Right, let’s be honest for a moment. Navigating the world of business insurance in the UK can feel like trying to solve a Rubik’s Cube blindfolded. It’s complex, full of jargon, and you’re constantly wondering if you’ve missed something crucial. But here’s the thing: it doesn’t have to be that way. My goal today is to cut through the noise, offering you a genuinely helpful, step-by-step guide to mastering your business insurance policy comparison UK . Think of me as your seasoned guide, helping you identify exactly what your business needs, where the pitfalls lie, and how to secure protection that truly protects, without breaking the bank. This isn’t just about finding the cheapest option; it’s about finding the right one.

I’ve seen countless businesses, from bustling startups to established SMEs, get tangled up in policies that either over-insure, under-insure, or simply don’t fit. A common mistake I see people make is rushing the process, often leading to regret when a claim arises. So, let’s roll up our sleeves and demystify this essential aspect of running a successful enterprise. We’ll cover the ‘how-to’ in detail, ensuring you walk away with the confidence to make an informed decision for your livelihood.

Why Comparing Isn’t Just Smart, It’s Essential (The “Why” Behind the “How”)

You might be thinking, “Surely, all business insurance is pretty much the same, right?” Oh, if only it were that simple! The truth is, the market for commercial insurance UK is incredibly diverse, with policies varying wildly in terms of coverage, exclusions, and, of course, price. Not taking the time for a proper comparison is akin to buying a car without test-driving it – you might end up with something that looks good on paper but fails to perform when it matters most.

Consider the implications: an unexpected incident – a client slipping on your premises, a data breach, or even an employee injury – can lead to significant financial liabilities. Without the correct cover, your business could face ruinous legal fees, compensation payouts, and reputational damage. The potential liability insurance cost UK alone can be staggering. My experience tells me that many businesses, especially smaller ones or those just starting, often underestimate their exposure. They might opt for what appears to be the cheapest business insurance UK without fully understanding its limitations. This approach, while tempting in the short term, often proves to be a false economy, leaving gaping holes in their protection. That’s why a diligent comparison isn’t just a good idea; it’s a fundamental pillar of risk management.

Decoding the Jargon | Key Types of Business Insurance You Need to Know

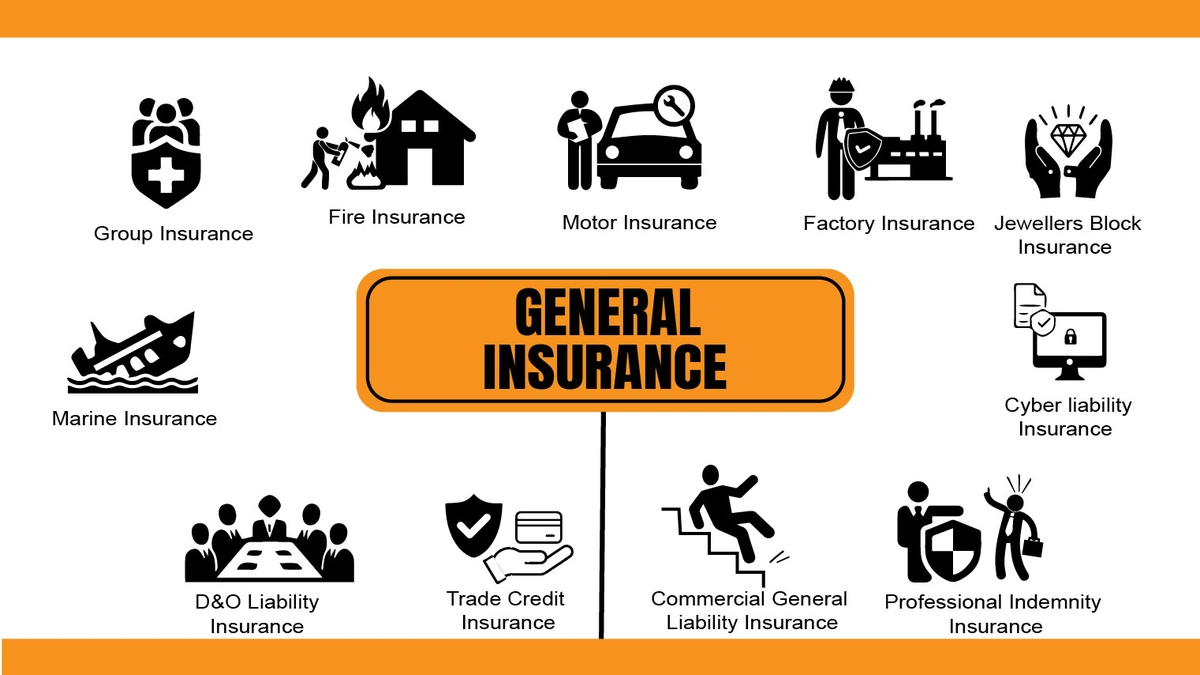

Before you even begin your business insurance policy comparison UK , you need to understand what you’re comparing. The world of insurance is rife with specific terms, and knowing them is half the battle. Here are the core types of business insurance UK that most enterprises consider:

- Professional Indemnity Insurance: If your business offers advice, design, or services (think consultants, designers, IT professionals), this is crucial. It protects you against claims of negligence, errors, or omissions in your professional service. The need for a robust professional indemnity insurance comparison cannot be overstated.

- Public Liability Insurance: Essential for any business interacting with the public. It covers claims made against you for injury or property damage caused by your business activities. For instance, if a customer trips over a loose cable in your shop.

- Employers’ Liability Insurance: A legal requirement for almost all UK businesses with employees, even temporary staff. It covers claims from employees who suffer injury or illness as a result of their work.

- Contents and Equipment Insurance: Protects your physical assets – office furniture, computers, machinery – against theft, damage, or loss.

- Cyber Insurance: Increasingly vital in our digital age, this covers losses and damages related to cyberattacks, data breaches, and other digital risks.

- Product Liability Insurance: If you manufacture, supply, or sell products, this protects you against claims for injury or damage caused by a faulty product.

Understanding these foundational types is your first step. It allows you to tailor your search and avoid paying for coverage you don’t need, or worse, missing out on cover you absolutely do.

Your Step-by-Step Blueprint for a Winning Business Insurance Policy Comparison UK

Now, let’s get down to the practicalities. This is where the rubber meets the road. Follow these steps to ensure you’re making a truly informed decision:

Step 1 | Assess Your Unique Risks

Before you even look at a quote, sit down and honestly evaluate your business. What are its specific vulnerabilities? Are you client-facing? Do you handle sensitive data? Do you operate heavy machinery? What’s your business structure (sole trader, limited company)? This initial risk assessment is paramount. It dictates which types of insurance are non-negotiable for you. For example, a freelance graphic designer will have very different needs than a construction company, particularly when considering insurance for self-employed UK options.

Step 2 | Gather All Necessary Information

Insurers will ask for specific details. Have these ready: your business type, industry, annual turnover, number of employees, payroll figures, details of any previous claims, and specific assets you want to cover. Being prepared will make the quoting process much faster and more accurate, helping you get reliable small business insurance quotes.

Step 3 | Decide on Your Comparison Method | Online vs. Broker

You have two main avenues: online comparison websites or a dedicated business insurance broker UK.

- Online Comparison Sites: Great for getting quick, indicative quotes, especially for simpler, more standardised policies. They allow you to rapidly compare prices from multiple providers. However, they might not always capture the nuances of a complex business.

- Insurance Broker: For more intricate businesses or if you value personalised advice, a broker can be invaluable. They have in-depth market knowledge, can negotiate on your behalf, and often have access to policies not available directly to the public. They act as your advocate, helping you navigate the complexities and understand the fine print.

Step 4 | Scrutinise Beyond the Price Tag

This is where many go wrong. The cheapest option isn’t always the best. When conducting your business insurance policy comparison UK , look closely at:

- Coverage Limits: Are the maximum payouts sufficient for your potential risks?

- Exclusions: What isn’t covered? These are often hidden in the small print and can be critical.

- Excess: This is the amount you pay towards a claim. A higher excess usually means lower premiums, but can you afford it if you need to claim?

- Policy Wording: Understand the terms and conditions. If something is unclear, ask!

- Insurer’s Reputation: How good is their customer service? How quickly do they process claims? Online reviews can offer insights here.

Step 5 | Review and Re-evaluate Annually

Your business isn’t static, so your insurance shouldn’t be either. Make it a habit to review your policies annually, or whenever there’s a significant change in your business operations. This ensures your coverage remains relevant and cost-effective.

Finding the Sweet Spot | Balancing Cost and Coverage

The quest for the cheapest business insurance UK is understandable. Every penny counts when you’re running a business. But as we’ve discussed, cutting corners on insurance can be a perilous game. The real sweet spot lies in balancing cost with comprehensive, adequate coverage. It’s about value, not just price.

I often advise clients to think about the worst-case scenario. If that scenario came to pass, would your current policy genuinely protect you, or would it leave you exposed? Sometimes, paying a little extra for a policy with broader coverage or lower excesses can provide immense peace of mind and ultimately save you a fortune should a claim arise. Don’t be afraid to ask for different quotes with varying levels of coverage. For more insights into securing your business, consider exploringbusiness insurance optionson our site.

FAQs | Your Burning Questions Answered

How often should I compare business insurance policies?

Ideally, you should compare your business insurance policy comparison UK options annually, typically before your renewal date. This ensures your coverage remains relevant and you’re getting the best possible price for your current business needs. However, if your business undergoes significant changes – like hiring new staff, expanding services, or acquiring new assets – you should review your policy immediately.

Can I get business insurance if I’m self-employed in the UK?

Absolutely! Many insurers offer tailored insurance for self-employed UK policies. Depending on your profession, you might need Professional Indemnity, Public Liability, or even specific tool insurance. It’s crucial to assess your individual risks as a sole trader or freelancer to ensure adequate protection.

What if my business changes significantly after I’ve taken out a policy?

You must inform your insurer about any material changes to your business. This could include a change in services, an increase in turnover, hiring new employees, or moving premises. Failing to do so could invalidate your policy, leaving you unprotected when you need it most.

Are online business insurance quotes reliable?

Online quotes are a great starting point for getting an idea of prices and coverage, especially for straightforward businesses. However, for more complex operations, they might not capture all the nuances. Always read the policy documents carefully, and consider speaking to a broker for tailored advice to ensure you fully understand what you’re buying. For general insurance knowledge, you can also visitour main insurance portal.

What’s the difference between Public Liability and Product Liability insurance?

Public Liability covers claims for injury or damage to third-party property caused by your business operations (e.g., a customer trips in your shop). Product Liability, on the other hand, covers claims for injury or damage caused by a faulty product that your business manufactures, supplies, or sells.

Final Thoughts | Take Control of Your Protection

Look, running a business is challenging enough without the added worry of inadequate insurance. Taking the time to properly conduct a business insurance policy comparison UK isn’t just a chore; it’s an investment in your peace of mind and the long-term viability of your enterprise. Don’t let the complexity deter you. By understanding your needs, decoding the jargon, and diligently comparing options, you’re not just buying a policy – you’re building a robust shield around your hard work and aspirations. Remember, proactive protection is always better than reactive damage control. Be smart, be thorough, and secure the future of your business.