Let’s be honest, talking about life insurance isn’t exactly a thrilling Friday night topic. It’s often shoved into the ‘adulting’ pile right next to doing taxes and remembering to change your air filter. But here’s the thing: understanding how much life insurance coverage do I need USA isn’t just a chore; it’s a profound act of love and responsibility. It’s about ensuring your loved ones aren’t left scrambling financially if the unthinkable happens. And trust me, navigating this in the American landscape can feel like trying to solve a Rubik’s Cube blindfolded.

I’ve seen countless people make the same mistake: either under-insuring, leaving their family vulnerable, or over-insuring and paying for coverage they don’t truly need. The goal here isn’t to just throw a random number at you. Instead, I want to guide you, step-by-step, through the thought process of determining your actual life insurance needs . Think of me as your personal financial confidant, helping you demystify the numbers so you can make an informed decision for your family’s financial security .

Beyond the Guesstimate | Why a Calculator Isn’t Enough

You’ve probably stumbled upon a life insurance calculator online, punched in a few numbers, and got a figure back. Useful, right? Well, yes, but also, not entirely. These tools are fantastic starting points, but they often miss the nuanced layers of your life. They don’t know about your dreams for your kids’ education, your aging parents, or that slightly-too-expensive coffee habit you can’t kick (just kidding, mostly). The ‘how’ of determining your coverage isn’t just about plugging in data; it’s about understanding the ‘why’ behind each financial obligation.

The core principle, as financial advisors often preach, is to replace your future income and cover your outstanding debts and future expenses . That sounds simple enough, but let’s break it down into digestible chunks, because frankly, it’s rarely as straightforward as it seems. My experience tells me that most people underestimate their true requirements because they don’t account for inflation or unforeseen circumstances. So, let’s dive into the real factors that influence your specific situation.

The D.I.M.E. Method | Your Personal Financial Blueprint

Forget generic advice for a moment. Let’s get personal. A popular, yet incredibly effective, method for calculating your needs is the D.I.M.E. method. It stands for Debt, Income, Mortgage, and Education. This framework helps you quantify the financial obligations you’d want covered, ensuring a comprehensive approach to your financial planning USA .

1. Debt Coverage | Erasing the Burden

First up: your debts. Imagine your family having to deal with the emotional toll of loss and the financial stress of your outstanding obligations. That’s a burden no one should carry. Think about all your consumer debts – credit card balances, car loans, personal loans. Then, there’s the big one: your mortgage. For many American families, the house is their largest asset, but also their largest liability. Ensuring the mortgage is paid off or significantly reduced is often a primary concern. This provides immediate stability and peace of mind. A common mistake I see people make is only considering their current debt, not anticipating potential future liabilities or the cost of living increases. So, add it all up: every penny owed, from the small to the substantial.

2. Income Replacement | Filling the Financial Void

This is arguably the most critical component. Your income fuels your family’s lifestyle, savings, and future plans. If you’re no longer there, who will provide that income? The general rule of thumb used to be 7-10 times your annual salary, but honestly, that’s a bit too simplistic. We need to think about how long your family would need that income replaced. Is it until your youngest child graduates college? Until your spouse retires? Or perhaps for a fixed period to allow them to adjust? I typically advise people to consider a period of 10-20 years, depending on their dependents’ ages and their spouse’s earning potential. This substantial amount of income replacement coverage ensures that daily life, future goals, and even unexpected costs are manageable.

3. Mortgage | Securing Their Home

While we touched on this in ‘Debt,’ the mortgage often warrants its own category due to its sheer size and importance. For many, owning a home is the cornerstone of their American dream. Losing that home due to an inability to make payments after a primary earner passes away is a nightmare scenario. Your life insurance should, at the very least, cover the outstanding balance of your mortgage. This isn’t just about paying a bill; it’s about preserving a sanctuary, a place of stability, and memories for your family. It’s about providing a profound sense of security during an incredibly difficult time.

4. Education | Investing in Their Future

If you have children, their education is likely a huge part of your long-term vision. College costs in the USA are, well, astronomical. Even if you’ve started a 529 plan, additional funds might be needed to cover tuition, room and board, books, and living expenses. Don’t forget, this isn’t just college; it could also include private school, vocational training, or even a postgraduate degree. Factor in potential inflation over the years. This component of your coverage demonstrates a commitment to your children’s future, ensuring their educational path remains unhindered. For more insights on securing your business’s future, you might find this article onsmall business insurance cost guidehelpful too, as it touches on different aspects of financial planning.

Beyond D.I.M.E. | The Nuances of Your Life

While D.I.M.E. is a fantastic foundation, your life is unique. Here are a few other considerations that often get overlooked when people try to calculate life insurance :

- Final Expenses: Funeral costs, medical bills not covered by health insurance, and probate fees can quickly add up to tens of thousands of dollars. These are immediate costs your family will face.

- Childcare Costs: If your spouse would need to return to work or hire more childcare after your passing, factor in these ongoing expenses.

- Special Needs Dependents: If you have a child or another dependent with special needs, their long-term care and financial support will require a significant, often lifelong, fund. This necessitates a more substantial policy.

- Inflation: The cost of living rises. A dollar today won’t buy as much in 10 or 20 years. Always factor in an inflation adjustment when projecting long-term needs.

- Existing Savings & Investments: Do you have substantial savings or existing investments that could offset some of these needs? Don’t forget to subtract these.

This holistic approach helps ensure you’re not just covering the basics, but truly providing a comprehensive safety net. For those exploring different financial products, understandinglow cost term insurance planscan also be a valuable piece of the puzzle.

Term Life vs. Whole Life | Understanding Your Options

Once you have a ballpark figure for your coverage amount, the next big question is: what kind of policy? The two main types are term life insurance and whole life insurance . This is where understanding the types of life insurance really comes into play.

- Term Life Insurance: This is straightforward. You pay premiums for a specific period (e.g., 10, 20, or 30 years), and if you pass away within that term, your beneficiaries receive a death benefit. It’s generally more affordable and ideal for covering specific, time-bound needs like a mortgage or raising children. It’s pure protection, no frills.

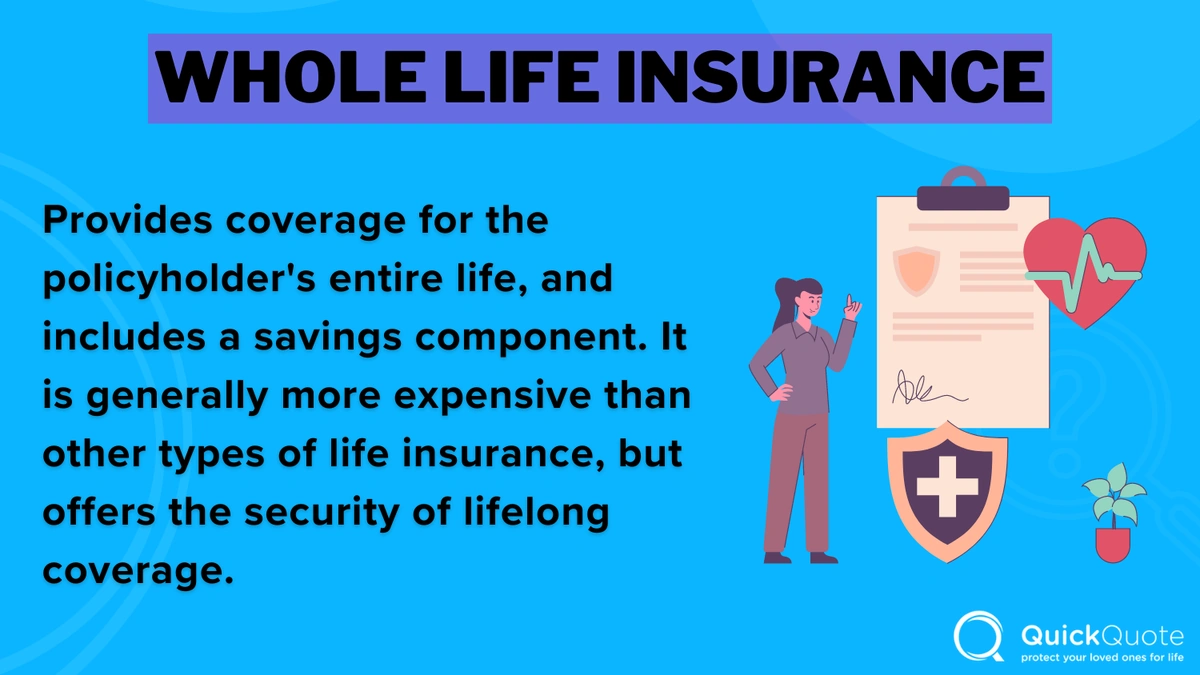

- Whole Life Insurance: This is a permanent policy that covers you for your entire life, as long as premiums are paid. It also builds cash value over time, which you can borrow against or withdraw. It’s more complex and typically more expensive than term life, often suitable for estate planning or long-term financial goals.

The choice between these often boils down to your budget, your long-term goals, and whether you want a policy that lasts your entire life or one that covers you for a specific period. Many financial experts, myself included, often recommend term life for most families, especially when you’re trying to maximize your coverage without breaking the bank. You can learn more about general life insurance concepts onInvestopedia.

The Cost Factor | What to Expect for Life Insurance in the USA

Let’s talk about life insurance cost . It’s a natural concern. The price you pay for your policy will depend on several factors:

- Age: Younger applicants generally pay less.

- Health: Your medical history, current health, and lifestyle habits (smoking, high-risk hobbies) significantly impact premiums.

- Coverage Amount: The higher the death benefit, the higher the premium.

- Policy Type: As discussed, term life is generally cheaper than whole life.

- Term Length: For term policies, longer terms (e.g., 30 years) are usually more expensive than shorter ones (e.g., 10 years).

It’s crucial to get quotes from multiple providers. Don’t just settle for the first offer. The market for life insurance in the USA is competitive, and rates can vary widely for similar coverage. And remember, the cheapest policy isn’t always the best; look for a reputable insurer with strong financial ratings.

When to Re-evaluate Your Coverage

Life isn’t static, and neither should your life insurance policy be. Major life events are perfect triggers to revisit your coverage and ensure it still aligns with your family’s needs. Think about:

- Getting married or divorced

- Having a child or adopting

- Buying a new home (especially with a larger mortgage)

- Significant salary increase or decrease

- Starting a business

- Children becoming financially independent

These moments fundamentally change your financial landscape and, consequently, your life insurance needs . It’s like regularly checking your car’s oil; a small check-up can prevent a big problem down the road.

Frequently Asked Questions About Life Insurance Coverage

Your Burning Questions, Answered.

What if I already have some life insurance through my employer?

That’s great! Employer-provided life insurance is a fantastic benefit, but it’s often not enough. It’s typically 1-2 times your annual salary, which might not cover all your family’s needs. Plus, it’s usually tied to your employment, meaning you lose it if you leave the job. Think of it as a good starting point, but rarely a complete solution.

Is it better to get term or whole life insurance?

For most families, especially those with significant, time-bound financial obligations like a mortgage or young children, term life insurance is often the more cost-effective and appropriate choice. It provides maximum coverage for the lowest premium. Whole life insurance can be suitable for specific long-term goals or estate planning, but it’s more expensive and complex.

Can I change my coverage amount later?

Yes, absolutely! Many term policies offer convertibility options to whole life, and you can often purchase additional term policies as your needs grow. It’s always a good idea to review your policy periodically with your agent, especially after major life events.

How much does life insurance cost per month in the USA?

The cost varies wildly based on age, health, coverage amount, and policy type. A healthy 30-year-old might pay $20-30 per month for a $500,000 20-year term policy, while someone older or with health issues would pay significantly more. Getting personalized quotes is the only way to know your exact life insurance cost .

What happens if I outlive my term life insurance policy?

If you outlive your term policy, the coverage simply ends, and you stop paying premiums. There’s no cash value payout. At that point, you can choose to purchase a new policy (though it will be more expensive due to your age), convert your existing term policy (if that option was available), or go without coverage if your financial obligations have diminished.

The Bottom Line | Don’t Leave It to Chance

Determining how much life insurance coverage do I need USA isn’t about fear; it’s about empowerment. It’s about taking control of your family’s financial destiny and ensuring that, no matter what, they are protected. It’s a complex decision, yes, but by breaking it down into manageable pieces – considering your debts, income replacement, mortgage, and future education costs – you can arrive at a figure that genuinely reflects your loved ones’ needs. Don’t just guess or rely on a quick online calculator. Take the time, do the math, and consult with a trusted financial professional. Your peace of mind, and your family’s future, are absolutely worth it.