Alright, let’s talk brass tacks. You’ve got this brilliant idea, you’re building a team, and the coffee-fueled late nights are starting to pay off. Yourstartupis taking off in the UK. Exciting, right? But then someone whispers the word ‘insurance,’ and suddenly your brain goes into a full-on fog. It feels like another bureaucratic hoop, a necessary evil, or worse, a costly distraction. And let’s be honest, who has time for that when you’re busy disrupting industries?

Here’s the thing: thinking aboutstartup business insurance UK requirementsisn’t about dread; it’s about smart business. It’s about building a robust foundation, protecting your dream, and frankly, avoiding some truly spectacular financial headaches down the line. I’ve seen countless startups make the mistake of either ignoring it or just ticking the bare minimum boxes, only to regret it when an unforeseen event strikes. So, instead of just telling you what insurance you might need, let me guide you through how to approach it, step-by-step, like a knowledgeable friend who’s navigated these waters before.

This isn’t just about compliance; it’s about strategicbusiness protection UK. It’s about understanding the hidden risks and making informed choices that safeguard your hard work. Let’s demystify this, shall we?

The Absolute Must-Haves | What the Law Demands from UK Startups

First things first, let’s tackle the non-negotiables. The UK has some clear legal requirements, especially if you’re growing beyond a solo operation. Missing these isn’t just risky; it’s illegal, and the fines can be brutal. So, what are the corestartup legal requirements UK insurance?

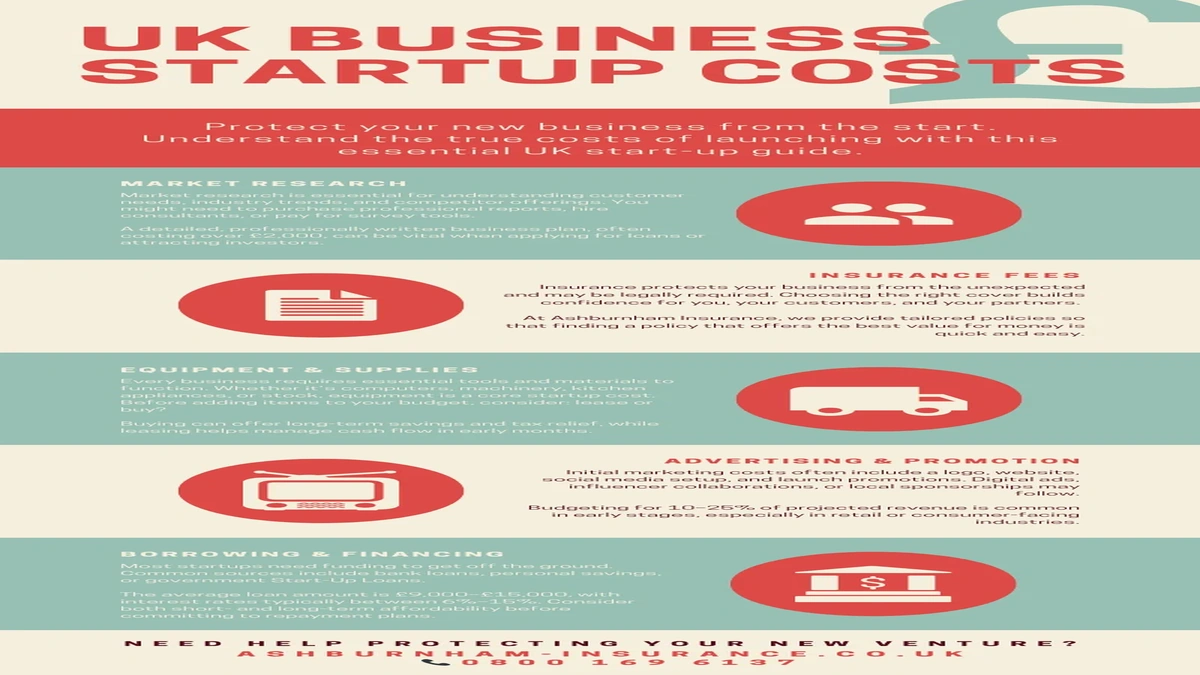

Employers’ Liability Insurance | Your First Mandatory Step

If you employ even one person – yes, even a part-timer, even an intern – you are legally required to have employers’ liability insurance UK . No ifs, no buts. This isn’t optional. It covers you if an employee gets injured or becomes ill as a result of the work they do for you. Think about it: a slip in the office, an accident with machinery, or even a stress-related illness. Without this, your business could face hefty compensation claims and significant penalties from the Health and Safety Executive.

The minimum cover is usually £5 million, but most policies offer £10 million. It’s a crucial piece of the puzzle, and frankly, it’s the bedrock of responsible employment. Don’t skimp here; it’s literally a legal obligation.

Public Liability Insurance | The Essential ‘What If’ Cover

While not strictly mandatory by law for all businesses, public liability insurance is so fundamentally important that I’d argue it should be. This covers you if a member of the public (a client, a delivery person, a passer-by) is injured or their property is damaged because of your business activities. Imagine a client tripping over a loose cable in your office, or a product you installed causing damage to their property. Without this, you’re looking at potentially crippling legal fees and compensation payouts. Most businesses, especially those interacting with the public, offering services, or having visitors, consider this a vital part of their small business insurance UK package.

Beyond the Basics | Smart Choices for Serious Protection

Once the legal boxes are ticked, it’s time to think strategically. What specific risks does your startup face? This is where the world of types of business insurance UK really opens up, and you need to tailor it to your unique operations. This isn’t about fear-mongering; it’s about pragmatic risk management for startups .

Professional Indemnity Insurance | For the Brainy Bits

If your startup offers advice, designs, or services (think consultants, web developers, marketing agencies, architects, IT services), then professional indemnity insurance UK is your best friend. It protects you against claims of professional negligence, mistakes, or errors in the services or advice you provide. Let’s say your software has a bug that costs a client revenue, or your advice leads to a financial loss for them. This policy steps in to cover legal costs and any compensation you might have to pay. It’s often a requirement in client contracts, especially for larger projects.

Commercial Property & Contents Insurance | Protecting Your Workspace

Whether you’re in a swanky co-working space, a rented office, or even working from a dedicated home office, your physical assets need protection. Commercial insurance for startups often includes cover for your equipment – laptops, servers, specialist machinery, furniture, and stock. Fire, theft, flood – these aren’t just things that happen to ‘other people.’ A single incident could wipe out your ability to operate, so ensuring your physical assets are covered is paramount. If you’re renting, your landlord will almost certainly require you to have this.

Cyber Insurance | The Modern-Day Shield

In our digital age, a cyber-attack isn’t a matter of ‘if,’ but ‘when.’ A data breach, a ransomware attack, or even a simple system outage can be devastating. Cyber insurance helps cover the costs associated with these incidents: data recovery, public relations to manage reputational damage, regulatory fines (like GDPR penalties), and even loss of income due to business interruption. For any tech-enabled startup, or one that handles sensitive customer data, this is becoming as critical as any other policy.

Navigating the Maze | How to Actually Get Insured

So, you know what you need, but how do you go about getting it without getting completely lost in jargon and endless quotes? This is where a little strategy goes a long way.

Comparing Providers for Small Business Insurance UK

There are many insurers out there offering small business insurance UK policies. Don’t just go with the first quote you get. Look at specialist providers who understand startups, as they might offer more tailored packages. Online comparison sites can be a good starting point, but remember they don’t always cover every insurer or every niche policy.

The Value of an Insurance Broker UK

Honestly, for a startup, working with an experienced insurance broker UK can be a game-changer. They understand the market, can assess your specific risks, and often have access to policies or better rates that you might not find directly. They act as your advocate, helping you understand the fine print and ensuring you don’t end up underinsured or paying for cover you don’t need. Think of them as your insurance translator and negotiator.

Assessing Risk Management for Startups

Before you even talk to an insurer, do a quick internal audit. What are your biggest risks? Data breaches? Physical accidents? Professional errors? Understanding your unique vulnerabilities helps you articulate your needs clearly to an insurer and ensures you get the right coverage. This proactive approach to risk management for startups will save you time and money.

Common Pitfalls & Pro Tips for Startup Founders

I’ve seen it all, and there are definitely some recurring mistakes that startup founders make when it comes to insurance. Avoid these, and you’ll be ahead of the curve:

- Underinsurance: Getting the cheapest policy might seem smart, but if it doesn’t adequately cover your risks, you’re essentially paying for a false sense of security. Always ensure your limits are realistic for potential claims.

- Not Reviewing Policies: Your startup is dynamic! What you needed on day one will be different on day 365. New employees, new services, new equipment – these all change your insurance needs. Review your policy at least annually, or whenever there’s a significant business change.

- Ignoring the Fine Print: Policies are full of exclusions and conditions. Take the time (or have your broker explain it) to understand what is and isn’t covered.

- Not Understanding Your Specific Needs: Generic policies rarely fit a startup perfectly. Dig deep into your specific startup business insurance UK requirements.

Remember, insurance isn’t a one-and-done purchase. It’s an ongoing part of your business strategy, evolving as you do. Treat it with the respect it deserves, and it will be there to catch you when things inevitably go sideways.

Frequently Asked Questions About UK Startup Insurance

What types of business insurance are legally required for all UK startups?

The only truly mandatory insurance for all UK businesses that employ staff is Employers’ Liability Insurance. If you don’t have employees, this isn’t mandatory. However, other insurances like Public Liability are often essential for practical protection, even if not legally required.

What’s the difference between public liability and professional indemnity insurance?

Public liability insurance covers claims from members of the public (clients, visitors, etc.) for injury or property damage caused by your business operations. Professional indemnity insurance covers claims from clients for financial losses due to mistakes, negligence, or bad advice in the professional services you provide.

Can I get cheap startup business insurance in the UK?

While you can find competitive rates for startup business insurance UK requirements , focusing solely on ‘cheap’ can be a pitfall. The goal should be adequate coverage at a fair price. Underinsurance can be far more costly in the long run. Work with a broker or compare quotes to find value, not just the lowest price.

How often should I review my insurance policy as my startup grows?

You should review your insurance policy at least annually, and certainly whenever there’s a significant change in your business, such as hiring new staff, expanding services, acquiring new equipment, moving premises, or taking on larger contracts. Your insurance needs are dynamic, just like your startup.

So, there you have it. Navigating startup business insurance UK requirements doesn’t have to be a bewildering ordeal. By understanding the legal necessities, making smart choices based on your unique risks, and leveraging the right resources, you can ensure your startup is not just innovative and agile, but also securely protected. Now, go forth and build that empire, knowing you’ve got your bases covered!