Let’s be honest, the idea of getting full coverage car insurance under $100 USA sounds a bit like finding a unicorn, doesn’t it? In a world where everything seems to cost more, especially auto insurance, many people just assume that truly comprehensive protection at such a low price is simply out of reach. I mean, who wouldn’t want that kind of deal?

But here’s the thing: while it’s not a walk in the park for everyone, achieving affordable auto insurance with robust protection is far from impossible. What fascinates me is how many drivers settle for basic liability, often because they believe health insurance family 4 cost and car insurance are just unavoidable money pits. They miss out on the peace of mind that comes with knowing their vehicle is covered, even in a fender bender that’s their fault, or against an unexpected act of nature. My goal today is to pull back the curtain and show you how smart drivers navigate the insurance landscape to secure that coveted cheap full coverage car insurance without sacrificing essential protection. It’s about strategy, not just luck.

Cracking the Code | Understanding “Full Coverage” (and Why It Matters)

First things first, let’s clear up a common misconception. “Full coverage” isn’t a single, magical policy you can buy. No, it’s actually a bundle of different types of coverage that, when put together, offer a high level of protection for you, your vehicle, and others on the road. Understanding these components is your first step towards finding how to get full coverage insurance that fits your budget.

- Liability Coverage: This is the backbone of any policy and is legally required in most states. It covers damages and injuries you might cause to other people and their property in an at-fault accident. It’s split into bodily injury liability (for medical expenses) and property damage liability (for car repairs, fences, etc.). Think of it as protecting your assets from lawsuits.

- Collision Coverage: This is where your car gets protected. If you hit another car, a pole, or even a pothole that causes damage to your own vehicle, collision coverage helps pay for the repairs, regardless of who was at fault. This is a big piece of why your insurance premiums might seem high, but it’s also crucial for protecting your investment.

- Comprehensive Coverage: This is the “unexpected stuff” coverage. It pays for damages to your car from things other than collisions: theft, vandalism, fire, hail, falling objects (like tree branches), and even hitting an animal. Living in a high-risk area for deer collisions? This is your friend.

When people talk about full coverage car insurance, they’re generally referring to a policy that includes at least these three types. It’s about protecting yourself from the myriad of financial headaches that can arise from owning and driving a car. And yes, finding this comprehensive package for under $100 is indeed the ultimate quest.

The Hunt for Savings | Strategies to Slash Your Premiums

So, how do you actually get those car insurance rates down? It’s not about cutting corners on protection; it’s about being smart and leveraging every available advantage. I’ve seen countless drivers save hundreds, even thousands, by simply knowing what to look for. Here are my go-to strategies:

Understanding Deductibles | Your Out-of-Pocket Sweet Spot

This is probably the most straightforward way to influence your premium. Your deductibles are the amount you agree to pay out-of-pocket before your insurance kicks in for collision and comprehensive claims. A higher deductible almost always means lower insurance premiums. For instance, if you choose a $1,000 deductible instead of $500, your monthly payment will likely drop. The trick? Make sure you have that deductible amount readily available in an emergency fund. Don’t pick a deductible you can’t afford.

Discounts Galore | Are You Leaving Money on the Table?

Insurance companies offer a staggering array of car insurance discounts, and many people don’t even realize they qualify for most of them. Seriously, ask your agent or check online! Some common ones include:

- Bundling Policies: This is huge. If you get your auto and term life insurance plans (or home, renters, etc.) from the same provider, you almost always get a multi-policy discount.

- Good Driver Discount: Maintain a clean driving record for a certain period (usually 3-5 years) and you’ll be rewarded.

- Multi-Car Discount: Insure more than one vehicle with the same company.

- Student Discounts: Good grades, defensive driving courses for teens, or students away at college can all lead to savings.

- Anti-Theft Devices: Alarms, tracking systems, and immobilizers can lower your comprehensive premium.

- Low Mileage Discount: Don’t drive much? Prove it, and save.

- Paid in Full Discount: Paying your annual premium upfront often saves you a small percentage.

It sounds simple, but truly exploring every discount option is a powerful way to reduce your overall cost for full coverage car insurance.

Vehicle Choice | The Car You Drive Matters

This is a big one that often gets overlooked. The type of car you drive significantly impacts your car insurance rates. Expensive luxury cars, high-performance sports cars, and vehicles with a high theft rate will naturally cost more to insure. Why? They’re more expensive to repair or replace. If you’re serious about getting full coverage car insurance under $100 USA, consider a practical, safe, and less flashy vehicle. Newer cars with advanced safety features can sometimes qualify for discounts, too.

Driving Habits & Telematics | Let Your Good Driving Speak

Many insurers now offer telematics programs (also known as usage-based insurance). These programs use a small device plugged into your car or a smartphone app to monitor your driving habits – things like mileage, speed, braking, and time of day you drive. If you’re a safe driver, these programs can offer substantial discounts. It’s a direct way to prove you’re a lower risk and earn a lower insurance premiums.

Your Credit Score | An Unseen Factor

In many states, your credit-based insurance score plays a role in determining your premiums. Insurers use this score as a predictor of how likely you are to file a claim. A higher credit score often translates to lower rates. This is why maintaining good financial health is crucial, not just for loans but for things like affordable auto insurance too.

Beyond the Big Names | Exploring Your Options

Don’t just stick with the first insurer you see an advertisement for. The market is competitive, and that’s good news for you. To find the best policy options for full coverage car insurance under $100 USA, you need to cast a wide net.

- Online Quote Comparison Tools: These are invaluable. Websites allow you to input your information once and get multiple online quotes from various auto insurance companies. This lets you compare apples to apples quickly and efficiently.

- Local Independent Agents: While online tools are great, an independent agent can be a secret weapon. They work with multiple insurers, not just one, and can often find deals or niche policies that you might miss on your own. They understand the local market and can offer personalized advice.

- Lesser-Known Insurers: Sometimes, smaller or regional insurance companies can offer surprisingly competitive rates. They might not have the massive advertising budgets, but their rates could be just what you’re looking for. Don’t be afraid to look beyond the top five names.

- Re-evaluate Annually: Your life changes, and so do car insurance rates. Get new quotes every year, especially if you’ve had a life event like getting married, moving, buying a new car, or if a ticket has dropped off your record. Loyalty is great, but don’t let it cost you money.

Real Talk | What to Expect and Potential Trade-offs

Can everyone truly get full coverage car insurance under $100 USA? Let’s be honest: no, not everyone. Several factors can make this goal more challenging:

- Age: Young drivers (especially those under 25) and very senior drivers often face higher rates due to perceived risk.

- Driving Record: Accidents, speeding tickets, or DUIs will significantly drive up your premiums for years.

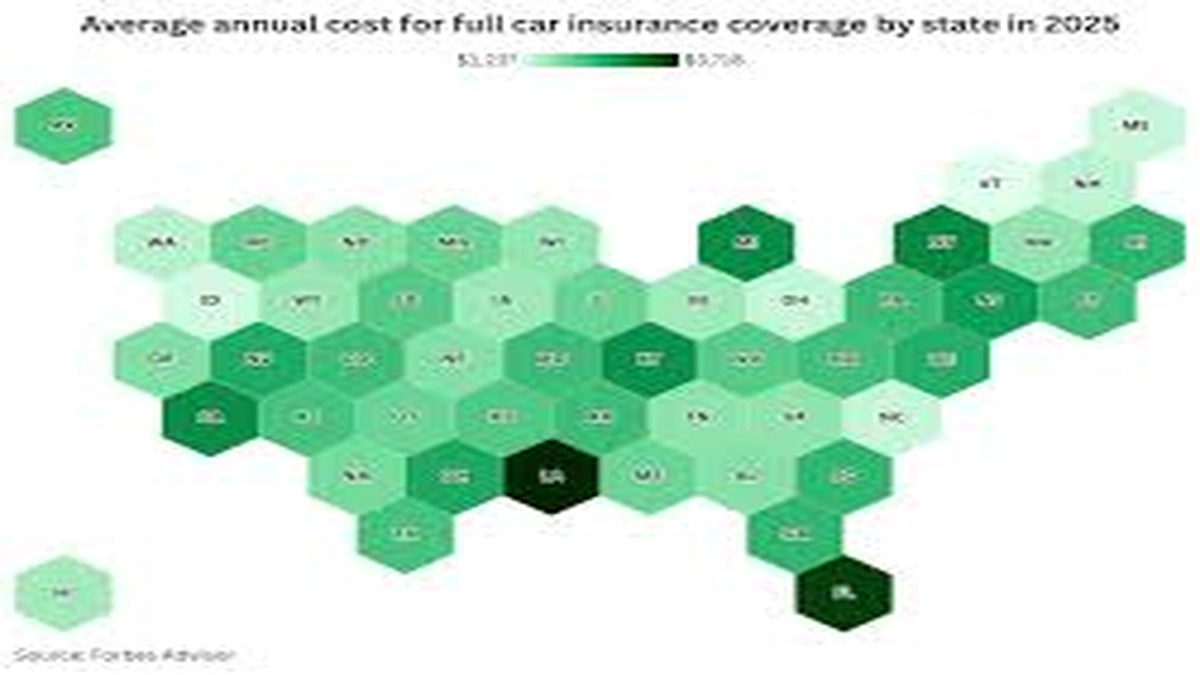

- Location: Living in urban areas with high theft rates, dense traffic, or frequent natural disasters will increase your costs. Your zip code is a huge factor in your insurance premiums.

- Vehicle Value: Insuring a brand-new, expensive car for under $100 might be a stretch, even with all the discounts.

The key is to balance cost with adequate protection. Sometimes, achieving that sub-$100 mark might mean accepting slightly higher basic car insurance terms and deductibles or choosing a vehicle that’s less expensive to repair. It’s about being realistic and strategic. Always ensure your chosen liability limits meet your state’s minimums and ideally exceed them for better protection. You can learn more about state regulations from resources like the National Association of Insurance Commissioners .

Ultimately, the pursuit of cheap full coverage car insurance is a journey of informed decisions and proactive searching. It’s about being an educated consumer and understanding that you have more power than you think to influence your rates. Don’t just accept the first quote; instead, equip yourself with these strategies and go hunting for that unicorn policy. It might just be waiting for you.

Frequently Asked Questions About Affordable Full Coverage Car Insurance

Is it really possible to get full coverage car insurance for less than $100 a month?

Yes, it is absolutely possible for many drivers, though it depends heavily on individual factors like your driving record, vehicle type, location, and the discounts you qualify for. It requires diligent research and applying smart strategies.

What’s the difference between minimum coverage and full coverage?

Minimum coverage typically refers to the state-mandated liability insurance, which covers damages you cause to others. Full coverage car insurance adds collision and comprehensive coverage, protecting your own vehicle from various damages.

How can my credit score affect my car insurance rates?

In many states, insurers use a credit-based insurance score as a factor in determining your premiums. A higher score is often associated with lower risk, potentially leading to lower rates for affordable auto insurance.

What are some easy ways to get discounts on my car insurance?

Common discounts include bundling insurance policies (auto + home/renters), good driver discounts, multi-car discounts, anti-theft device discounts, and paying your premium in full. Always ask your provider about all available options!

Should I raise my deductible to lower my monthly premium?

Raising your deductibles can significantly lower your monthly insurance premiums. However, only do this if you have enough savings to comfortably pay that higher deductible out-of-pocket if you need to file a claim.

How often should I shop around for new car insurance quotes?

It’s a good practice to shop for online quotes at least once a year, or whenever you have a major life event like moving, buying a new car, getting married, or if a past traffic violation expires from your record. This ensures you’re always getting the best car insurance rates.