Let’s be honest, the thought of navigating health insurance in the USA as a freelancer can feel like trying to solve a Rubik’s Cube blindfolded. It’s confusing, often expensive, and frankly, a bit terrifying when you realize your health (and your wallet) are on the line. Gone are the days of a steady employer-sponsored plan, replaced by a landscape of acronyms, deductibles, and premiums that can make your head spin. But here’s the thing: it doesn’t have to be an insurmountable challenge. As someone who’s seen countless independent professionals grapple with this, I can tell you there are smart, actionable ways to find the right coverage without breaking the bank. My goal? To guide you through this maze, step-by-step, so you can focus on what you do best: your freelance work.

The Freelance Healthcare Tightrope | Why It Feels So Complex

The rise of the gig economy health coverage needs has fundamentally reshaped how we think about benefits. When you’re an independent contractor, a consultant, or running your own creative studio, you’re not just your own boss; you’re also your own HR department, benefits administrator, and financial planner. This means the onus of securing health coverage falls squarely on your shoulders. Unlike traditional employees who often have a portion of their premiums covered by their employer, freelancers bear the full brunt of the health insurance for freelancers USA cost . This unique position demands a different approach to understanding, budgeting for, and ultimately acquiring health insurance.

What fascinates me is how many incredibly talented freelancers, adept at their craft, feel completely out of their depth when it comes to this. It’s not a lack of intelligence; it’s a lack of clear, straightforward guidance. Many initially assume they’ll just ‘figure it out’ if something happens, but that’s a gamble with potentially devastating consequences. The hidden context here is that the US healthcare system wasn’t originally designed with the modern freelancer in mind, making proactive planning absolutely crucial for your financial and physical well-being.

Navigating the Major Avenues | Where to Look for Coverage

So, where do you even begin? Think of these as your primary routes to finding suitable health insurance.

The ACA Marketplace (Affordable Care Act Plans for Self-Employed)

This is often the first, and best, stop for many freelancers. The Affordable Care Act (ACA), often referred to as Obamacare, created state and federal marketplaces where individuals can purchase health insurance. The beauty of the ACA for freelancers, especially those with fluctuating incomes, lies in the potential for financial assistance. According to the officialhealthcare.govwebsite, you might qualify for health insurance subsidies USA , known as Premium Tax Credits and Cost-Sharing Reductions. These subsidies can significantly reduce your monthly premiums and out-of-pocket costs, making affordable health plans for self-employed a reality.

Here’s the trick: your eligibility for these subsidies depends on your estimated household income for the year. It’s vital to estimate this accurately (and update it if it changes!) because it directly impacts how much financial help you receive. Many independent contractors find that the ACA marketplace offers comprehensive plans that cover essential health benefits, regardless of pre-existing conditions – a huge plus compared to pre-ACA options.

Professional Organizations & Associations

Don’t underestimate the power of community! Various professional organizations and associations cater specifically to freelancers and independent workers. Groups like the Freelancers Union, for instance, sometimes offer group health insurance plans or access to vetted insurance brokers who understand the unique needs of their members. While not always as robust as the ACA marketplace, these can be valuable resources, especially for specific industries or demographics (e.g., AARP for older freelancers). A common mistake I see people make is overlooking these specific niche options, assuming they’re only for large corporations.

Direct from Insurers (Outside the Marketplace)

You can also purchase health insurance directly from private insurance companies. While this gives you direct access to a wider range of plans, it’s important to note that you won’t be eligible for ACA subsidies if you buy outside the marketplace. This option might be suitable if your income is too high to qualify for subsidies, or if you prefer a specific plan not offered on the marketplace. Always compare these plans carefully with those on the ACA marketplace to ensure you’re getting the best value and coverage for your unique situation.

Short-Term Health Insurance Options

For some, short-term health insurance options might seem appealing due to their lower monthly premiums. However, let me rephrase that for clarity: these are generally not a substitute for comprehensive health insurance. They typically offer limited benefits, don’t cover pre-existing conditions, and aren’t compliant with ACA standards. They can be useful in very specific, temporary situations – say, a gap between jobs or while waiting for an ACA plan to kick in – but they are not a long-term solution for robust health coverage options . It’s best to be fully aware of their limitations before considering them.

Cracking the Cost Code | Understanding Deductibles, Premiums, and More

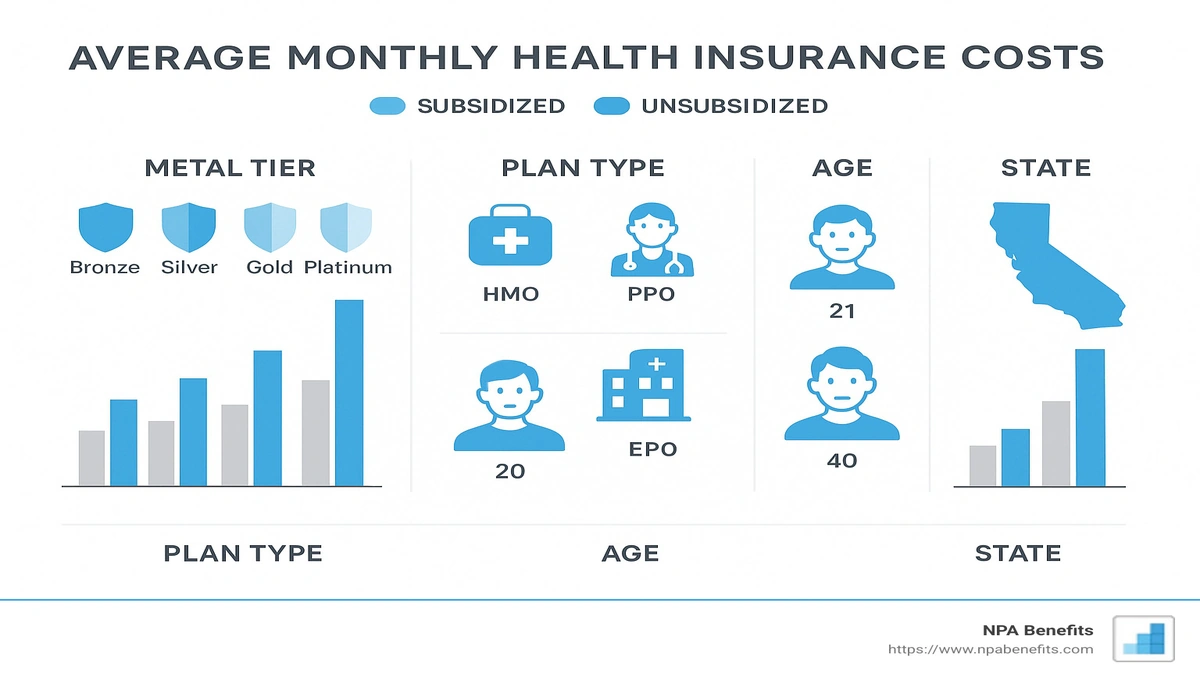

So, you’re looking at plans, and suddenly you’re drowning in jargon. Let’s demystify the key terms that directly impact your health insurance for freelancers USA cost .

- Premiums: This is the most straightforward part – the monthly fee you pay to keep your insurance active. Think of it like your subscription cost.

- Deductibles: This is the amount you have to pay out-of-pocket for covered medical services before your insurance company starts paying. For example, if your deductible is $5,000, you’ll pay the first $5,000 in medical bills for the year before your insurer contributes. Plans with lower monthly premiums often have higher deductibles.

- Copayments (Copays): A fixed amount you pay for a covered service after you’ve met your deductible. For instance, a $30 copay for a doctor’s visit.

- Coinsurance: This is a percentage of the cost of a covered service that you pay after you’ve met your deductible. If your coinsurance is 20%, and a procedure costs $1,000 after your deductible, you’d pay $200.

- Out-of-Pocket Maximum: This is your financial safety net. It’s the maximum amount you’ll have to pay for covered services in a plan year. Once you hit this limit, your insurance company pays 100% of the cost of covered benefits for the rest of the year. This is a crucial number for understanding your absolute worst-case scenario financially.

It’s a balancing act, really. You might opt for a plan with a lower premium but a higher deductible if you’re generally healthy and want to keep monthly costs down. Conversely, if you anticipate frequent medical needs, a higher premium plan with a lower deductible and copays might save you money in the long run. Understanding deductible and premium interplay is key to making an informed decision about your self-employed health insurance .

Smart Strategies to Lower Your Freelance Health Insurance Bill

Now that you know the landscape and the lingo, let’s talk about tangible ways to reduce your overall healthcare expenses as an independent contractor .

- Leverage Subsidies: I cannot stress this enough. If your income qualifies, those ACA Premium Tax Credits and Cost-Sharing Reductions are your best friends. Make sure your income estimate is accurate on the marketplace.

- Consider a High Deductible Health Plan (HDHP) with an HSA: If you’re relatively healthy, an HDHP typically has lower premiums. Paired with a Health Savings Account (HSA), you can contribute pre-tax dollars to cover your deductible and other qualified medical expenses. The money grows tax-free and can be withdrawn tax-free for medical costs. It’s a fantastic triple-tax-advantage savings tool!

- Shop Around Annually During Open Enrollment: Don’t just auto-renew! Plans and prices change every year. Dedicate time during the open enrollment period to compare plans, even if you’re happy with your current one. New affordable health plans for self-employed might emerge.

- Explore Group Options: Beyond professional organizations, look into options like health-sharing ministries (with caution, as they are not insurance) or even small business group plans if you have employees.

- Embrace Telehealth: Many plans now offer robust telehealth options, allowing you to consult with doctors remotely for a fraction of the cost (or even free) compared to an in-person visit. This can significantly reduce your out-of-pocket expenses for routine care.

Managing your overall financial security as a freelancer involves more than just health insurance. It’s about building a comprehensive safety net. Just as you’d consider specific coverage for your property, such ascondo owners insurance USA, or understand liability like withthird party car insurance cost UK, knowing all your insurance needs is crucial. While these might seem disparate, they all contribute to your peace of mind and financial stability in the independent world.

FAQs | Your Burning Questions Answered

Can I get health insurance if I only freelance part-time?

Absolutely! The ACA Marketplace doesn’t care if you’re freelancing full-time or part-time. Your eligibility for plans and subsidies is based on your income, not your work status. So, yes, even if your freelance work supplements another income, you can find coverage.

What if I have a pre-existing condition?

Under the Affordable Care Act, insurance companies cannot deny you coverage or charge you more because of a pre-existing condition. This is one of the biggest benefits of enrolling in an ACA-compliant plan, making it a critical consideration for many freelancers.

Are short-term health insurance options a good idea for freelancers?

Generally, no, not as a long-term solution. While they offer lower premiums, they often come with significant limitations, such as not covering pre-existing conditions, not being ACA-compliant, and having caps on benefits. They’re best considered only for very temporary gaps in coverage, not as your primary gig economy health coverage .

How do health insurance subsidies USA work for fluctuating freelance income?

This is a common concern! When you apply on the ACA Marketplace, you’ll estimate your annual income. If your income changes significantly during the year, you must update your information on the marketplace. This helps ensure you receive the correct amount of subsidy. If you underestimate, you might owe money back at tax time; if you overestimate, you might miss out on financial help you’re entitled to.

What’s the difference between a deductible and a premium?

The premium is the fixed amount you pay monthly to keep your insurance active, regardless of whether you use medical services. The deductible is the amount you must pay out-of-pocket for covered medical services before your insurance starts paying a larger share (usually after which copays/coinsurance kick in). So, premium is your entry fee; deductible is your initial self-pay threshold for services.

Ultimately, navigating health insurance for freelancers USA cost isn’t about finding a magic bullet, but about understanding your options, being proactive, and making informed choices. It’s an essential investment in yourself and your business. By taking the time to research, compare, and strategize, you can secure the peace of mind that comes with knowing you’re covered, allowing you to pour all your energy into your passion. Don’t let the complexity deter you; empower yourself with knowledge and take control of your healthcare journey.