Picture this: you’ve poured your heart, soul, and countless hours into building your dream business here in India. You’ve got the talent, the clients, and the drive. Everything seems to be running smoothly, right? But what if I told you there’s a lurking vulnerability, a silent threat that could dismantle everything you’ve worked for, even if you do everything right?

Here’s the thing about being a professional in today’s dynamic landscape, especially for service providers: perfection is an impossible standard, and perception is often reality. Even the most meticulous architect, the most diligent IT consultant, or the sharpest financial advisor can face a client accusation. And that, my friends, is where the real drama, and potentially the real financial pain, begins.

We’re talking about professional indemnity insurance for business. Now, I know what you might be thinking: “Another insurance policy? Isn’t general liability enough?” Let me tell you, it’s not. Not when your reputation, your future, and your bank account are on the line. This isn’t just another item on a checklist; it’s a strategic shield, a critical part ofcomprehensive business insurance optionsthat many unfortunately overlook until it’s too late. Today, we’re diving deep into the ‘why’ – why this specific insurance isn’t just good to have, but absolutely essential for any business offering professional services.

Beyond the Blame Game | Understanding Professional Indemnity’s Core “Why”

So, why exactly does professional indemnity insurance matter so profoundly for Indian businesses? It boils down to the very nature of professional services. Unlike a product that might be physically defective, your service is intellectual. It’s advice, design, analysis, code, or consultation. The ‘defects’ here are often subjective, based on a client’s expectations, perceived negligence, or even a simple misunderstanding that snowballs into a serious accusation.

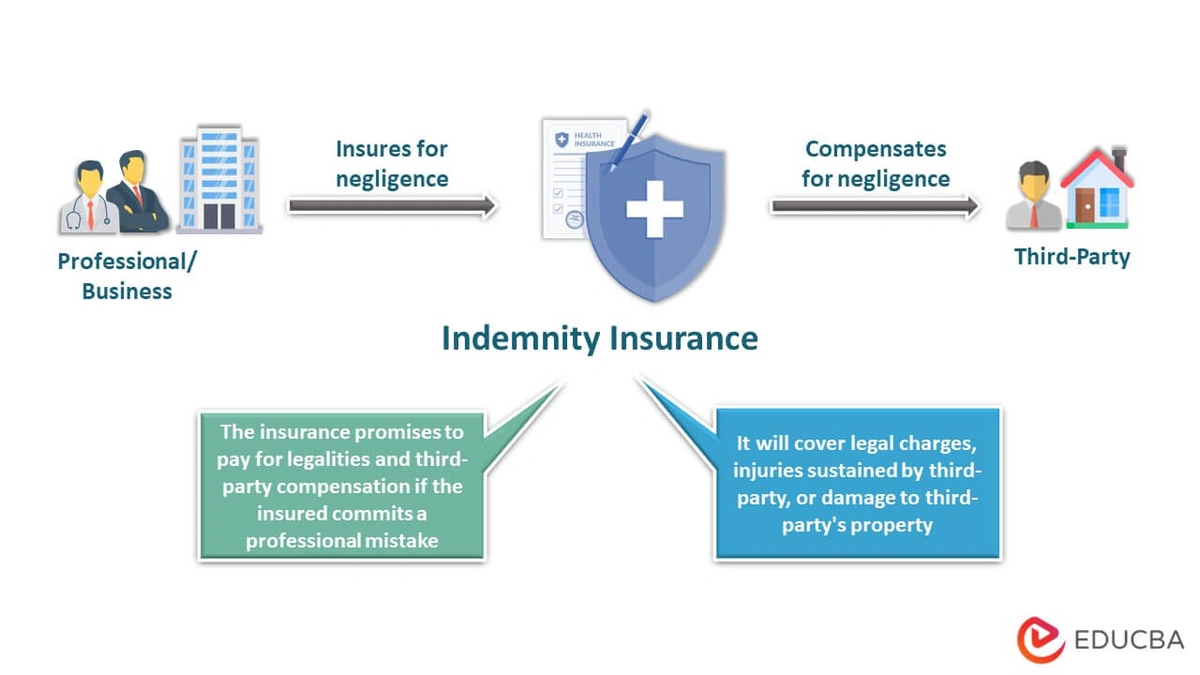

The core purpose of professional indemnity insurance for business is to protect you from claims of financial loss made by a client due to an error, omission, or negligent act in the professional services you provide. Think about it: a software developer misses a critical bug, an accountant makes a calculation error, a marketing agency gives advice that doesn’t yield expected results, or even an architect whose design leads to unexpected structural issues down the line. In each of these scenarios, the client could allege that your professional failing caused them a financial detriment. This isn’t about someone slipping on a wet floor in your office; that’s general liability territory. This is about the very expertise you sell.

What fascinates me is how often businesses, especially startups and SMEs, conflate this with general liability. General liability covers physical injury or property damage – the ‘oops’ moments. But professional indemnity (often referred to as professional liability insurance or errors and omissions (E&O) insurance India) covers the ‘oops, I made a mistake in my professional judgment or service delivery’ moments. The distinction is crucial because the financial implications of professional negligence claims can be staggering, encompassing not just compensation but also formidable legal costs for defense, whether you’re at fault or not. And let’s be honest, fighting a legal battle, even if you’re eventually exonerated, can drain resources, time, and morale like nothing else.

The Hidden Traps | What Risks Does It Really Cover?

It’s easy to dismiss the need for professional indemnity insurance if you believe your work is flawless. But the reality is that claims can arise from a myriad of situations, some of which you might not even consider as ‘mistakes.’ Let me walk you through a few common pitfalls:

- Errors and Omissions: This is the most straightforward. You overlooked a crucial detail in a report, an engineer made a miscalculation, or a consultant provided incorrect advice. These simple human errors can have significant financial repercussions for your client.

- Negligence: A client might claim you failed to exercise the due care and skill expected of a professional in your field. This could be anything from a delayed project that caused financial loss to a poorly executed service.

- Misrepresentation or Breach of Duty: Accusations that you misrepresented your capabilities, failed to deliver on a promise, or breached a professional duty can also trigger a claim.

- Breach of Confidentiality: In our data-driven world, accidental disclosure of sensitive client information, even unintentional, can lead to massive claims and reputational damage.

- Loss of Documents or Data: Imagine losing critical client documents or digital data. The cost of recovery, potential fines, and client compensation can be immense.

- Defamation or Libel: While less common, claims can arise if a client believes your professional communication (e.g., a published report or analysis) defamed them.

The insidious thing about these risks is that they aren’t always immediately apparent. A mistake made today could lead to a claim years down the line. This is particularly relevant for Indian service providers across sectors like IT, finance, legal, marketing, engineering, and healthcare. For instance, a small architectural firm might face a claim years after a building’s completion due to an unforeseen structural issue. Without adequate indemnity cover benefits, such a claim could easily bankrupt the firm.

The legal landscape in India is evolving, with increasing consumer awareness and a greater propensity for clients to seek recourse. Navigating these professional negligence claims requires expert legal defense, which, as anyone who’s dealt with legal matters knows, doesn’t come cheap. That’s why legal expenses coverage within your PI policy is a lifesaver, covering your defense costs whether the claim is valid or baseless.

More Than Just a Policy | The Strategic Advantage for Indian Businesses

Beyond simply protecting you from financial ruin, acquiring professional indemnity insurance for business offers a significant strategic advantage that forward-thinking Indian enterprises understand. It’s not just about covering your backside; it’s about bolstering your front. Consider these aspects:

- Enhanced Credibility and Client Trust: When you tell a potential client that you are professionally insured, it sends a powerful message. It signals that you are serious about your work, you stand by your services, and you have taken responsible steps to protect them (and yourself) if things go wrong. This significantly enhances your credibility, especially when pitching for larger projects or working with international clients who often mandate such coverage. It tells them you understand the inherent risks of your profession and are prepared for them.

- Meeting Contractual Requirements: Increasingly, larger corporations, government bodies, and even savvy individual clients in India are making professional indemnity insurance a mandatory contractual requirement before engaging your services. Without it, you might be locked out of lucrative opportunities. Having a policy in place means you’re ready to seize these chances without delay.

- Peace of Mind and Focus: Let’s be honest, the threat of a potential lawsuit is a huge distraction. It saps energy, creativity, and focus. Knowing you have robust financial protection in the form of a PI policy allows you to concentrate on what you do best: serving your clients and growing your business, rather than constantly looking over your shoulder. This is fundamental for effective risk management for professionals.

- Attracting and Retaining Talent: For professional firms, demonstrating a commitment to protecting both the firm and its individual professionals can be a key factor in attracting and retaining top talent. Employees want to know that their employer has their back in case of an honest mistake.

It’s about proactively managing risk, not reactively responding to disaster. This proactive stance is what differentiates a sustainable business from one that’s constantly teetering on the edge. By investing in errors and omissions insurance, you’re investing in your own longevity and stability. I recall a conversation with a seasonedconsultant insurance Indiaexpert who said, “It’s not if you’ll face a claim, but when. And when you do, you’ll be glad you planned ahead.” That wisdom, I think, resonates deeply.

Navigating the Nuances | Key Things to Know About Your PI Policy

Alright, you’re convinced you need it. Now, how do you actually get the right professional indemnity insurance for business that fits your specific needs? This isn’t a one-size-fits-all product; understanding the nuances is critical.

The most important distinction you’ll encounter is between ‘claims-made’ and ‘occurrence-based’ policies. Almost all professional indemnity policies are written on a claims-made basis. This means the policy that is active when the claim is first made against you is the one that responds, regardless of when the alleged error or omission actually occurred. This is a crucial point, especially if you cease operations or change insurers. You might need ‘run-off cover’ to protect against future claims arising from past work. Always clarify this with your insurer.

Other vital considerations include:

- Coverage Limits: How much cover do you really need? This isn’t a guess. Consider your project sizes, the potential for financial loss your services could cause, and any contractual requirements. Too little coverage leaves you exposed; too much might be an unnecessary expense.

- Deductible/Excess: This is the amount you pay out of pocket before the insurance kicks in. A higher deductible usually means a lower premium, but ensure it’s an amount you can comfortably afford in case of a claim.

- Retroactive Date: This specifies how far back your policy will cover work done. Ideally, it should cover all your past work since the inception of your business or your first professional engagement.

- Exclusions: Every policy has them. Read the fine print! Common exclusions might include fraud, dishonest acts, bodily injury (covered by general liability), or pre-existing claims.

- Reporting Period: After a policy expires or is cancelled, you typically have a short window (the reporting period) to report any new claims arising from work performed during the policy period.

Choosing the right provider is also paramount. Look for insurers with a strong track record in India, transparent policy wordings, and excellent claims-handling services. Don’t just go for the cheapest option; focus on value and comprehensive coverage. Engaging with a specialist broker can be incredibly helpful here, as they can tailor a policy to your specific profession – whether you’re a software developer, an independent consultant, or an entire engineering firm.

As per the latest guidelines from the Insurance Regulatory and Development Authority of India (IRDAI), insurers are increasingly standardising certain aspects, but the specifics still vary significantly. It’s best to consult official sources likeIRDAI’s websiteor reputable insurance advisors to understand the regulatory landscape and ensure compliance. Remember, a policy isn’t just paperwork; it’s a promise, and you want that promise to hold up when you need it most.

Ultimately, investing in professional indemnity insurance isn’t about admitting you’ll make mistakes; it’s about acknowledging that you operate in a complex world where even the best professionals can face unforeseen challenges. It’s about building a robust, resilient business capable of weathering any storm, offering peace of mind, and ensuring long-term prosperity.

Frequently Asked Questions (FAQs)

Who specifically needs professional indemnity insurance?

Any individual or business that provides advice, design, or services based on their professional knowledge or skills can benefit. This includes, but isn’t limited to, consultants (IT, management, marketing), architects, engineers, accountants, lawyers, financial advisors, software developers, graphic designers, advertising agencies, real estate agents, and even healthcare professionals. If a client could potentially sue you for a financial loss resulting from your professional service, you likely need it.

Is professional indemnity insurance mandatory in India?

For certain professions, yes, it is legally mandated by their respective regulatory bodies (e.g., medical practitioners, lawyers, chartered accountants for specific activities). For others, while not legally mandatory, it’s often a contractual requirement by clients, especially larger corporations or government entities. Even when not mandatory, it’s highly recommended for risk mitigation.

How is the premium for professional indemnity insurance calculated?

Premiums depend on several factors: your profession (higher risk professions generally have higher premiums), your business turnover, the sum insured (the maximum amount the policy will pay out), your claims history, the number of employees, the geographical scope of your work, and the deductible chosen. Insurers assess the potential for professional negligence claims based on these variables.

What’s the difference between professional indemnity and general liability insurance?

General liability insurance covers claims for bodily injury or property damage that occur on your business premises or as a result of your business operations. Think a client tripping over a loose rug. Professional indemnity insurance, on the other hand, covers claims for financial loss due to errors, omissions, or negligence in the professional services or advice you provide. It protects your expertise, not just your premises.

Can I get professional indemnity for a freelance business?

Absolutely, and many freelancers in India find it indispensable! As a freelancer, you often bear the full brunt of any claims against your work. A dedicated consultant insurance India policy tailored for individuals or small businesses can provide crucial financial protection against potential lawsuits, giving you peace of mind and enhancing your professional standing with clients.

What happens if I make a claim?

If you face a claim or even a potential claim, you should notify your insurer immediately, as per your policy terms. They will guide you through the process, which typically involves an investigation, legal defense (covered by your policy), and potentially settlement or court proceedings. The insurer will generally handle the legal aspects and financial compensation, subject to your policy limits and deductible.