Let’s be honest, finding car insurance for bad credit drivers USA can feel like trying to solve a Rubik’s Cube blindfolded. It’s frustrating, often expensive, and frankly, a bit disheartening. You’re just trying to get from point A to point B safely, but your past financial hiccups seem to cast a long shadow over your present needs. I’ve seen countless drivers in this exact spot, feeling stuck and wondering if affordable coverage is even a real possibility. Well, here’s the thing: it absolutely is. It just requires a bit more savvy, a few insider tips, and a willingness to navigate the system differently.

This isn’t just about finding any policy; it’s about finding the right policy without breaking the bank. Think of me as your guide, helping you shine a light on the hidden pathways to better rates. We’re going to dive deep into the ‘how’ – how to understand the system, how to actively seek out more favorable terms, and how to ultimately secure reliable auto insurance even when your credit score isn’t singing praises.

The Credit Score Conundrum | Why It Matters for Your Auto Insurance

You might be scratching your head, wondering, “What does my credit score have to do with my driving?” It’s a valid question, and one I hear all the time. The short answer, according to most insurance companies, is risk. Insurers use a complex algorithm that often includes a credit-based insurance score (which is not your FICO score, but a related metric) to predict how likely you are to file a claim. The logic, however flawed it might feel to us, is that individuals with lower credit scores are statistically more likely to file claims, or perhaps even miss payments on their premiums. This translates directly into higher insurance rates for those with bad credit .

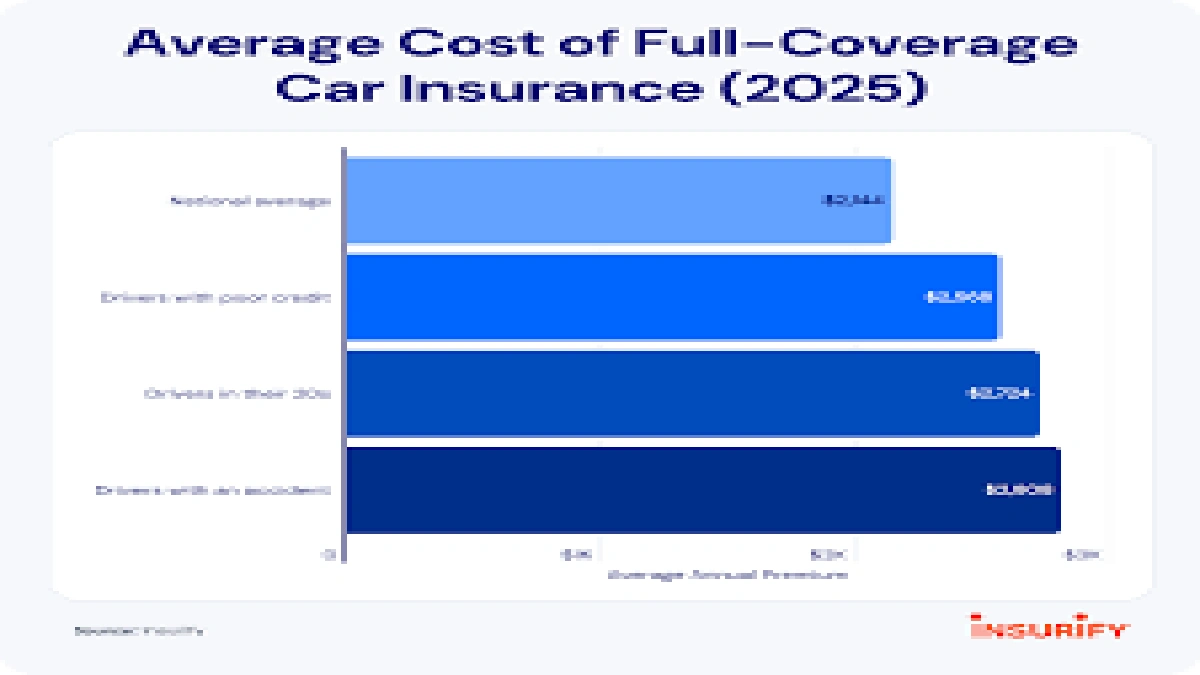

It’s not about being a bad driver; it’s about perceived financial stability. This is why understanding how credit score affects car insurance rates is your first step to empowerment. While not every state allows insurers to use credit scores (California, Hawaii, Massachusetts, and Michigan are notable exceptions), in the vast majority of the USA, your credit history plays a significant role. For instance, a report by the Consumer Federation of America found that drivers with poor credit could pay 70% to 100% more for auto insurance than those with excellent credit, even with identical driving records. It’s a bitter pill to swallow, but acknowledging this reality is crucial for strategizing your next move. So, while it feels unfair, knowing the game helps you play it better. For more insights on credit’s impact on insurance, you can check resources likethe Consumer Federation of America.

Your Action Plan | Finding Affordable Car Insurance for Bad Credit Drivers USA

Okay, so we know the ‘why.’ Now, let’s get to the ‘how’ – the practical steps you can take to mitigate the impact of bad credit and find genuinely affordable car insurance for bad credit drivers USA . This isn’t a magic wand, but a strategic approach that will yield results if you stick with it.

Step 1 | Shop Around Relentlessly (and Smartly)

This is probably the single most important piece of advice I can give you. Do not, under any circumstances, settle for the first quote you receive. Different insurers weigh credit scores differently. Some might be more lenient, or simply have a different risk assessment model for drivers with less-than-perfect credit. You absolutely need to get multiple insurance quotes for drivers with poor credit . Use online comparison tools, call local agents, and don’t be afraid to pit quotes against each other. What looks like a small difference on paper can save you hundreds, if not thousands, over a year.

Step 2 | Understand High-Risk Auto Insurance

If your credit score (and perhaps a shaky driving record) places you in the “high-risk” category, you’re not alone. Many drivers fall into this bracket. The key here is to specifically seek out companies that specialize in high-risk auto insurance . These insurers are set up to deal with drivers who might have a few more blemishes on their record, and while their rates might still be higher than average, they are often more competitive for your specific situation. Don’t waste time with companies that clearly cater to pristine drivers; focus your energy where you’re more likely to find a fit. You might also find better options forinstant approval life insurancethrough similar specialized providers.

Step 3 | The SR-22 Factor (If Applicable)

For some drivers with bad credit , especially those with serious driving infractions like DUIs, an SR-22 form might be required. This isn’t an insurance policy itself, but a certificate of financial responsibility that your insurer files with the state DMV, proving you carry the minimum required liability coverage. If you need SR-22 insurance , be upfront about it when getting quotes. Not all insurers offer it, and those that do will factor it into your premium. It’s a temporary requirement, usually for 3-5 years, but it’s crucial to comply to avoid license suspension. You can find more details on SR-22 requirements on your state’s DMV website, such asthe California DMV.

Step 4 | Maximize Every Discount Imaginable

Discounts are your best friend when you’re trying to lower insurance rates . Seriously, ask about everything . Common discounts include: multi-policy (bundling auto with homeowners or renters insurance), good student (if applicable), defensive driving course completion, anti-theft devices, low mileage, paying in full, and even having certain vehicle safety features. Every little bit helps, and for drivers with bad credit , these savings can be the difference between unaffordable and manageable premiums. Don’t be shy; inquire about every single one.

Step 5 | Consider a Higher Deductible (with caution)

A higher deductible means you pay more out-of-pocket if you make a claim, but it significantly lowers your monthly premium. This can be a viable strategy for saving money on your auto insurance , but it comes with a caveat: only choose a deductible you can comfortably afford to pay at a moment’s notice. An emergency fund specifically for your deductible is a smart move here. You wouldn’t want to save on premiums only to be unable to pay your deductible after an accident.

Step 6 | Explore No-Down-Payment Options (with a realistic outlook)

While truly “no-down-payment” car insurance is rare, especially for drivers with bad credit , some insurers offer low initial payments or monthly installment plans. The term no-down-payment car insurance bad credit often refers to policies where the first month’s premium is the only upfront cost. These can ease the immediate financial burden, but remember that the total annual cost might still be higher than policies requiring a larger initial payment. Always compare the total annual cost, not just the upfront fee.

Strategies Beyond the Policy | Improving Your Credit and Saving More

While the immediate goal is to find affordable car insurance for bad credit drivers USA , let’s also talk about the long game. Because here’s the truth: the best way to get the cheapest car insurance for bad credit in the long run is to tackle the root cause – your credit score. This isn’t a quick fix, but a sustained effort that will benefit you far beyond just your insurance premiums. It’s like building a strong foundation; it takes time, but the benefits are immense.

One of the most impactful ways to start improving credit score for insurance and generally is to simply pay your bills on time, every time. Payment history is the biggest factor in your credit score. Next, try to keep your credit utilization low – this means not maxing out your credit cards. If you have old, unpaid debts, look into strategies like debt consolidation or settlement, but proceed with caution and professional advice. Regularly check your credit report for errors (you can get a free one annually from each of the three major bureaus). Disputing inaccuracies can sometimes give your score a quick, albeit minor, boost. Remember, even small improvements in your credit score can eventually translate into lower insurance rates .

This long-term strategy isn’t just about reducing your auto insurance costs; it’s about financial health overall. A stronger credit profile opens doors to better interest rates on loans, mortgages, and even helps with things like renting an apartment or getting certain jobs. Think of it as an investment in your future self. For businesses, understanding financial requirements is key, much like navigatingsmall business insurance requirements.

Don’t Let Bad Credit Define Your Driving Future

Navigating the world of car insurance for bad credit drivers USA can feel like an uphill battle, but it doesn’t have to be a losing one. The key is to be proactive, informed, and persistent. Don’t let the initial frustration or a few high quotes deter you. There are options out there, even for those needing high-risk auto insurance or facing the complexities of SR-22 . By diligently shopping around, understanding the factors at play, leveraging every possible discount, and committing to improving your financial standing over time, you can absolutely find reliable and more affordable coverage.

Remember, your past financial situation doesn’t have to dictate your ability to drive safely and legally. With a strategic approach and a bit of determination, you can take control of your auto insurance destiny. You’ve got this!

Frequently Asked Questions About Car Insurance for Bad Credit Drivers

Does my credit score really impact my car insurance rates in the USA?

Yes, in most U.S. states, your credit-based insurance score (a variation of your credit score) is a significant factor insurers use to assess risk and determine your premium. States like California, Hawaii, Massachusetts, and Michigan are exceptions.

Can I get car insurance with no down payment if I have bad credit?

While truly “no down payment” policies are rare, especially for drivers with bad credit, many insurers offer low initial payments or monthly installment plans where your first month’s premium serves as the initial payment. Always compare total annual costs.

What is SR-22 insurance and do I need it?

SR-22 is not an insurance policy but a certificate proving you carry the minimum liability coverage required by your state, often mandated after serious driving offenses like a DUI. If required, your insurer files it for you, and it typically leads to higher premiums.

How long does bad credit affect my car insurance?

The impact of bad credit on your car insurance can last as long as the negative items remain on your credit report, typically 7-10 years. However, as your credit score gradually improves, you can start seeing reductions in your premiums much sooner.

Are there specific companies that specialize in high-risk auto insurance?

Yes, many insurance companies specialize in or have divisions dedicated to high-risk auto insurance . These often include non-standard carriers or larger insurers with specific programs designed for drivers with past incidents or bad credit . It’s crucial to shop around and specifically ask if they cater to high-risk drivers.

What’s the fastest way to get cheapest car insurance for bad credit?

The fastest way to find the cheapest car insurance for bad credit is to aggressively shop around and compare quotes from at least 5-7 different insurers, focusing on those known to be more lenient with credit. Also, maximize all eligible discounts and consider a higher deductible you can afford.