Let’s be honest, talking about health insurance isn’t exactly a thrilling Friday night activity. But what is thrilling? The peace of mind that comes from knowing your loved ones are protected, come what may. In India, with healthcare costs soaring faster than a cricket ball hit for six, choosing the best health insurance for family isn’t just a smart move; it’s an absolute necessity. But where do you even begin? The options seem endless, the jargon confusing, and the fear of picking the wrong plan? That’s real.

I’ve seen countless families struggle with this very decision, often feeling overwhelmed and even paralyzed by choice. The goal here isn’t to just tell you what to do, but to guide you, step-by-step, through the process as if we’re sitting across from each other, sipping chai. We’ll cut through the noise, demystify the terms, and equip you to make an informed decision for your family’s health security. Because when it comes to health, there’s no room for guesswork, only clarity.

The “Why Now” Behind Family Health Insurance | More Than Just a Policy

Why is everyone suddenly talking about `family floater plan`s and comprehensive health covers? It’s not just a trend; it’s a reflection of our changing times. Medical inflation in India is alarmingly high, often in double digits. A simple fever could mean an outpatient consultation, but a sudden surgery or a chronic illness can wipe out years of savings faster than you can say “cashless hospitalization.”

Think about it: a critical illness affecting one member can put immense financial strain on the entire household. This is precisely why having robust `health insurance benefits India` offers is paramount. It’s not just about covering hospital bills; it’s about safeguarding your family’s financial future, ensuring that health setbacks don’t translate into financial ruin. The hidden context here is that relying solely on personal savings, however substantial, is a high-stakes gamble in today’s medical landscape. A dedicated `health plan for family` acts as that crucial safety net, allowing you to focus on recovery rather than the exorbitant bills.

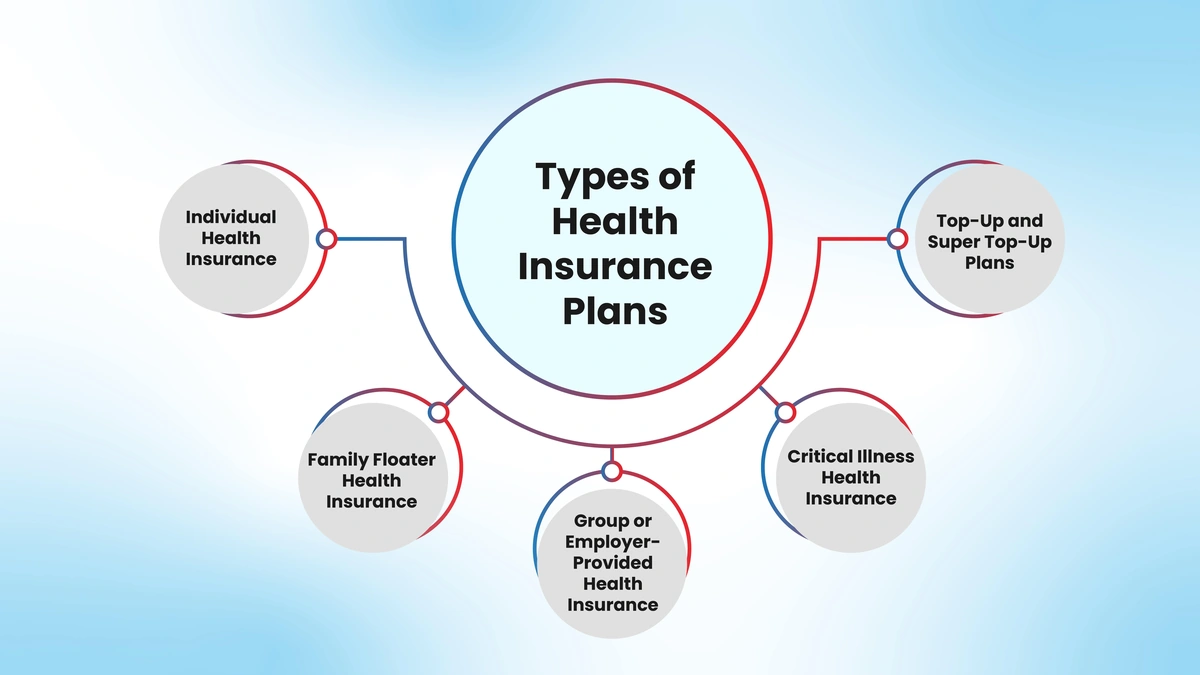

Decoding the Jargon | Key Terms You Must Know Before You Buy

Alright, let’s tackle the elephant in the room: the terminology. Insurance documents can feel like they’re written in another language, right? But understanding a few core concepts will make your `health insurance comparison` journey infinitely smoother. Here’s what you absolutely need to know:

1. Family Floater Plan: This is arguably the most popular type of best health insurance for family in India. Instead of each member having a separate policy, a single sum insured (more on that next!) floats among all family members covered under the policy. So, if your `sum insured family health` is ₹10 Lakhs, any family member can utilize up to that entire amount for their medical needs during the policy year. It’s often more cost-effective than individual policies for families, especially nuclear ones.

2. Sum Insured (SI): This is the maximum amount your insurance company will pay out in a policy year. Choosing the right SI is crucial. For a family in a metro city, a ₹5-10 Lakh sum insured might be a good starting point, but with rising costs, many are now opting for ₹15-25 Lakhs or even more. My advice? Don’t skimp here. A higher `sum insured family health` offers better protection against severe medical emergencies.

3. Cashless Hospitalization: This is a godsend. When you get admitted to a network hospital (one that has an agreement with your insurer), your bills are settled directly by the insurance company. No running around for cash, no submitting lengthy reimbursement forms post-discharge. This feature, enabling `cashless hospitalization`, is a huge relief during stressful times. Always check the insurer’s network hospitals in your city!

4. Waiting Period: Ah, the not-so-fun part. Most policies have a waiting period before certain conditions are covered. This can include an initial waiting period (e.g., 30 days for any illness except accidental injuries), waiting periods for specific diseases (e.g., 2-4 years for cataracts or joint replacements), and a waiting period for pre-existing diseases (often 2-4 years). Understanding the `waiting period health insurance` entails is vital to avoid nasty surprises later.

Your Step-by-Step Playbook | How to Compare & Pick the Best Plan

Now that we’ve got the basics down, let’s get practical. How do you actually go about finding the best health insurance for family ? It’s a bit like being a detective, looking at clues and piecing them together. Here’s my foolproof playbook:

- Assess Your Family’s Needs: This is the foundation. Do you have elderly parents? Young children? Are there any pre-existing conditions? Does anyone have a family history of `critical illness cover family` conditions? If you’re planning a family, consider policies with `maternity cover family plan` benefits. Your family’s unique profile will dictate the type of coverage you need. For example, if you have parents over 60, a separate senior citizen policy might sometimes be better than adding them to a floater plan, depending on the terms.

- Determine the Right Sum Insured: We talked about this, but it bears repeating. Don’t just pick an arbitrary number. Consider the cost of major surgeries in your city, the duration of potential hospital stays, and future medical inflation. An `affordable family health insurance` plan isn’t always the cheapest one; it’s the one that provides adequate coverage without leaving you vulnerable.

- Compare Beyond the Premium: This is where most people make a mistake. They only look at the `health insurance premium`. While important, it’s only one piece of the puzzle. Look at the coverage scope, sub-limits (caps on specific treatments like room rent), co-payment clauses (where you pay a percentage of the bill), and exclusions. A slightly higher premium might get you significantly better coverage and fewer restrictions. Seriously, dive into the policy wording!

- Check for Inclusions & Exclusions: Does the policy cover daycare procedures? Home healthcare? Organ donor expenses? What about specific conditions like mental health treatments? Equally important are the exclusions – what the policy won’t cover. Many policies, for instance, don’t cover cosmetic surgery or self-inflicted injuries. Be meticulous here.

- Network Hospitals and Claim Settlement Ratio: For `cashless hospitalization` to be truly effective, your preferred hospitals should be in the insurer’s network. Also, research the insurer’s Claim Settlement Ratio (CSR). This ratio, published by IRDAI, tells you the percentage of claims an insurer settles in a year. A higher CSR (say, above 90-95%) indicates a more reliable company.

Beyond the Basics | Tax Benefits & What Else to Look For

Choosing a good `medical insurance for family` isn’t just about protecting your health; it can also be a smart financial move, thanks to `tax benefits health insurance` offers under Section 80D of the Income Tax Act. You can claim deductions on premiums paid for yourself, your spouse, dependent children, and even your parents. This small perk makes health insurance even more attractive.

But beyond the financial incentives, consider these additional factors:

- Restoration Benefit: Some policies offer a ‘restore benefit’, meaning if your sum insured is exhausted in a year, it gets replenished once, often for unrelated illnesses. This is a powerful feature for comprehensive protection.

- No-Claim Bonus (NCB): For every claim-free year, your sum insured can increase, or your premium can decrease. It’s a nice reward for staying healthy!

- Add-ons/Riders: Many policies allow you to customize your coverage with riders like `critical illness cover family` (for specific life-threatening diseases), personal accident cover, or even daily hospital cash. Don’t just blindly add them, though. Evaluate if they truly align with your family’s specific risks and needs.

- Customer Service: This is intangible but vital. When you need to make a claim, you want responsive and helpful customer service. Read reviews, ask for recommendations, and consider the reputation of the `top health insurance companies India` has to offer. A smooth claim process is priceless.

Common Pitfalls & How to Dodge Them

I’ve witnessed many families stumble, often making preventable mistakes. Here’s what to watch out for:

A common mistake I see people make is underinsuring their family. They go for the lowest `health insurance premium` thinking any cover is better than none. But what if a major illness strikes and your ₹5 Lakh policy is exhausted in a week? You’ll be left footing the rest of the bill. Always aim for adequate, not just affordable, coverage.

Another pitfall is not disclosing pre-existing diseases. Seriously, don’t do it. While it might lead to higher premiums or a longer `waiting period health insurance` clause, non-disclosure is grounds for claim rejection. Be honest and transparent when filling out your application. It builds trust and ensures your claims won’t be denied when you need them most.

Lastly, don’t forget to regularly review your policy. Your family’s needs change over time. A policy that was perfect five years ago might no longer be sufficient today, especially with medical advancements and inflation. A periodic check-in with your policy, perhaps annually, can save you from future headaches. You can explore more options atfamily health insuranceplans.

Choosing the best health insurance for family is not a one-time decision; it’s an ongoing commitment to your family’s well-being. It requires a bit of research, a dash of foresight, and a willingness to understand the nuances. But the reward? The profound peace of mind that your loved ones are protected, come what may. And that, my friend, is truly priceless. You might also want to look intolife insuranceoptions for holistic financial planning.

Frequently Asked Questions About Family Health Insurance

What is a family floater plan and is it right for my family?

A family floater plan is a single health insurance policy that covers all members of a family under one sum insured, which can be utilized by any member during the policy year. It’s generally ideal for nuclear families (e.g., self, spouse, and two dependent children) as it often offers comprehensive coverage at a lower premium compared to individual policies for each member.

How do I compare different health insurance policies effectively?

To compare effectively, look beyond just the premium. Evaluate the sum insured, coverage scope, exclusions, waiting periods, network hospitals, co-payment clauses, claim settlement ratio of the insurer, and unique benefits like restoration or no-claim bonus. Consider using online comparison portals and reading policy documents thoroughly.

What happens if I need cashless hospitalization?

For cashless hospitalization, you need to be admitted to one of your insurer’s network hospitals. You or your family needs to inform the insurer (or Third-Party Administrator – TPA) within a specified timeframe (often 24-48 hours prior for planned, or within 24 hours for emergency hospitalization). The hospital will then coordinate directly with the insurer for bill settlement, relieving you of immediate payment burdens.

Can I add my parents to my existing family health insurance?

While some family floater plans allow adding dependent parents, it’s often more prudent to get a separate policy for them, especially if they are elderly or have pre-existing conditions. Adding them to a floater can significantly increase the premium and potentially exhaust the sum insured for other family members due to higher claim risks.

Are there any tax benefits associated with family health insurance?

Yes, premiums paid for health insurance policies are eligible for tax deductions under Section 80D of the Income Tax Act, 1961. You can claim deductions for premiums paid for yourself, your spouse, dependent children, and parents, up to specified limits, making it a tax-efficient way to secure your family’s health.

What are common reasons for claims being rejected?

Common reasons for claim rejection include non-disclosure of pre-existing diseases, claims made during a waiting period, treatments excluded from the policy, incomplete documentation, or claims for conditions not covered (e.g., cosmetic surgery). Always read your policy document carefully and provide accurate information to avoid rejections.