Let’s be honest, when you’re launching or running an LLC in the USA, the phrase “insurance cost” probably doesn’t spark joy. It often feels like another unavoidable expense, a line item to minimize. But here’s the thing: understanding your general liability insurance for LLC USA cost isn’t just about finding the cheapest premium. It’s about making a strategic investment in your business’s future, a decision that can literally save your venture from unforeseen disasters. What fascinates me, having navigated these waters with countless small business owners, isn’t just what you pay, but why the numbers can swing so wildly. And more importantly, why skimping here is almost always a costly mistake.

Think of it this way: your LLC is your brainchild, your livelihood. And just like you’d protect your home or your health, your business needs a robust shield. General liability insurance, often called commercial general liability (CGL) , is that foundational shield. It protects your business from claims of bodily injury, property damage, and personal and advertising injury that might arise from your business operations. Without it, a slip-and-fall incident on your premises, a faulty product causing damage, or even an accidental libel claim could lead to devastating financial consequences. So, let’s peel back the layers and truly understand what drives these costs and how to ensure you’re getting genuine value, not just a low price tag.

Beyond the Sticker Price: What Really Drives Your General Liability Insurance for LLC USA Cost?

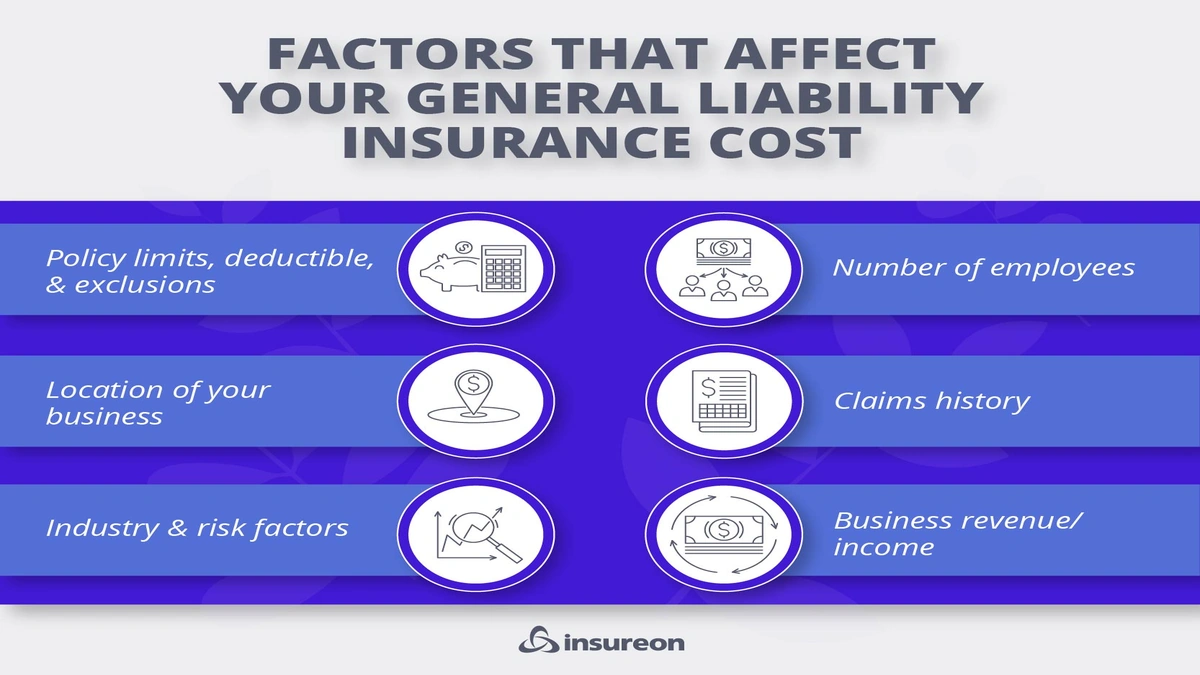

When you get an insurance quote, it’s not just a random number. Insurers are master risk calculators, and they’re looking at a multitude of factors to determine your potential exposure. This is where the ‘why’ really comes into play. The most significant drivers of your small business insurance costs include:

- Your Industry: This is probably the biggest factor. A consulting firm working remotely faces vastly different risks than a construction company or a restaurant. Businesses with higher foot traffic, physical products, or operations involving heavy machinery will naturally have higher premiums because their statistical likelihood of a claim is greater.

- Your Location: Where your LLC operates matters. Businesses in densely populated urban areas, or regions with a higher propensity for lawsuits, might see increased insurance premiums. State-specific regulations and legal environments also play a role.

- Your Business Size and Revenue: Generally, larger businesses with more employees, higher revenues, and a broader scope of operations present more potential points of failure, thus leading to higher costs.

- Your Claims History: Past claims are a red flag for insurers. A history of previous liability claims will almost certainly push your rates up. This is why proactive risk management is so crucial.

I’ve seen businesses in seemingly low-risk sectors get hit with surprisingly high quotes because of a single, ignored safety protocol. It’s not just about the industry; it’s about how you operate within it. This is where a deep dive into your specific business model becomes indispensable.

The Unseen Variables: Risk Assessment and Policy Limits

It might sound a bit like detective work, but insurers are essentially conducting a detailed risk assessment of your LLC. They’re looking at everything from your physical premises – is it well-maintained? Are there clear safety signs? – to your operational procedures. Do you have robust employee training? Are your products manufactured to high standards? Every detail contributes to the overall risk profile.

Then there are your policy limits . This is the maximum amount an insurer will pay out for a covered claim. Choosing the right limits is a delicate balance. Too low, and you could be exposed to significant out-of-pocket expenses if a major lawsuit hits. Too high, and you might be paying for coverage you don’t realistically need, driving up your insurance premiums unnecessarily. Most small businesses opt for limits like $1 million per occurrence and $2 million aggregate, but your specific needs might vary. And don’t forget the deductibles – the amount you pay before your insurance kicks in. A higher deductible typically means lower premiums, but it also means more initial outlay if a claim occurs.

Having advised numerous LLCs, I’ve seen a common mistake: focusing solely on the premium without truly understanding what those limits mean in a real-world scenario. It’s not just a theoretical number on a policy; it’s the lifeline that could keep your business afloat. Just as homeowners consider specific environmental risks like hurricanes and floods when assessinghome insurance coverage, businesses must consider their unique operational and environmental exposures when crafting their broader protection strategy.

Navigating the Market: Getting the Best Business Liability Coverage Without Overpaying

So, how do you ensure you’re getting comprehensive business liability coverage without feeling like you’re throwing money into a black hole? It boils down to smart shopping and proactive management:

- Shop Around, Seriously: Don’t just get one quote. Different insurers have different appetites for risk and may specialize in certain industries. What one company considers high-risk, another might view as manageable. Compare at least three to five insurance quotes from reputable providers.

- Bundle Your Policies: Often, insurers offer discounts if you purchase multiple policies from them. This could include general liability, professional liability (E&O), workers’ compensation, or commercial property insurance. It’s not just about cost savings; it streamlines your insurance management too. For a deeper dive into liability considerations, especially for smaller entities, exploring resources on public liability insurance for small business can provide valuable context, even if the specific regulations differ from the USA.

- Implement Robust Risk Management: This is your secret weapon. Proactive measures like regular safety inspections, employee training, clear signage, secure premises, and strong contracts can significantly reduce your risk profile. The fewer claims you have, the lower your long-term premiums will be.

- Review Your Policy Annually: Your business isn’t static, and neither should your insurance. Changes in your operations, revenue, or even location should trigger a policy review. You might be over-insured or, worse, under-insured for your current needs.

- Work with an Independent Agent: An independent insurance agent can be an invaluable asset. They work with multiple carriers, understand the nuances of various policies, and can help you tailor coverage that truly fits your LLC without bias towards a single provider.

Remember, the goal isn’t just to find cheap insurance. It’s to find adequate insurance that offers robust LLC protection at a fair price. As the U.S. Small Business Administration often emphasizes, understanding and mitigating risks is fundamental to sustainable business growth. For more insights into managing business risks, official resources likeSBA.govcan be extremely helpful.

More Than Just an Expense: The Strategic Value of LLC Protection

Ultimately, viewing your general liability insurance for LLC USA cost as an investment rather than just an expense shifts your perspective entirely. It’s not just about covering unexpected accidents; it’s about safeguarding your reputation, preserving your assets, and ensuring the continuity of your business.

Consider the alternative: a lawsuit could lead to crippling legal fees, settlement costs, and even damage to your brand that takes years to repair. For many small LLCs, a single significant uninsured claim could mean the end of the business. The peace of mind that comes with knowing you’re protected allows you to focus on what you do best: innovating, growing, and serving your customers.

So, the next time you look at that premium, don’t just see a number. See the security, the stability, and the strategic advantage it provides. It’s the silent partner always working to protect your dreams.

Frequently Asked Questions About LLC Insurance Costs

How much does general liability insurance typically cost for an LLC in the USA?

The average general liability insurance for LLC USA cost can range from $300 to $1,000 annually for small businesses, but this is a broad estimate. Your actual cost will depend heavily on your industry, location, business size, and specific risks. High-risk industries will pay significantly more.

What factors can lower my insurance premiums?

You can potentially lower your insurance premiums by implementing strong safety protocols, maintaining a clean claims history, choosing higher deductibles, bundling multiple policies with one insurer, and accurately representing your business’s risk profile to underwriters.

Is commercial general liability (CGL) mandatory for all LLCs?

While commercial general liability (CGL) is not federally mandated for all LLCs, many states or specific industries may require it. Landlords often require it for commercial leases, and clients might demand proof of insurance before doing business with you. It’s highly recommended for almost all businesses due to the inherent risks of operation.

Can I bundle business liability coverage with other policies?

Yes, absolutely! Many insurers offer Business Owner’s Policies (BOPs) that combine general liability insurance with commercial property insurance and sometimes business interruption insurance. This can often lead to cost savings and simplify your overall insurance management.

What’s the difference between general liability and professional liability?

General liability insurance covers claims of bodily injury, property damage, and personal/advertising injury arising from your business operations. Professional liability (or Errors & Omissions) covers claims related to professional negligence, mistakes, or inadequate work from services you provide. They cover different types of risks, and many service-based LLCs need both.