your personal finances, much like learning abouthome insurance for first-time homeowners UK.

Common Pitfalls to Avoid (And What I’ve Learned)

It’s easy to get overwhelmed, but here’s what I’ve seen over the years that can trip up even the savviest e-commerce owners:

- Underinsuring: This is probably the biggest mistake. Thinking you’re covered only to find out your limits are too low or a specific peril isn’t included. Always err on the side of caution.

- Not Reading the Fine Print: Insurance policies are dense, I get it. But the exclusions and limitations are critical. If you don’t understand something, ask your broker to explain it in plain English.

- Assuming Coverage: Don’t assume your general business insurance automatically covers every aspect of your online store. Specifically, check for clauses related to product liability, cyber risks, and shipping.

- Ignoring Policy Reviews: Your business evolves, and so should your insurance. What was adequate last year might not be today. Review your ecommerce business insurance USA policy annually, especially if you’ve expanded your product line, increased sales, or changed your operational model.

Building trustworthiness with your customers starts with protecting your business, and that includes being prepared for the unexpected. Being proactive about your insurance needs is a sign of a responsible and forward-thinking entrepreneur.

Future-Proofing Your Online Empire | Staying Ahead of the Curve

The digital world moves at lightning speed. New technologies, new regulations, and new risks emerge constantly. Think about the rise of AI, new privacy laws, or even evolving consumer expectations for delivery and returns. Your ecommerce business insurance USA policy needs to be adaptable.

Staying informed about industry trends and potential new liabilities is key. Engage with your insurance broker regularly, not just at renewal time. Ask them about emerging risks and how your current policy might (or might not) cover them. Being proactive in adapting your coverage is how you future-proof your online empire. Just as you’d consider comprehensive options for your family’s well-being withfamily health insurance plans, your business deserves the same diligent consideration.

FAQs About Ecommerce Business Insurance USA

What is ecommerce liability insurance?

Ecommerce liability insurance refers to a range of policies designed to protect online businesses from financial losses due to claims of negligence, injury, or damage. This typically includes commercial general liability, product liability, and cyber liability insurance, all tailored to the unique risks faced by online sellers.

Do dropshippers need insurance in the USA?

Yes, absolutely. Even if you don’t physically handle inventory, as a dropshipper, you can still be held liable for product defects, advertising claims, or data breaches. Dropshipping insurance USA is crucial, particularly product liability and cyber insurance, to protect against potential lawsuits and financial losses.

How much does online business insurance cost?

The online business insurance cost varies widely based on factors like your business type, sales volume, products sold, claims history, and the specific coverages and limits you choose. Small e-commerce businesses might pay a few hundred dollars a year, while larger operations with higher risks could pay several thousands. It’s best to get custom quotes.

What is the most important insurance for an e-commerce business?

While several policies are crucial, commercial general liability and product liability insurance are often considered the most important for e-commerce businesses selling physical goods, as they cover common claims of injury or property damage. For businesses handling customer data, cyber insurance is equally vital.

Can I get business interruption insurance for my online store?

Yes, you can. Business interruption insurance for e-commerce is designed to replace lost income and cover ongoing expenses if your online store or operations are temporarily halted due to a covered event, such as a server outage, natural disaster affecting your inventory, or a cyberattack.

How do I choose the best ecommerce insurance provider?

To how to choose ecommerce insurance , look for providers or brokers who specialize in small businesses or e-commerce. Compare quotes, review policy details thoroughly, and prioritize providers with strong customer service and a good reputation for handling claims. Ensure they understand the unique risks of your online business model.

So, there you have it. The world of e-commerce is thrilling, but it’s also fraught with silent risks. Don’t let a single unforeseen event derail your dreams. Investing in the right ecommerce business insurance USA policy isn’t just about protecting your assets; it’s about buying peace of mind, empowering you to innovate, grow, and truly focus on what you do best: building an incredible online business. Stay protected, stay smart, and keep thriving!