Alright, let’s grab a cuppa and talk shop, shall we? If you’re running a small business in the UK, whether you’re a freelance designer, a mobile hairdresser, a local builder, or even a quaint little cafe owner, there’s one phrase that probably pops into your head (or should!) more often than you’d like: public liability insurance for small business UK . Now, I know what you’re thinking – insurance, yawn. But here’s the thing: this isn’t just another checkbox on your ‘to-do’ list. This is about protecting your dream, your livelihood, and frankly, your peace of mind. And let me tell you, navigating the world of business insurance can feel like trying to solve a Rubik’s Cube blindfolded.

I’ve seen countless small business owners, just like you, get bogged down in the jargon, unsure if they even need it, or worse, making assumptions that leave them dangerously exposed. That’s why I’m here. Consider me your friendly guide, helping you cut through the noise and understand exactly how to secure the right public liability insurance UK for your venture. We’re not just talking about what it is; we’re diving into the ‘how’ – how to assess your needs, how to find the right policy, and how to avoid those pesky pitfalls that can cost you dearly. Because honestly, the last thing you need is a surprise lawsuit derailing all your hard work.

Do I Really Need Public Liability Insurance UK for My Business? Let’s Break It Down.

This is probably the most common question I hear, and it’s a valid one. Unlikeemployers’ liability insurance UK, which is a legal requirement if you have employees, public liability insurance isn’t legally mandated for most businesses. But – and this is a big ‘but’ – just because it’s not compulsory doesn’t mean it’s optional for smart business owners. Think of it this way: if your business activities bring you into contact with members of the public (clients, customers, suppliers, even passers-by) or their property, you’re exposed to risk.

Imagine this scenario: you’re a plumber, working in a client’s home, and accidentally knock over an expensive vase. Or perhaps you run a market stall, and a customer trips over a loose cable, injuring themselves. Maybe you’re a consultant visiting a client’s office, and you spill coffee on their server (a nightmare, right?). In all these cases, if you’re deemed responsible, you could face a claim for damages, medical expenses, or legal costs. These can quickly spiral into tens of thousands of pounds, an amount that could cripple a small business. So, while not legally required, it’s an essential safeguard for almost every small business interacting with the public. It’s about protecting your assets and your future from unforeseen accidents. This is particularly crucial for those who are self-employed public liability insurance UK is often overlooked but just as vital.

Understanding the ‘How’ | What Does Public Liability Insurance Actually Cover?

Okay, so you’re convinced you need it. Great! Now, let’s get into the nitty-gritty of what this type of coverage actually does. At its core, public liability insurance for small business UK protects you against claims made by members of the public for injury, illness, or property damage caused by your business activities. This isn’t just about accidents on your premises; it extends to incidents that occur off-site, at a client’s location, or even in a public space where you’re operating.

Here are some of the common scenarios it covers:

- Accidental Injury: A customer slips on a wet floor in your shop and breaks their arm.

- Property Damage: Your team is working on a construction site and accidentally damages a neighbouring building.

- Legal Costs: If a claim is made against you, this insurance typically covers the legal fees involved in defending yourself, whether you’re found liable or not. This is a huge, often underestimated, benefit.

It’s important to differentiate this from othertypes of business insurance UK, such as professional indemnity insurance (which covers claims of professional negligence or bad advice) or product liability insurance (for faults with products you sell). A good policy will clearly outline its scope, and a reputable insurance broker UK can help you understand these distinctions.

Cracking the Code | Business Liability Insurance Cost UK and What Influences It

Ah, the million-dollar question (or rather, the hundreds-of-pounds question): how much does it actually cost? There’s no single answer, unfortunately, as the business liability insurance cost UK is influenced by a number of factors. It’s not a one-size-fits-all premium, and that’s actually a good thing, as it means you can tailor it to your specific needs.

Key factors that insurers consider include:

- Your Business Type: A freelance graphic designer working from home will generally pay less than a roofer or a restaurant owner, simply because the inherent risks are lower. Certain trades are deemed ‘higher risk’ due to the nature of their work.

- Your Turnover/Size: Larger businesses with higher turnover often have more exposure and may require higher levels of cover, thus impacting the premium.

- Number of Employees: While public liability covers the public, having more employees can increase the likelihood of an incident occurring.

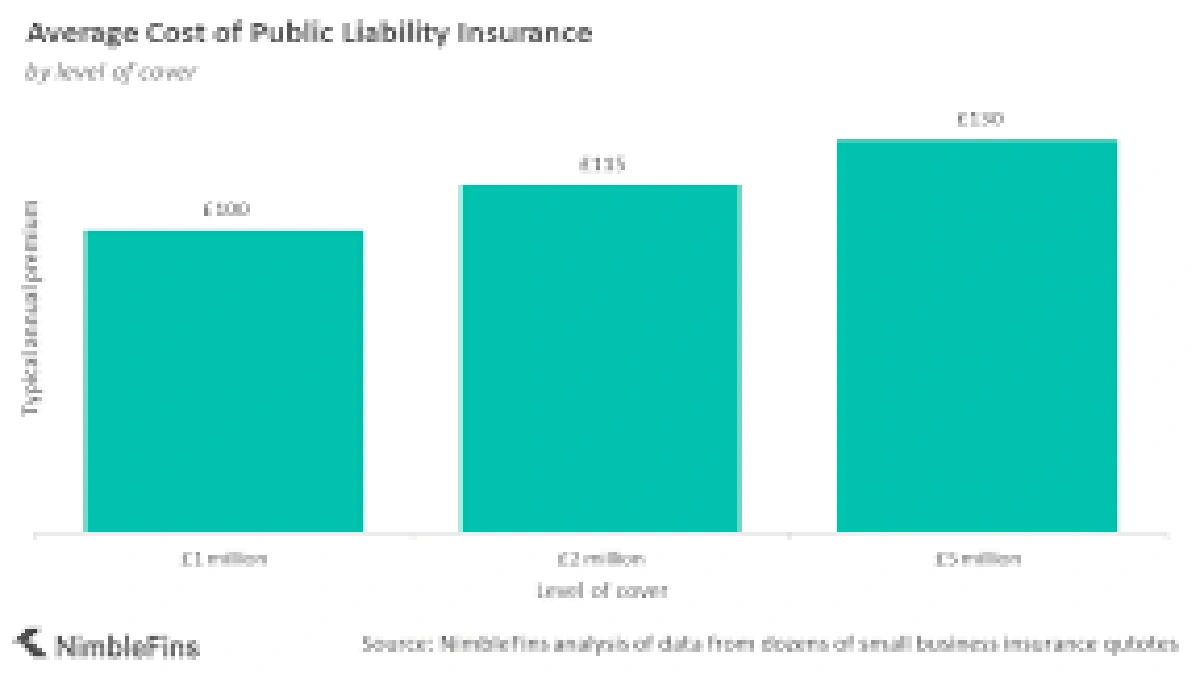

- Level of Cover: Policies typically start at £1 million, but you can opt for £2 million, £5 million, or even £10 million. The higher the cover, the higher the premium, but also the greater your protection. I always recommend considering the maximum potential damage or injury your business could realistically cause.

- Claims History: A clean claims history can lead to lower premiums.

- Excess: This is the amount you agree to pay towards a claim yourself. Opting for a higher excess can sometimes reduce your premium.

My advice? Don’t just go for the cheapest option. It’s tempting, I know. But often, the cheapest policy might have significant exclusions or a lower level of cover than you truly need. Focus on value and adequate protection. For specific information, you can always check resources likethe Association of British Insurers (ABI)for general guidance on business insurance.

Choosing Your Policy | Tips for Finding the Best Public Liability Insurance for Small Business UK

Finding the right policy doesn’t have to be a headache. Here’s a pragmatic, step-by-step approach I recommend:

1. Assess Your Risk Profile

Before you even start looking, sit down and honestly evaluate your business. What are the potential hazards? Do you work at client sites? Do customers visit your premises? Do you handle expensive equipment or materials? Understanding your unique risks will help you determine the appropriate level of cover. For example, a mobile dog groomer has different risks than an online consultant.

2. Decide on Your Level of Cover

As mentioned, options typically range from £1 million to £10 million. Many contracts, especially with larger clients or local councils, might stipulate a minimum level of small business insurance UK you need, often £5 million. Even if not stipulated, think about the worst-case scenario. A serious injury could easily exceed £1 million in compensation and legal fees.

3. Shop Around (But Smartly!)

Don’t just get one quote. Use comparison websites as a starting point, but then consider speaking directly with a few specialist insurers or, better yet, an independent insurance broker UK . Brokers can be invaluable; they have access to a wider range of policies, understand the nuances, and can often negotiate better deals or find cover for niche businesses. They can also bundle differentinsurance optionstogether for you.

4. Read the Fine Print

This is where many people fall short. Before signing on the dotted line, read the policy document carefully. Understand the exclusions (what isn’t covered), the excess, and the claims process. If something isn’t clear, ask! A good insurer or broker will be happy to explain it.

5. Review Annually

Your business isn’t static, so your insurance shouldn’t be either. Review your policy annually, or whenever there’s a significant change in your business (e.g., you hire employees, expand your services, or move premises). This ensures you always have adequate and appropriate cover.

FAQs About Public Liability Insurance for Small Business UK

What is the difference between public liability and professional indemnity insurance?

Public liability insurance covers claims for injury or property damage to third parties caused by your business activities. Professional indemnity insurance, on the other hand, protects you against claims of professional negligence, errors, or omissions in the advice or services you provide.

Is public liability insurance a legal requirement for self-employed individuals in the UK?

No, public liability insurance for small business UK is generally not a legal requirement for self-employed individuals, unless specific contracts or clients demand it. However, it is highly recommended to protect against potential claims from the public or clients for injury or damage.

How much public liability cover do I need?

The amount of cover you need depends on your business type, the risks involved, and any contractual requirements. Most small businesses opt for at least £1 million, but £2 million or £5 million is common, especially for higher-risk trades or those working with larger clients. Always assess your maximum potential exposure.

Can I get public liability insurance as part of a larger business insurance package?

Yes, absolutely! Many insurers offer combined policies that bundle public liability insurance UK with other essential covers like professional indemnity, employers’ liability, and business contents insurance. This can often be more cost-effective and simpler to manage than separate policies.

What happens if I don’t have public liability insurance and someone makes a claim against me?

If you don’t have public liability insurance and are found liable for causing injury or property damage, you would be personally responsible for paying any compensation, legal fees, and associated costs. This could lead to significant financial hardship, potentially forcing your business to close.

Final Thoughts | Don’t Just Buy It, Understand It.

Look, running a small business is tough enough without the constant worry of an unforeseen accident wiping out everything you’ve worked for. Understanding and securing the right public liability insurance for small business UK isn’t just a smart business decision; it’s an act of self-preservation. It’s about building a robust foundation for your venture, one that can withstand the unexpected bumps in the road. So, take the time, do your homework, and get that shield in place. Your future self (and your bank account) will thank you for it.