Let’s be honest, navigating the world of insurance can feel like trying to solve a Rubik’s Cube blindfolded. Especially when it comes to something as crucial aslife insurance. You know you need it, you want to protect your loved ones, but the sheer thought of figuring out what you’ll pay for a term life insurance premium calculator USA can send shivers down your spine. Am I right? I’ve seen countless folks (and been one of them!) just punch in a few numbers, get a quote, and either feel overwhelmed or just pick the cheapest option without really understanding what they’re getting into.

Here’s the thing: you don’t have to be an actuary to understand your life insurance cost . What if I told you there’s a way to not just use a term life insurance premium calculator USA but to truly master it? To understand the levers that move your life insurance premiums and, more importantly, how to secure the best term life insurance rates for your unique situation? That’s exactly what we’re going to do today. Think of me as your guide, sitting across from you with a cup of chai, breaking down the jargon and showing you the simple, actionable steps to take control of yourfinancial planning.

Why Most People Overpay | Understanding the Hidden Factors Affecting Your Premium

When you first look at a premium calculator , it seems straightforward, doesn’t it? Age, gender, smoking status. But I initially thought this was the whole picture, and then I realized there’s so much more beneath the surface. The truth is, your premium isn’t just pulled out of thin air. It’s a sophisticated calculation based on risk – your risk to the insurance company. And understanding these factors affecting life insurance premiums is your first step to getting a better deal.

Let’s break down the major players:

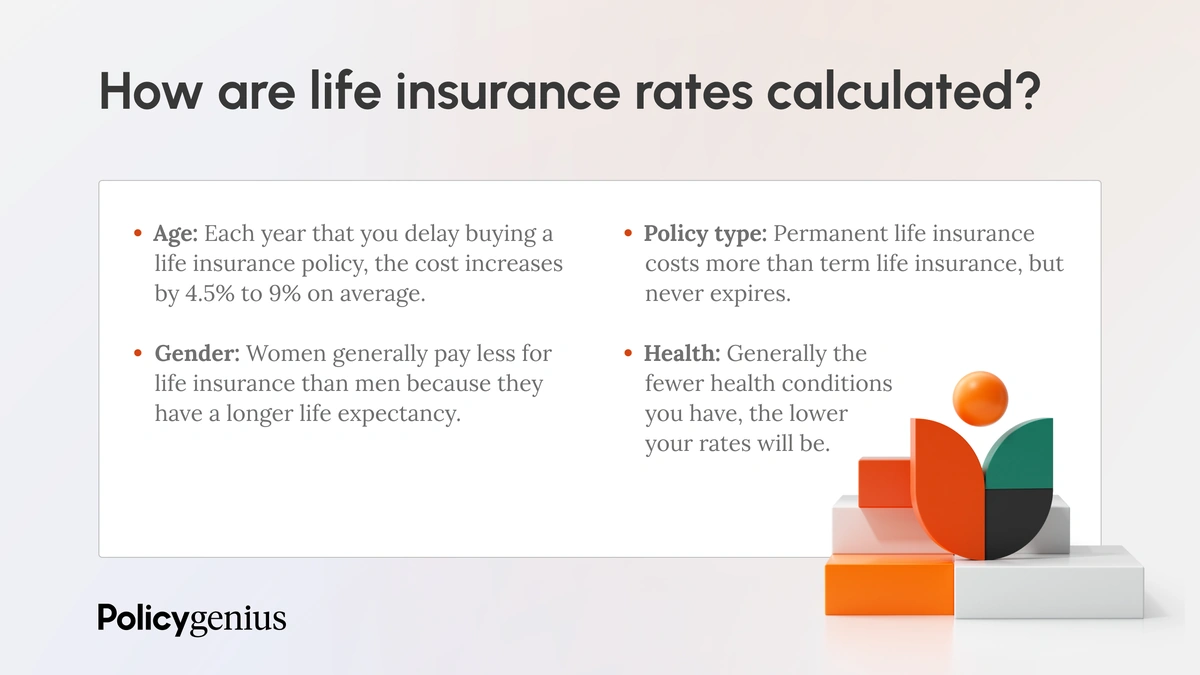

- Age: This one’s a no-brainer. The younger you are, generally the lower your life insurance cost. Why? Because you’re statistically less likely to pass away during the policy term. Every year you delay, those rates creep up. It’s not a scare tactic; it’s just how the math works.

- Health & Medical History: This is arguably the biggest determinant. Insurers want to know everything: your current health, past illnesses, family medical history (especially for critical conditions like heart disease or cancer), and even your cholesterol and blood pressure readings. A healthy lifestyle and clean bill of health can significantly reduce your insurance rates. Be honest here; discrepancies can lead to claims being denied later, which defeats the entire purpose.

- Lifestyle: Do you skydive on weekends? Work in a hazardous profession? Even your driving record can play a role. The riskier your hobbies or job, the higher your premium might be. On the flip side, being a non-smoker is a huge advantage. If you quit smoking, you might even qualify for better rates after a certain period (usually 12-24 months).

- Coverage Amount & Term Length: This is where your coverage needs come in. Naturally, a $1 million policy will cost more than a $250,000 policy. Similarly, a 30-year term policy will generally cost more than a 10-year term because the insurer is taking on risk for a longer period. This is a critical balancing act – you want enough coverage, but not so much that it becomes unaffordable.

- Gender: Historically, women have paid less for term life insurance than men because, on average, they live longer. While this is a general trend, individual factors always override broad statistics.

Understanding these elements is like having an X-ray vision into the insurer’s decision-making process. It empowers you to not just accept a quote, but to question it, and even strategize how you might improve your standing.

Your Step-by-Step Playbook | Using a Term Life Insurance Premium Calculator Like a Pro

Okay, now that we know why premiums are what they are, let’s get practical. The term life insurance premium calculator USA isn’t just a tool; it’s your personal financial compass. But like any powerful tool, knowing how to use it properly makes all the difference. I’ve seen people rush through this, missing crucial details, and ending up with wildly inaccurate estimates. Let’s make sure that’s not you.

Here’s how to truly leverage it:

- Start with Your Needs, Not Just a Number: Before you even touch a calculator, think about your coverage needs. How much debt do you have (mortgage, car loans, student loans)? How many years until your kids are financially independent? What about your spouse’s income replacement? A good rule of thumb is 5-10 times your annual income, plus outstanding debts and future expenses. Don’t guess; make a rough list. This initial step is vital for getting meaningful online life insurance quotes.

- Gather Your Basic Information: Have your exact age, gender, and smoking status ready. Be honest! If you recently quit, note the date.

- Be Prepared for Health Questions: While an initial premium calculator might just ask “Excellent, Good, Fair, Poor” for health, understand that a real application will dig much deeper. Think about any medical conditions, medications, or significant family history. Even if the calculator doesn’t ask for granular detail, having this information in your mind helps you interpret the initial estimate more realistically.

- Input Your Desired Term Length: Most term life insurance policies come in 10, 15, 20, 25, or 30-year increments. Match this to your financial obligations. If your mortgage will be paid off in 15 years and your kids will be through college in 20, a 20-year term might be perfect.

- Run Multiple Scenarios: This is a pro tip. Don’t just run one calculation. Try different coverage amounts and term lengths. What if you need $750,000 instead of $1 million? What if you choose a 20-year term instead of 30? This helps you understand the elasticity of your potential life insurance cost and find a sweet spot that fits your budget and protection goals.

- Understand the “Quote” vs. “Actual Premium”: An online life insurance quotes from a calculator is an estimate. Your actual premium will only be determined after a full underwriting process, which might include a medical exam and review of your records. Don’t get disheartened if your final rate is slightly higher; the calculator provides an excellent starting point for your financial planning.

By following these steps, you’re not just using a tool; you’re engaging in smart financial strategy. You’re moving from a passive recipient of information to an active participant in securing your financial future.

Beyond the Numbers | How to Choose the Right Policy and Get the Best Rates

So, you’ve played around with the term life insurance premium calculator USA, you’ve got some online quotes, and you’re feeling more confident. Fantastic! But the journey doesn’t end there. Now comes the crucial part: choosing the right policy and ensuring you’re truly getting the best term life insurance rates. This is where your expertise, combined with a bit of savvy comparison, really pays off.

One common pitfall I see is people getting stuck on just the cheapest price. While affordable term life insurance is a goal, it’s not the only goal. You need the right coverage at an affordable price. Here’s how to navigate this:

Comparing Apples to Apples | Term vs. Whole Life Insurance

Before diving deep into specific term policies, it’s worth a quick refresher on the fundamental difference. Term vs whole life insurance is a classic debate. Term life is straightforward: it covers you for a specific period (the “term”) and pays out if you die within that term. It’s generally much more affordable because it doesn’t build cash value. Whole life, on the other hand, covers you for your entire life and includes a savings component. For most families looking for pure protection during their peak earning and debt-accumulation years, term life insurance is the more practical andcost-effective choice.

Finding the Best Term Life Insurance Rates

Once you’ve decided on term, here’s how to refine your search for those elusive best term life insurance rates:

- Shop Around, Seriously: Don’t just get a quote from one company. Every insurer has different underwriting guidelines and target demographics. What might be expensive with one could be significantly cheaper with another, especially if you have a unique health profile. Use independent brokers or aggregator sites that compare multiple carriers. This is where a good life insurance cost estimator can point you to various providers.

- Consider Laddering Policies: This is an advanced strategy, but incredibly smart. Instead of one large 30-year policy, you might buy a 20-year policy for a certain amount and a 10-year policy for a smaller amount. As your financial obligations decrease (kids grow up, mortgage gets paid), you can let the shorter, smaller policies expire, reducing your overall life insurance cost over time.

- Review Riders: These are add-ons to your policy. Some can be incredibly useful (like a “waiver of premium” rider if you become disabled), while others might be unnecessary and just add to your premium. Understand what each rider does and if it truly adds value for your situation.

- Lock in Rates Early: As we discussed, age is a major factor. The younger and healthier you are when you purchase your term life insurance, the lower your rates will be for the entire term of the policy. This is why financial planning often emphasizes getting coverage sooner rather than later.

- Re-evaluate Periodically: Life changes! Marriage, kids, a new home, a significant pay raise, or debt reduction can all impact your coverage needs. It’s a good idea to revisit your term life insurance premium calculator USA and your existing policy every 3-5 years, or after any major life event, to ensure you’re still adequately protected without overpaying.

Ultimately, securing the right term life insurance policy isn’t about finding the absolute cheapest number on a screen. It’s about finding the sweet spot where robust protection for your loved ones meets an affordable term life insurance premium that fits comfortably into your budget. It’s about peace of mind, knowing that you’ve done your due diligence and made an informed decision.

Frequently Asked Questions About Term Life Insurance Premiums

What is a term life insurance premium calculator USA used for?

A term life insurance premium calculator USA is an online tool designed to provide an estimate of how much you might pay for a term life insurance policy. You input details like age, gender, health status, desired coverage amount, and term length, and it generates an approximate premium. It’s a great starting point for understanding your potential life insurance cost.

How accurate are online life insurance quotes?

Online life insurance quotes from a calculator are generally good estimates, but they are not binding. The final premium can only be determined after a full underwriting process, which typically involves a medical exam, review of your medical records, and a detailed assessment of your lifestyle. Factors like specific health conditions, medications, or hazardous hobbies might adjust the final rate.

What factors affect term life insurance premiums the most?

The most significant factors affecting life insurance premiums are your age, current health status (including medical history), and the coverage amount and term length you choose. Generally, younger, healthier individuals seeking less coverage for a shorter term will have lower insurance rates.

Can I get affordable term life insurance if I have a pre-existing condition?

Yes, it’s often possible to get affordable term life insurance even with a pre-existing condition, though your premiums might be higher than someone with perfect health. It’s crucial to be honest about your health history during the application process. Different insurers have varying underwriting guidelines, so shopping around with multiple carriers or using an independent broker can help you find the best term life insurance rates.

Is term life insurance better than whole life insurance?

Neither is inherently “better”; it depends on your specific coverage needs and financial goals. Term life insurance is often recommended for pure protection for a specific period (e.g., until your kids are grown or your mortgage is paid off) because it’s significantly more affordable. Whole life insurance offers lifelong coverage and a cash value component, making it suitable for different long-term financial strategies. For most people focused on maximizing protection for their family during their working years, term life is usually the more straightforward and cost-effective choice.

How often should I re-evaluate my term life insurance policy?

It’s a good practice to re-evaluate your term life insurance policy every 3-5 years, or after any major life event. This includes getting married, having children, buying a home, taking on significant debt, or experiencing a substantial change in income. Re-running a term life insurance premium calculator USA and reviewing your existing policy helps ensure your coverage still aligns with your current financial planning and protection needs.

So, there you have it. You’re not just looking for a number anymore; you’re equipped with the knowledge to actively seek out and secure the ideal term life insurance protection for your family. This isn’t just about saving a few bucks; it’s about making informed decisions that bring genuine peace of mind. Go forth, calculate, compare, and protect what matters most!