Let’s be honest, talking about life insurance isn’t exactly a thrilling Friday night topic. But here’s the thing: it’s one of those grown-up essentials that can literally change your family’s future. And if you’re anything like me, you’ve probably thought, “I should really look into that,” followed quickly by, “Ugh, it’s probably complicated and expensive.” Sound familiar?

What fascinates me is how many people put off getting this vitalfinancial protection UKbecause they assume it’s out of reach. Especially when we’re talking aboutUK life insurance. But what if I told you that finding low cost life insurance UK monthly plans isn’t just possible, it’s actually quite straightforward once you know the ropes? My goal today is to cut through the jargon and give you a practical, no-nonsense guide to securing that peace of mind without breaking the bank. Think of me as your knowledgeable friend, sitting across the coffee table, helping you make sense of it all.

We’re going to dive deep into the ‘how’ – how to truly find an affordable life cover UK that fits your budget and your family’s needs. Because it’s not just about finding the cheapest option; it’s about finding the right cheap option.

Let’s Talk Basics | What Even Is Low-Cost Life Insurance, Really?

When people hear “low cost,” they often jump to “cheap and nasty.” But in the world of insurance, “low cost” often means smart, efficient, and tailored. It’s about getting value for your money, not necessarily stripping away essential cover. The most common type of insurance that aligns with finding low cost life insurance UK monthly plans is what we call ‘term life insurance’.

Think ofcheap term life insurance UKlike renting a house. You pay a monthly premium for a set period (the ‘term’), and if you pass away within that term, your beneficiaries receive a lump sum. Simple, right? Unlike whole-of-life policies, which cover you indefinitely and tend to be far more expensive, term life insurance is designed to cover specific periods, typically when your financial obligations are highest – like when you have a mortgage or young children.

The beauty of monthly premiums life insurance is its accessibility. Instead of a huge upfront payment (which almost no one wants), you spread the cost, making it much easier to budget for. This is where the ‘low cost’ aspect truly shines, allowing many more families to secure crucial financial protection UK without feeling a significant pinch each month. It’s about making a vital safety net an everyday, manageable expense, not a luxury.

The ‘How-To’ of Finding Genuinely Affordable Life Cover UK | My Step-by-Step Playbook

Right, so you’re convinced you need it. Now, how do you actually find it? This is where many people get stuck, but it doesn’t have to be a maze. I’ve seen countless folks navigate this, and here’s the playbook I recommend:

- Assess Your Needs, Honestly | Before you even look at a quote, figure out what you’re trying to protect. How much debt do you have (mortgage, loans)? How many years until your kids are financially independent? What would your family need to maintain their lifestyle if you weren’t around? A common mistake I see people make is vastly underestimating this figure, thinking they’re saving money, when in reality, they’re creating a potential shortfall for their loved ones. Be realistic about the lump sum your family would actually need.

- Know What Affects Your Premium | Insurers look at a few key things: your age (younger is generally cheaper), your health (medical history, current conditions), your lifestyle (smoking, dangerous hobbies), and the length of the term. Being honest about these factors isn’t just ethical; it ensures your policy is valid when it matters most. For instance, if you’re a smoker but declare yourself a non-smoker, your family’s claim could be rejected. Not worth the risk for a few quid a month, trust me.

- Compare, Compare, Compare! This is arguably the most crucial step. Don’t just go with the first provider you see. Use comparison websites or speak to an independent financial advisor. These platforms can quickly generate numerous life insurance quotes UK tailored to your profile. It’s similar to how you might comparecar insurance price comparison– a few minutes of effort can save you hundreds, if not thousands, over the lifetime of the policy.

- Consider Your Term Length | Do you need cover for 10 years, 20 years, or until your mortgage is paid off? The longer the term, generally the higher the monthly premium. But don’t skimp here if you truly need the cover for an extended period. Balance cost with genuine need.

Beyond the Price Tag | What to Look For in the Best Budget Life Insurance Plans

Finding the absolute lowest premium isn’t always the smart play. The true value in best budget life insurance lies in the balance between cost and comprehensive cover. Let me rephrase that for clarity: a policy that’s cheap but doesn’t pay out when you need it is, in fact, the most expensive policy you could ever buy. So, what else should you be scrutinising?

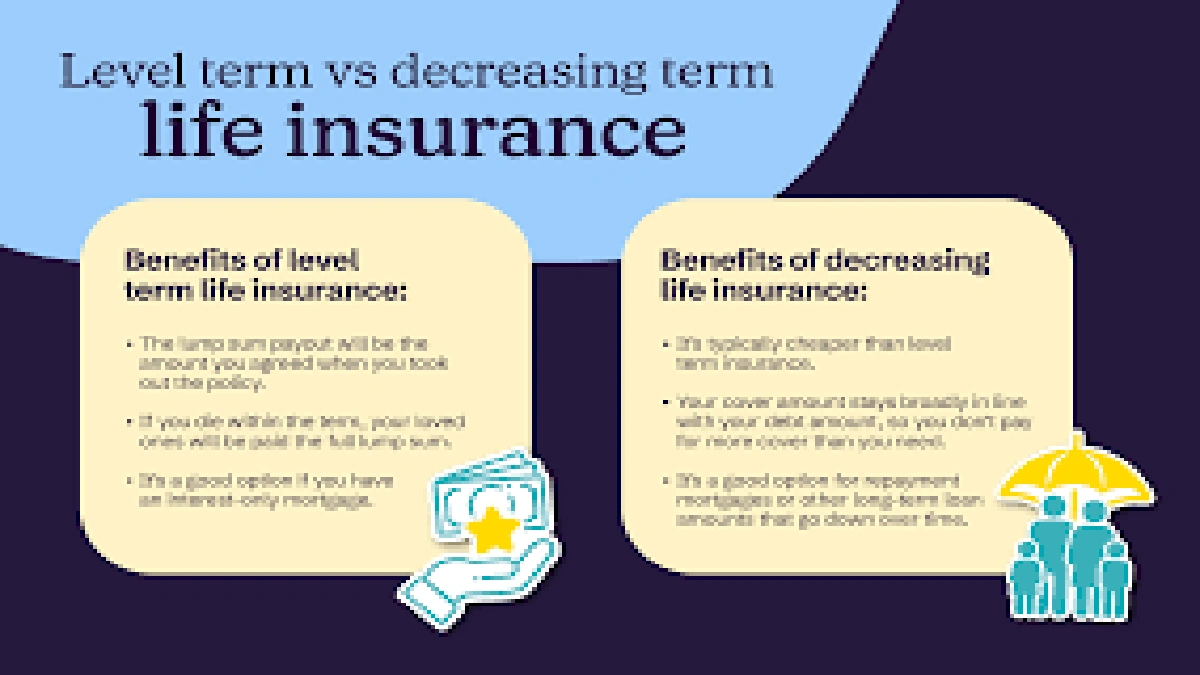

Firstly, understand the type of term life insurance you’re getting. Level term insurance means the payout remains the same throughout the policy term. Decreasing term insurance, on the other hand, sees the payout decrease over time, often designed to align with a decreasing debt like a mortgage. If your main concern is covering a specific debt that reduces over time, decreasing term can be a very effective way to get low cost life insurance UK monthly plans.

Secondly, look at the insurer’s reputation. Are they reliable? Do they have a good track record for paying claims? A quick search online for reviews and ratings can tell you a lot. While you’re focused on understanding life insurance policies, also pay attention to the small print regarding exclusions. What circumstances aren’t covered? Knowing this upfront avoids nasty surprises later.

Finally, consider any ‘riders’ or add-ons. Things like critical illness cover or waiver of premium can seem like extra costs, but they offer additional layers of financial protection UK. For example, critical illness cover pays out a lump sum if you’re diagnosed with a specified serious illness. While it increases your monthly premiums life insurance, it could be invaluable. Weigh up the potential benefit against the added cost – sometimes, a slightly higher premium for robust cover is the truly low-cost option in the long run.

Common Pitfalls & Smart Moves | Avoiding the Traps of Cheap Life Cover

Okay, you’re almost an expert! But even with the best intentions, it’s easy to stumble. Here are a couple of common traps and how to deftly avoid them:

- The ‘Set It and Forget It’ Trap | Life changes, doesn’t it? Marriages, children, new mortgages, even a significant pay rise or fall. Your low cost life insurance UK monthly plans should evolve with you. I initially thought once I had a policy, I was done. But then I realised, my needs five years ago are vastly different from my needs now. Make it a habit to review your policy every few years, or after any major life event. This ensures you still have the right level of affordable life cover UK. You might even find you can get a better deal, similar to how you’d re-evaluate yourhome insurance costannually.

- The ‘Too Good to Be True’ Trap | If a premium seems suspiciously low compared to other life insurance quotes UK, dig a little deeper. Are there significant exclusions? Is the cover amount truly adequate? Is the insurer reputable? Sometimes, the ‘cheapest’ option is cheap for a reason, and that reason might be a lack of comprehensive cover or a convoluted claims process. Always prioritise clarity and reliability.

Ultimately, securing low cost life insurance UK monthly plans is about making informed choices. It’s about empowering yourself with knowledge so you can select a policy that genuinely protects your loved ones without causing financial strain in the present. It’s not just a piece of paper; it’s a promise, a commitment to those who depend on you. And that, my friend, is truly priceless.

Frequently Asked Questions About Low Cost Life Insurance UK

Is low cost life insurance UK monthly plans always the best option?

While monthly plans offer great flexibility and affordability, the “best” option depends on your individual circumstances. For example, if you have a significant lump sum available, paying annually might sometimes offer a slight discount. However, for most people seeking affordable life cover UK, monthly payments are the most practical and manageable way to secure essential protection.

Can I get cheap term life insurance UK with pre-existing conditions?

Yes, it’s often possible to get cheap term life insurance UK even with pre-existing medical conditions, though your premiums might be higher than someone without. It’s crucial to be completely honest about your health history during the application process. Insurers will assess your specific condition and may offer terms, or in some cases, exclude claims related to that condition. Always compare life insurance quotes UK from multiple providers, as their underwriting criteria can vary.

How often should I compare life insurance quotes UK?

It’s a good idea to compare life insurance quotes UK every few years, or whenever you experience a significant life event. This includes getting married, having children, buying a new home, or even a major change in your income. Your needs evolve, and so do the market’s offerings, so regular reviews ensure you always have the most appropriate and low cost life insurance UK monthly plans.

What happens if I miss a monthly premium?

Typically, if you miss a monthly premiums life insurance payment, the insurer will send you a reminder and may offer a grace period (often 30 days) to catch up. If the payment remains unpaid after the grace period, your policy could lapse, meaning your cover would cease. It’s vital to contact your insurer immediately if you anticipate difficulty making a payment to discuss your options.

What’s the difference between level term and decreasing term life insurance?

Withunderstanding life insurance policies, level term life insurance provides a fixed payout amount throughout the entire policy term. Decreasing term life insurance, conversely, sees the payout amount gradually reduce over the policy term. Decreasing term is often chosen to cover a debt that reduces over time, like a mortgage, making it a potentially more low cost life insurance UK monthly plans option for that specific purpose.