Alright, let’s talk about car insurance. For most of us, it’s always been this fixed, often frustrating, expense, right? You pay a set premium every month, whether you drive 50 miles or 500. But what if there was a smarter way, especially if your car mostly sits pretty in the driveway? That’s where pay per mile car insurance steps onto the scene in the USA , and trust me, it’s more than just a trendy new option. It’s a fundamental shift in how we think about protecting our vehicles, and for many, it could mean significant car insurance savings .

Now, I know what you might be thinking: “Another insurance gimmick?” And honestly, I initially thought it might be just that. But then I dug deeper, and what fascinates me is the ‘why’ behind its growing popularity. It’s not just about saving a few bucks; it’s about aligning your costs with your actual driving habits, a concept that traditional insurance often overlooks. For a savvy consumer, particularly those of us who might have moved to the US and are navigating new commutes or even working remotely, understanding this shift is crucial. It’s about being smart with your money, plain and simple.

Why “Pay Per Mile” is More Than Just a Buzzword | The Economic Shift

Let’s be honest, the world has changed. The 9-to-5 commute, five days a week, is no longer the default for everyone. Remote work is more common, ride-sharing services are prevalent, and many urban dwellers rely on public transport or bikes. Yet, traditional auto insurance, with its fixed monthly or annual premiums, often acts as if we’re all still logging thousands of miles every month. This system, frankly, penalizes low-mileage drivers – people who use their cars infrequently, maybe just for weekend errands or occasional trips.

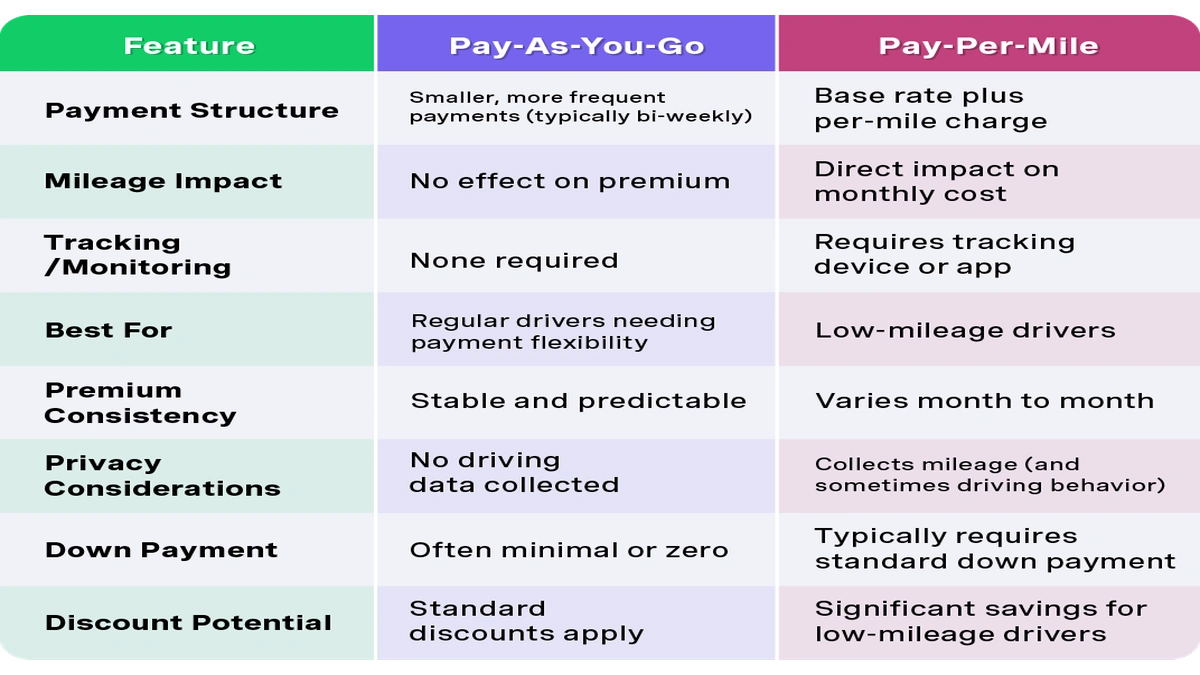

This is precisely the gap that usage-based insurance (UBI) , often synonymous with pay per mile car insurance, aims to fill. Instead of guessing your risk based on demographics and historical data, UBI models base your insurance premiums on how much you actually drive. Think of it as a utility bill for your car: you only pay for what you consume. This model has gained serious traction, especially post-pandemic, as people re-evaluated their driving needs. It’s a fairer, more transparent approach that reflects real-world usage, making it a game-changer for many.

How Telematics is Reshaping Your Insurance Premiums (and Privacy)

So, how exactly do these companies know how much you drive? The magic word here is “telematics.” This involves a small device, often plugged into your car’s OBD-II port, or a smartphone app, that tracks your mileage. Some advanced systems even monitor your driving habits like speed, braking, and time of day you drive. This is the backbone of telematics insurance, allowing providers to offer highly personalized rates.

Companies like Metromile, Root, and Allstate Milewise are prominent players in the per-mile car insurance companies landscape. They use this data to calculate your base rate plus a per-mile charge. For instance, you might pay a fixed daily rate of $2.00 plus 6 cents for every mile you drive. It’s a straightforward premium calculation that can lead to substantial savings on car insurance for those who drive less. However, it’s not without its considerations. The elephant in the room, of course, is data privacy concerns. Giving an insurance company access to your driving data raises questions for some, and it’s a valid point to ponder. You’re trading some personal data for potential savings, and that’s a choice every individual has to make. For a deeper dive into how this technology works, you might find thisInvestopedia article on Usage-Based Insurancequite enlightening.

Who Truly Benefits? A Deep Dive for Indian-origin Drivers in the USA

Let’s narrow this down a bit, especially for our community. If you’re an Indian-origin individual living in the USA, your driving patterns might be quite unique. Are you a student relying on university transport or ride-shares, only using a car for occasional grocery runs? Are you a recent immigrant still getting settled, with a short commute or perhaps working from home? Or maybe you have a second car that’s used infrequently? If any of these sound familiar, then pay per mile car insurance could be a fantastic fit for you.

Consider the typical scenarios: a student in a city like New York or Chicago, where public transport is robust; a tech professional in Silicon Valley who bikes to work most days; or a family with two cars, where one is primarily for weekend leisure. For these low-mileage drivers, the traditional insurance model is almost certainly overcharging them. By switching to a per-mile car insurance plan, they could see their insurance premiums drop significantly. It’s about matching the cost to the actual risk and usage. However, if you’re a cross-country trucker, an Uber driver, or someone with a long daily commute, this might not be your golden ticket. It truly depends on your individual driving habits and needs. It’s always wise to be exploring your insurance options thoroughly.

Navigating the Comparison | What to Look For Beyond the Rate

Okay, so you’re intrigued. You’re thinking about making the switch or at least getting a quote. But how do you compare pay per mile car insurance USA options effectively? It’s not just about the lowest per-mile rate. There are several other factors you absolutely must consider.

First, look at the fixed daily or monthly fee. Some companies have a higher base fee but a lower per-mile rate, while others might flip that. Then, dive into the coverage itself. Are the deductibles reasonable? What about liability limits, comprehensive, and collision coverage? Do they offer roadside assistance, and what are the terms? Don’t forget to check customer service reviews – an app-based insurance model needs solid support when things go wrong. Transparency in their premium calculation is also key; you want to understand exactly how your rates are determined.

Moreover, consider the technology. Is the tracking device easy to install? Is the app user-friendly and reliable? Some companies might cap your daily mileage for billing purposes (e.g., you won’t be charged for more than 250 miles in a single day, even if you drive further), which is a fantastic perk for occasional long trips. Just like when you’re understanding insurance payouts for life insurance, it’s crucial to read the fine print for your car insurance too, ensuring you’re fully protected.

Your Burning Questions About Pay Per Mile Insurance Answered

How do pay per mile car insurance companies track my mileage?

Most commonly, they use a small telematics device that plugs into your car’s OBD-II port (On-Board Diagnostics) or a smartphone app with GPS tracking. This technology monitors your driving distance.

Is usage-based insurance cheaper for everyone?

No, it’s generally cheaper for low-mileage drivers. If you drive significantly more than the average person (e.g., over 10,000-12,000 miles per year), a traditional policy might still be more cost-effective. It truly depends on your driving habits.

What about my privacy with telematics insurance?

This is a common concern. While telematics insurance companies collect data on your mileage and sometimes driving behavior, they are typically bound by privacy policies. It’s crucial to read their terms to understand what data is collected, how it’s used, and if it’s shared with third parties. Many focus solely on mileage, not detailed driving style.

Can I switch back to traditional insurance easily?

Yes, you can. Insurance policies are typically renewable every six or twelve months, and you can usually switch providers or policy types at renewal. If you find pay per mile car insurance isn’t working for you, you can always explore other options.

Which are the top per-mile car insurance companies in the USA?

Some of the leading per-mile car insurance companies include Metromile, Root, Allstate Milewise, and Nationwide SmartMiles. Availability can vary by state, so it’s always best to get quotes from multiple providers in your area.

So, there you have it. Pay per mile car insurance isn’t just a niche product; it’s a significant evolution in the car insurance USA landscape, driven by changing lifestyles and a demand for fairer pricing. For the right driver – especially those of us who find our cars sitting idle more often than not – it offers a compelling pathway to substantial savings on car insurance and a more equitable way to pay for protection. It’s about being an informed consumer in a rapidly evolving market. Don’t just settle for the status quo; explore what truly fits your life.