So, you’ve launched your business, haven’t you? Or maybe you’re a seasoned pro, but still, that little voice in your head whispers about ‘what ifs’. The thrill of building something, offering your expertise, it’s incredible. But then reality hits: the paperwork, the regulations, and of course, the ever-present threat of a claim. That’s where professional indemnity insurance UK cost starts to loom large in your thoughts. And let’s be honest, it can feel like trying to decipher an ancient scroll.

Here’s the thing: unlike a fixed price tag on a coffee, there’s no single answer to “how much does PI insurance cost?” It’s a bit like asking “how much does a car cost?” – well, it depends on the make, model, engine size, and whether you want heated seats, doesn’t it? My goal today is to cut through the jargon and guide you, step-by-step, through understanding and, crucially, managing your professional indemnity insurance UK cost . Think of me as your knowledgeable friend, explaining the nuances over a virtual cuppa.

What Even Is Professional Indemnity Insurance, Anyway? (And Why You Need It)

Before we dive into the numbers, let’s ensure we’re all on the same page. What precisely are we talking about? Professional indemnity (PI) insurance is a type of business insurance designed to protect professionals (and their businesses) from claims of negligence, error, or omission in the professional advice or services they provide. Imagine you’re an IT consultant, and a piece of advice you gave leads to a client losing data. Or an architect whose design has a structural flaw. Or even a marketing agency whose campaign inadvertently causes a loss of revenue for a client.

In these scenarios, your client could sue you for financial losses. Without PI insurance, you’d be personally on the hook for legal defence costs, potential damages, and settlement fees – which, let me tell you, can be absolutely crippling. This isn’t just about protecting your bank balance; it’s about safeguarding your reputation, your livelihood, and your peace of mind. Many professions, like solicitors, accountants, and financial advisors, are legally or regulatory required to have it. But even if you’re not, if you offer advice or services based on your expertise, you absolutely need to consider it.

The Elephant in the Room | Decoding Professional Indemnity Insurance UK Cost

Alright, let’s tackle the big one: the actual cost. As I mentioned, it’s not a static figure. The professional indemnity insurance UK cost is incredibly dynamic, fluctuating based on a myriad of factors. It’s like a complex algorithm, and understanding these variables is your first step to getting a fair deal. I’ve seen countless businesses get caught out simply because they didn’t know what influenced their premiums.

So, what are these mysterious factors affecting professional indemnity insurance cost ? Let’s break them down:

- Your Profession and Risk Level: This is probably the biggest factor. Are you an accountant handling sensitive financial data, or a freelance copywriter? An architect designing multi-million-pound structures, or a graphic designer creating logos? Professions with higher inherent risks (where an error could lead to significant financial loss or physical damage) will naturally command higher premiums. For example, the professional indemnity insurance for consultants UK in high-risk sectors like engineering will differ vastly from those in lower-risk fields.

- Your Turnover/Revenue: Generally, the higher your annual turnover, the higher your potential exposure to claims. Insurers see higher revenue as an indication of more clients, larger projects, and thus, a greater chance of something going awry.

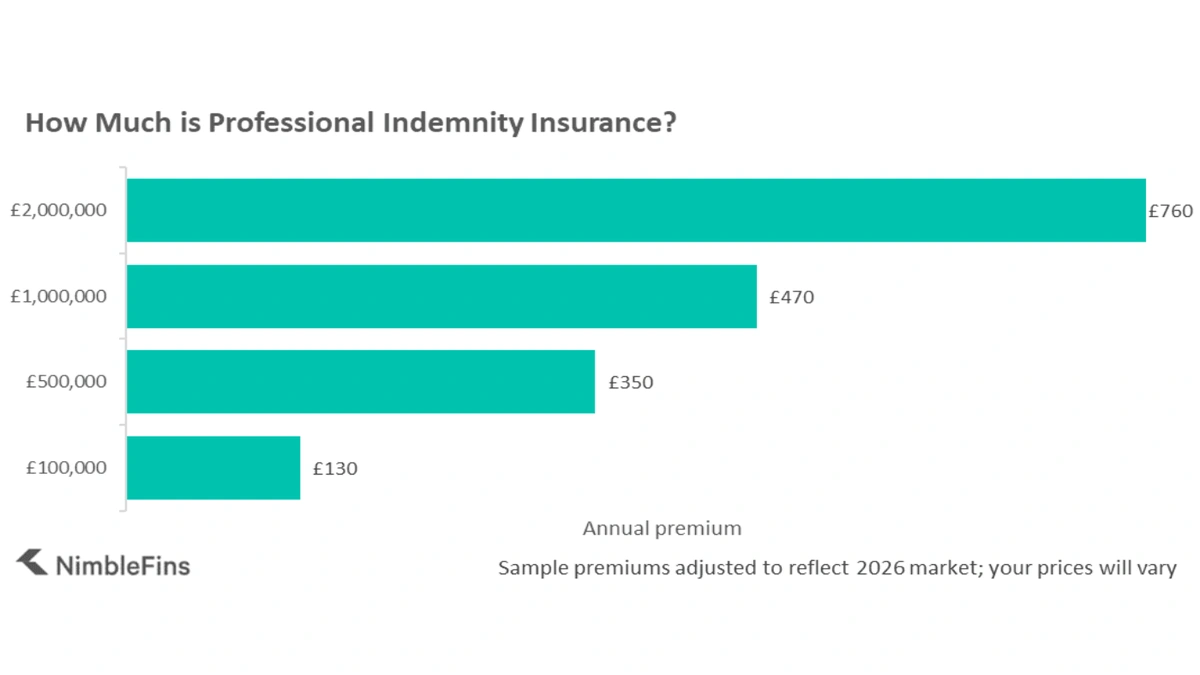

- The Indemnity Limit: This is the maximum amount your insurer will pay out for any single claim (or sometimes, for all claims in a policy year). Common limits range from £50,000 to £5 million or more. The higher the limit you choose, the higher your premium. It’s crucial to select a limit that adequately covers your potential liabilities. Think about the worst-case scenario for your projects.

- Your Claims History: If you’ve had previous claims against you, insurers will view you as a higher risk, which will inevitably drive up your costs. A clean claims history is a golden ticket to better rates.

- Your Contractual Requirements: Many client contracts, especially with larger organisations, will stipulate a minimum level of PI cover you must hold. This can dictate your indemnity limit, irrespective of what you might prefer.

- Number of Employees: If you operate as a sole trader, your risk profile is different from a larger firm. For a professional indemnity insurance UK limited company with multiple employees, the policy needs to cover the actions of all staff, which increases complexity and, consequently, cost. This is a key consideration for small business insurance too.

- The Excess/Deductible: This is the amount you agree to pay yourself towards any claim before your insurer steps in. A higher excess typically means a lower premium, but be sure you can comfortably afford that excess if a claim arises.

So, what does this mean for someone asking, ” how much is professional indemnity insurance for self employed UK ?” For a low-risk self-employed professional like a freelance copywriter with a modest turnover and a £100,000 indemnity limit, you might be looking at premiums from £100-£300 per year. But for a high-risk consultant, or a PI insurance cost UK small business in a field like architecture with a £1 million limit, that could easily jump to £1,000-£5,000+ annually. It’s a vast spectrum!

Smart Strategies to Get the Best Professional Indemnity Insurance Quotes UK

Now that you understand what influences the cost, let’s talk strategy. You don’t just have to accept the first quote you get. There are smart ways to navigate the market and ensure you’re getting value, not just a policy. I’ve seen too many people just renew year after year without questioning if they could do better.

- Shop Around (Seriously!): This isn’t a secret, but it’s often overlooked. Don’t just stick with your current insurer out of habit. Use insurance brokers who have access to multiple providers, or leverage comparison websites. Each insurer has a different appetite for risk and different pricing models. What’s expensive with one might be competitive with another.

- Be Meticulously Accurate with Your Information: When seeking professional indemnity insurance quotes UK, provide precise and comprehensive details about your business, services, turnover, and claims history. Undervaluing or misrepresenting your business might get you a cheaper quote initially, but it could invalidate your policy when you need it most. Honesty is absolutely the best policy here.

- Understand Your True Needs: Don’t just blindly pick an indemnity limit. Assess your worst-case scenario. What’s the maximum financial damage an error from your services could cause? If your largest contract is £50,000, a £1 million limit might be overkill, but a £50,000 limit might be too low if a claim could impact many clients or lead to significant consequential losses. Balance adequate cover with affordability.

- Consider a Higher Excess: If you have robust emergency savings, opting for a higher excess (the amount you pay towards a claim) can significantly reduce your annual premium. Just ensure it’s an amount you could comfortably pay without stress.

- Implement Robust Risk Management: Insurers love to see that you’re proactive about mitigating risks. This could include having clear contracts, robust internal quality control processes, excellent record-keeping, client sign-offs, and continuous professional development. Documenting these practices can sometimes lead to better rates.

- Don’t Always Go for the “Cheapest”: While everyone wants the cheapest professional indemnity insurance UK, remember that the cheapest isn’t always the best value. A slightly higher premium for an insurer with an excellent reputation for claims handling, broader coverage, or better customer service can be worth every penny if you ever need to make a claim. Think long-term protection, not just short-term savings.

For more insights into managing financial risks, you might find our guide on term life insurance premium calculator USA helpful, as it touches on similar principles of assessing future financial needs.

Beyond the Premium | What Else to Consider

It’s easy to get fixated on the number, but the premium is just one part of the puzzle. A cheap policy with significant exclusions or a poor insurer isn’t a bargain; it’s a liability waiting to happen. What truly fascinates me is how often people overlook the fine print.

- Policy Exclusions: This is critical. What isn’t covered? Some policies might exclude certain types of work, specific geographical locations, or claims arising from specific circumstances (like cyber-attacks, which often require separate cyber insurance ). Always read the policy wording carefully.

- Insurer’s Reputation and Financial Stability: In the event of a large claim, you want an insurer who is financially sound and has a proven track record of fair and efficient claims handling. Research reviews and ratings.

- Customer Service: When you have a question or, more importantly, when you need to make a claim, good customer service is invaluable. Can you easily reach them? Are they helpful and responsive?

- Retroactive Cover: If you’re switching insurers, ensure your new policy provides retroactive cover for work you did before the policy started. Otherwise, you could have a gap in your protection for past projects.

The UK insurance market is regulated by the Financial Conduct Authority (FCA), which provides a layer of protection for consumers. You can always check an insurer’s or broker’s registration on the FCA Register to ensure they are legitimate.

Your Burning Questions About Professional Indemnity Insurance Answered

FAQs

Is professional indemnity insurance mandatory in the UK?

It depends on your profession. For certain regulated professions like solicitors, accountants, and financial advisors, it is legally or regulatory mandatory. For many others, while not legally required, it’s often a contractual requirement by clients or simply a crucial best practice to protect your business.

How can I reduce my professional indemnity insurance cost?

You can reduce costs by shopping around for quotes, choosing a higher excess, accurately detailing your services to avoid over-insuring, demonstrating robust risk management practices, and ensuring your indemnity limit truly reflects your exposure, not just a generic figure.

What is the typical professional indemnity insurance cost for a freelancer?

For a low-risk freelancer (e.g., copywriter, graphic designer) with a modest turnover and an indemnity limit of £100,000 to £250,000, the cost can range from £100 to £400 per year. Higher-risk freelance consultants might pay significantly more, often £500+ annually.

Does my turnover affect my PI insurance premium?

Yes, absolutely. Your annual turnover is a significant factor. Insurers typically view higher turnover as indicative of more work, more clients, and therefore, a greater potential for claims, which will generally result in higher premiums.

Can I get professional indemnity insurance for a new business?

Yes, you can. Many insurers offer policies specifically tailored for startups and new businesses. Be prepared to provide details about your planned services, projected turnover, and relevant experience to help them assess the risk.

What is an ‘indemnity limit’ and how do I choose it?

The indemnity limit is the maximum amount your insurer will pay out for a single claim or, in some cases, for all claims within a policy year. You should choose a limit that covers the potential financial loss a client could suffer due to your error or negligence, including legal costs. Consider your largest contract values and any contractual requirements.

So, there you have it. Understanding professional indemnity insurance UK cost isn’t about finding a magic number; it’s about understanding the variables, asking the right questions, and making informed decisions that truly protect your hard-earned business. It’s an investment in your future, your reputation, and your peace of mind. Go forth, negotiate wisely, and build with confidence!