Alright, let’s be honest. When you hear ” best car insurance policy ,” what’s the first thing that comes to mind? Probably a headache, right? Endless comparisons, confusing jargon, and that nagging fear of choosing the wrong one. But what if I told you it doesn’t have to be that way? What if, instead of just grabbing the cheapest option or sticking with your old one out of habit, you could actually understand what you’re buying and why it’s the right fit for you and your ride in India?

Here’s the thing: choosing the best car insurance policy isn’t about finding a mythical ‘one-size-fits-all’ solution. It’s about finding the policy that best serves your specific needs, your car, and your wallet, all while offering genuine peace of mind. And trust me, navigating the world of motor insurance in India can feel like a maze, but I’m here to be your friendly, slightly quirky guide.

I’ve seen countless drivers, from city commuters to highway adventurers, make common mistakes that cost them dearly later. My goal today is to arm you with the knowledge and the ‘how-to’ to avoid those pitfalls and confidently pick a policy that actually protects you when it matters most. So, let’s dive deep, shall we?

Understanding the Basics | Third-Party vs. Comprehensive & Beyond

Before we even think about comparing providers, we need to get our heads around the fundamental types of coverage. This is where many people get tripped up, and it’s absolutely crucial.

1. Third-Party Liability Insurance | The Non-Negotiable Minimum

In India, according to the Motor Vehicles Act, 1988, having aThird-Party Liability (TPL) insurancepolicy is mandatory for every vehicle on the road. No ifs, no buts. This policy covers any legal liability arising from an accident that causes injury, death, or property damage to a third party. Notice what it doesn’t cover? Damage to your car. It’s the bare minimum, a safety net for others, but not for you.

So, while it saves you from legal trouble, relying solely on third-party insurance means any damage to your own vehicle, no matter how minor, will come straight out of your pocket. Is it the ‘best car insurance policy’ for most? Probably not, unless your car is an absolute rust bucket you’re planning to scrap next month.

2. Comprehensive Car Insurance | Your All-Round Shield

Now, this is where things get interesting for the discerning driver. A comprehensive insurance policy is what most people mean when they talk about a ‘full’ cover. It not only includes the mandatory third-party liability but also provides coverage for damages to your own vehicle. Think about it:

- Damage due to accidents

- Theft (a very real concern in India!)

- Fire

- Natural calamities (floods, earthquakes, cyclones – we’ve seen enough of these, haven’t we?)

- Man-made calamities (riots, strikes, terrorism)

This is typically the smart choice for most car owners. It offers peace of mind that goes far beyond just ticking a legal box. And frankly, considering the unpredictable nature of our roads and weather, it’s often worth the slightly higher insurance premium .

The Game-Changers | Add-on Covers and Their Real Value

Okay, so you’ve decided on comprehensive. Excellent! But here’s where you truly customize your car insurance policy to make it the ‘best’ for your unique situation. Think of add-on covers as enhancements that supercharge your base policy. Many people skip these to save a few hundred rupees, only to regret it when a claim arises. Let me walk you through the ones that genuinely matter:

- Zero Depreciation (Bumper-to-Bumper) Cover: Ah, the holy grail! Normally, when you make a claim for repairs, the insurer deducts depreciation from the cost of parts. With zero depreciation, you get the full cost of repairs without any deductions for depreciation on plastic, rubber, metal parts, etc. This is an absolute must-have, especially for new cars or those up to 5-7 years old. It makes a huge difference in your claim settlement.

- Roadside Assistance (RSA) Cover: Ever been stranded in the middle of nowhere with a flat tyre or an engine issue? It’s a nightmare. RSA covers towing, minor on-site repairs, fuel delivery, and even accommodation in some cases. Given India’s varied terrains, this is a lifesaver.

- Return to Invoice Cover: In case of total loss (theft or irreparable damage), a standard comprehensive policy gives you the Insured Declared Value (IDV) of your car, which is its depreciated market value. Return to Invoice ensures you get the original invoice price of your car (including registration and road tax). For brand new cars, this is invaluable. It helps you buy a new car of the same make and model.

- Engine Protection Cover: Critical for areas prone to flooding! Standard policies don’t always cover hydrostatic lock (damage due to water entering the engine). This add-on specifically covers engine and gearbox damage due to water ingression or oil leakage. Don’t skip this if you live in a city that sees heavy monsoons.

- No Claim Bonus (NCB) Protection: Your NCB is a discount you earn for not making claims. A substantial NCB can significantly reduce your premium. This add-on allows you to make a small claim without losing your accumulated NCB. Pretty neat, right?

Choosing the right combination of these can literally save you lakhs of rupees and endless headaches. Think about your driving habits, where you live, and your car’s age when considering these.

The ‘How-To’ of Picking the Best | Factors to Consider Beyond the Price Tag

Now that you know your options, how do you actually pick the best car insurance policy? It’s not just about the cheapest quote you find online. That’s a common rookie mistake! To genuinely compare car insurance quotes India has to offer, you need a holistic approach.

1. Insured Declared Value (IDV) | The True Value of Your Car

The IDV is the maximum sum your insurer will pay in case of total loss or theft. It’s essentially your car’s current market value, factoring in depreciation. Don’t be tempted to lower your IDV just to get a cheaper premium. While it might save you a few hundreds now, it could cost you lakhs if your car is stolen or totaled. Always ensure your IDV reflects the true worth of your vehicle.

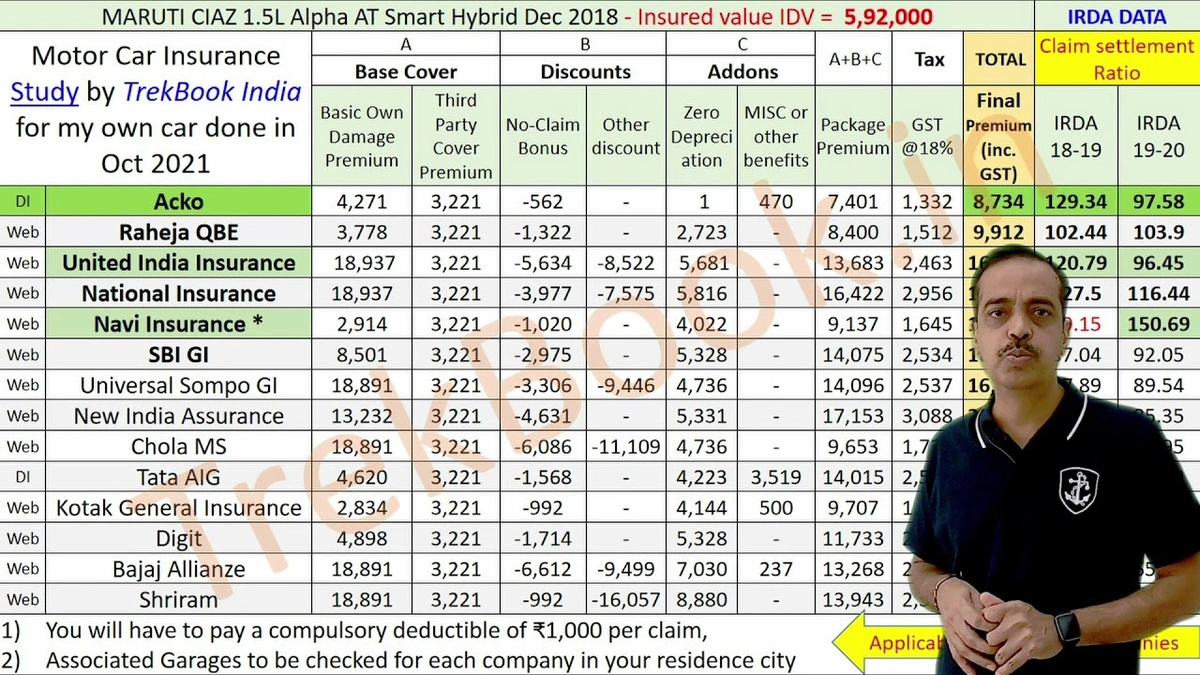

2. Claim Settlement Ratio (CSR) | The Ultimate Trust Indicator

This is arguably one of the most important metrics! The Claim Settlement Ratio tells you the percentage of claims an insurer settles in a year compared to the total claims received. A higher CSR (say, above 90-95%) indicates a more reliable insurer who is likely to honour your claims. You can usually find this data on the IRDAI (Insurance Regulatory and Development Authority of India) website or reputable insurance comparison portals. Always check this before committing to amotor insuranceprovider.

3. Network of Garages | Convenience Matters

Imagine your car breaks down in an unfamiliar city. If your insurer has a wide network of cashless garages, you can get your car repaired without having to pay upfront and then seek reimbursement. This saves you significant hassle and out-of-pocket expense during a stressful time. A large network indicates better service and convenience.

4. Customer Service and Support | Your Lifeline

When you have an accident, you’re usually stressed and need quick assistance. How responsive is the insurer’s customer service? Are they available 24/7? Do they have a user-friendly app or online portal for managing your policy document and claims? These practical aspects can make or break your experience, especially during a crisis.

5. No Claim Bonus (NCB) | Don’t Let it Lapse!

As mentioned, NCB is a reward for safe driving. It can accumulate up to 50% over five claim-free years! When you switch insurers, you can transfer your NCB. Always ensure your new insurer correctly applies your accumulated NCB. This is a huge factor in reducing yourinsurance premiumfor subsequent years.

The Smart Way to Compare and Buy | Online Car Insurance Comparison

Gone are the days of shuffling through stacks of paperwork and visiting multiple agents. The digital age has made comparing and buying online car insurance comparison a breeze. Platforms allow you to enter your car details, choose your desired coverage and add-ons, and instantly get quotes from various insurers.

But here’s my advice: don’t just pick the first one that looks good. Use these platforms to get a broad idea, then delve deeper into the fine print of 2-3 top contenders. Check their CSR, read customer reviews (especially about theirclaim process), and only then make an informed decision. Remember, the ‘best’ policy isn’t just about the lowest price; it’s about the best value, reliability, and coverage that suits you.

Frequently Asked Questions About Choosing the Best Car Insurance Policy

Q1 | What’s the main difference between third-party and comprehensive car insurance?

A1: Third-party insurance is legally mandatory and covers damages to a third party. Comprehensive insurance, on the other hand, covers both third-party liabilities and damages to your own vehicle, making it a much broader and more protective cover.

Q2 | Is a zero-depreciation add-on really worth it for my car?

A2: Absolutely, especially for newer cars (up to 5-7 years old). It ensures that during a claim, depreciation isn’t deducted from the cost of parts, meaning you get a higher claim amount and pay less out of pocket for repairs.

Q3 | How important is the Claim Settlement Ratio (CSR) when choosing an insurer?

A3: The CSR is extremely important! It indicates an insurer’s reliability and willingness to settle claims. Always aim for an insurer with a high CSR (90%+) as it suggests a smoother and more trustworthy claim process.

Q4 | Can I transfer my No Claim Bonus (NCB) if I switch car insurance companies?

A4: Yes, definitely! Your NCB is tied to you, the policyholder, not your vehicle. When you switch insurers, you can transfer your accumulated NCB, which will significantly reduce your new premium, provided you haven’t made any claims in the preceding policy year.

Q5 | What is Insured Declared Value (IDV) and why does it matter?

A5: IDV is the maximum sum assured your insurer will pay if your car is stolen or damaged beyond repair (total loss). It’s essentially the current market value of your car. Maintaining an accurate IDV ensures you receive fair compensation in the event of a total loss, so don’t undervalue it just to save on premiums.

The Final Word | Drive Smart, Insure Smarter

Choosing the best car insurance policy in India isn’t about guesswork or settling for less. It’s about being informed, understanding your options, and making a decision that truly protects your valuable asset and your peace of mind. By focusing on comprehensive coverage, intelligently selecting add-ons, and scrutinizing factors like IDV and CSR, you’re not just buying a policy; you’re investing in security. So, take your time, ask the right questions, and drive knowing you’re truly covered, no matter what surprises the road ahead brings. Happy motoring!